Author : Haya Assem

Reviewed By : Enerpize Team

Journal Entries in Accounting: Definition, Format, and Types

Table of contents:

- What is a Journal Entry?

- What to Include in a Journal Entry?

- What are the Main Types of Journal Entries?

- How to create a journal entry?

- What is the Accounting Purpose of Journal Entries?

- How to Track Journal Entries?

- Example of a Journal Entry

- Automate your Journal Entries with Enerpize!

- Key Takeaways

What is a Journal Entry?

A journal entry is a document that records all business transactions in a company's accounting books. Journal entry is an important step in the accounting cycle because it allows you to record transactions and financial activity in various sizes and types of accounting records.

Essentially, it requires meticulously tracking and documenting all financial activities. It tracks accounts and financial transactions while briefly explaining the transaction details.

Almost all businesses currently use a double-entry accounting system in which every transaction impacts at least two accounts; one is debited, and the other is credited, resulting in an equal in debits and credits amount journal entry, which is required.

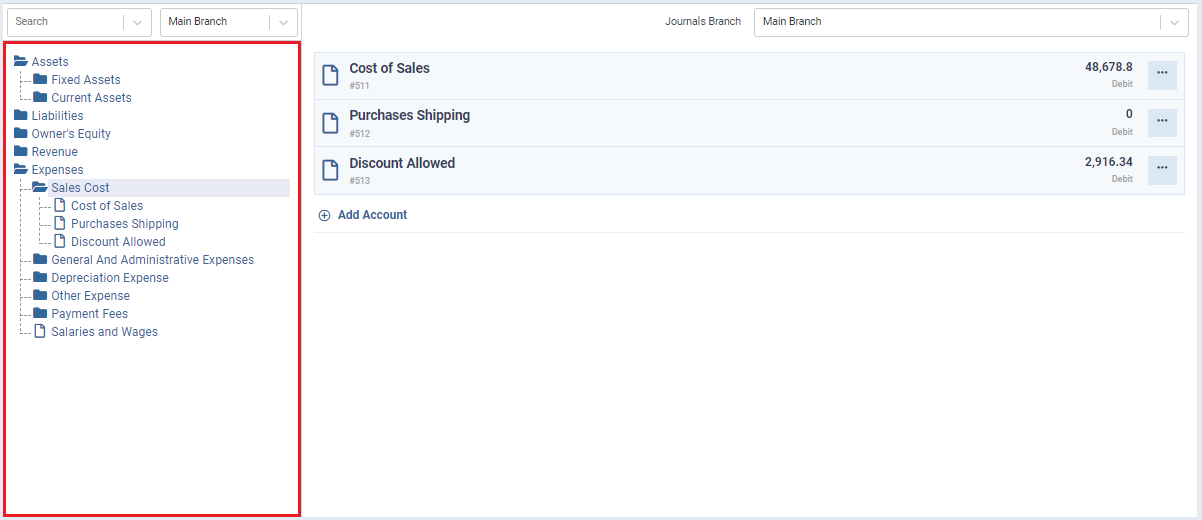

What to Include in a Journal Entry?

Journal entry's most important role is to record an organization’s transactions. In order to accurately reflect and recognize the transaction, you must include enough information about the transaction.

A journal entry requires a few elements to be included, these elements are:

-

Reference number: Unique identifier or reference no. to retrieve the entry when required.

-

Date: The date where the transaction took place.

-

Description: A brief description of the transaction’s details.

-

Accounts: Impacted accounts names or numbers.

-

Amounts: Debit and Credit amounts involved in the transaction.

.png)

What are the Main Types of Journal Entries?

Journal entries can be categorized into several types based on the nature of the transaction or event being recorded. There are 6 main types of journal entries which are:

-

Opening Entries: A current accounting period's opening entry is the preceding accounting period's closing balance. Recorded at the beginning of an accounting period to open various temporary accounts and establish account balances for the period.

-

Transfer Entries: It is an entry that records transactions from one account to another within the same organization. It involves debiting one account and crediting another account to reflect the incoming transfer.

-

Compound Entries: Involves more than two accounts and is used when multiple transactions are recorded in a single entry, and they may not follow the strict one-to-one rule of journal entries. For example, a single entry may involve both revenue and expense accounts.

-

Closing Entries: Made at the end of an accounting period to close temporary accounts (revenue, expense, and dividend accounts) and transfer their balances to the retained earnings or owner's equity account.

-

Adjusting Entries: These entries are made at the end of an accounting period to adjust account balances for accruals, deferrals, depreciation, and other adjustments necessary to accurately reflect the financial position of the business.

-

Reversing Entries: These entries are made at the beginning of an accounting period to reverse adjusting entries made in the previous period, simplifying the accounting process for certain transactions.

How to create a journal entry?

Preparing journal entries is an essential process in the field of accounting, as it plays a critical role in maintaining exact and comprehensive financial records for any organization. In the following lines, you will find accurate guidance for creating a journal entry.

.png)

-

Keep all invoices and documents related to all business transactions

Before creating a journal entry, it is essential to keep a detailed record of all business transactions. This entails meticulously gathering and categorizing invoices, receipts, and other relevant documents from all transactions. These records serve as the foundation for accurate financial reporting.

-

Determine the affected accounts

Once all necessary documents are in order, the next step is to analyze the transactions and determine which accounts are impacted. This entails identifying specific assets, liabilities, equity, revenues, or expenses that are influenced by the business operation or transaction in question.

-

Identify debit and credit accounts

The following step is to understand the nature of the transaction and the accounting rules associated with it in order to determine which accounts will be debited or credited such as revenue, expenses, liabilities, and assets.

-

Start preparing the journal entry

After identifying the impacted accounts and determining the debits and credits, you can start generating the journal entry.

Start by entering the transaction's date, recording debits and credits into the relevant accounts, and adding the transaction's unique number, which will help you to track transactions more easily. Also, add a brief description of the transaction with exact amounts.

-

Close your accounting entries

At the end of each accounting period, it is necessary to close temporary accounts such as revenue and expenses. Closing entries reset these accounts to zero, preparing them for the next accounting period.

This involves transferring the journal entries to a general ledger. The process ensures that the financial records accurately reflect the company's performance and position during a certain time period.

What is the Accounting Purpose of Journal Entries?

Journal entries serve an important part in the meticulous recording of a company's financial transactions. These entries comprehensively document all economic events affecting the company's assets, liabilities, equity, revenue, and expenses.

The double-entry system, which is fundamental to this procedure, ensures that each transaction affects at least two accounts, maintaining the accounting equation's integrity. The information produced from journal entries is then transferred to ledgers, resulting in a simplified overview of transactions related to specific accounts. These entries provide the raw data required for the preparation of financial statements.

They also help to ensure compliance with generally accepted accounting principles (GAAP) and other applicable accounting standards. Additionally, auditors rely significantly on them to carefully track and verify the accuracy of financial transactions, which plays a critical role in assessing the overall financial health of the business.

How to Track Journal Entries?

First, identify a system that is suitable for your business. This may be done using spreadsheets or accounting software like Enerpize. Categorize each expense, create subcategories, and ensure the transaction details are recorded accurately.

Additionally, regular account reconciliation is required. The process involves comparing your recorded transactions to bank statements to ensure accuracy and detect and correct any discrepancies.

Use cloud-based software to securely save digital data for the possibility of a disaster, such as a hard drive failure or theft. By following these tips, you will be able to keep track of your journal entries in an organized and efficient way.

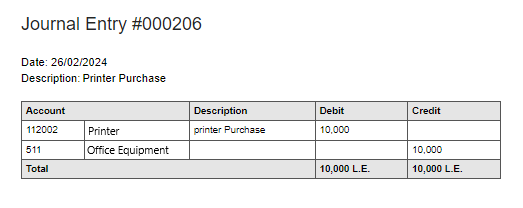

Example of a Journal Entry

Asset Purchase

When you first acquire new equipment, the account associated with that equipment is debited, but the account from which you paid for the asset is credited.

For example, if you buy a new printer that is worth $10,000 for your company, the printer account will be debited and the office equipment account credited with $10,000.

Automate your Journal Entries with Enerpize!

Much effort is frequently wasted revising entries, inputting daily transactions, and transferring them to the general ledger, which is a long and complex process. This is something Enerpize saves you from.

The software creates entries as soon as a transaction occurs in the system. It also automatically balances these transactions in the account ledger before transferring them to the general ledger for inclusion in the trial balance.

Furthermore, it includes them in the financial statements and reports. This saves you a lot of time and effort and also streamlines the work for the accounting team.

Key Takeaways

-

Journal entries are critical in accounting for documenting all business activities and tracking financial operations, and they use the double-entry approach to ensure accuracy and balance.

-

They record transactions accurately, including reference numbers, dates, descriptions, impacted accounts, and debit/credit amounts for clarity and recognition.

-

Journal entry types: Opening (start of period), Transfer (move between accounts), Compound (multiple transactions), Closing (period end), Adjusting (end adjustments), Reversing (simplify next period).

-

Essential steps in journal entry preparation: Organize transaction documents, identify affected accounts, determine debit/credit entries, generate entries with date and description, and close temporary accounts for accurate financial records.

-

Journal entries crucially document financial transactions, applying a double-entry system for integrity. They form the basis for ledgers, aiding compliance, and are vital for financial statements and auditing accuracy.

-

For an accurate tracking of journal entries choose a suitable system, categorize expenses, reconcile regularly with bank statements, and secure digital data.

Journal entries are easy with Enerpize.

Try our accounting module to mange your journal entries

Journal entries are easy with Enerpize.

Try our accounting module to mange your journal entries