Author : Haya Assem

Reviewed By : Enerpize Team

Prepaid Expense Journal Entries: A Comprehensive Guide

Table of contents:

- What is The Journal Entry for Prepaid Expenses?

- Uses of Journal Entries for Prepaid Expenses

- How to Record Journal Entries for Prepaid Expenses

- How to Write Expenses in A Journal Entry?

- How to Pass a Journal Entry for Expenses?

- Prepaid Expense Journal Entries in Financial Statements

- Prepaid Expenses Journal Entry Example

- How Enerpize Help in Recording Prepaid Expenses Journal Entries

- FAQs About Prepaid Expense Journal Entries

When businesses make payments in advance for products or services, these are known as prepaid expenses. Common examples include prepaid rent, insurance, and subscriptions. Initially classified as assets, these payments represent future benefits that will be gradually recognized as expenses over time. As these benefits are gradually realized, the prepaid expenses are systematically recorded as expenses on the income statement, ensuring accurate financial reporting.

Key Takeaways

- Payments made in advance for goods or services (e.g., rent, insurance) are recorded as assets because they represent future economic benefits.

- Two-Step Accounting Process:

- Initial Entry: Debit Prepaid Expense, Credit Cash/Bank

- Adjusting Entry (as the benefit is consumed): Debit Expense Account, Credit Prepaid Expense

- Ensures expense timing aligns with the benefit period (matching principle).

- Impact on Financial Statements:

- Balance Sheet: Increases assets (Prepaid Expense) and decreases cash

- Income Statement: Increases expenses over time, which reduces net income

- Prepaid expenses are gradually recognized monthly or as consumed, until fully expensed

What is The Journal Entry for Prepaid Expenses?

The journal entry for prepaid expenses first records the payment as an asset by debiting "Prepaid Expenses" and crediting "Cash." As the benefit is used, an adjusting entry debits the expense account and credits “Prepaid Expenses.”

The accounting side of prepaid expenses involves two main steps:

- Recording the Prepaid Expense (when the Payment is Made): When you pay for a service or product in advance, you record it as a prepaid cost in your accounting records.

- Recognizing the Expense as it is Incurred: As time passes and the prepaid expense is used (e.g., each month of the insurance coverage period passes), you need to gradually move the amount from the prepaid expense account to the relevant expenses account. This is done through an adjusting journal entry.

Uses of Journal Entries for Prepaid Expenses

Prepaid expenses play a crucial role in accurate financial reporting and management. Here are the key uses of journal entries for prepaid expenses:

Record Payments Accurately

Prepaid expense journal entries guarantee that any advance payments for products or services are accurately recorded as assets. This reflects that these payments are not considered expenses yet but future financial benefits to the business.

Match Expenses with Revenues

These journal entries help align expenses with the periods in which the associated benefits are received. Businesses adhere to the matching principle by gradually expensing prepaid amounts, ensuring that expenses are recognized in the same period as the revenues they help generate.

Maintain Accurate Financial Statements

Prepaid expenses are initially recorded as assets on the balance sheet. As they are consumed, they are systematically expensed, ensuring that the financial statements accurately reflect the company's financial condition at any given period.

Facilitate Financial Planning

Tracking prepaid expenses through journal entries allows businesses to more accurately track their cash flow. Businesses that are aware of when these prepaid amounts will be expensed can better prepare for future financial obligations and manage their resources.

Read Also: How To Track Business Expenses: A Comprehensive Guide

Support Audit and Compliance

Prepaid expenses journal entries provide a clear and credible record of advance payments. This transparency is critical for financial audits as it helps auditors to ensure that these expenses are appropriately recorded and expensed, resulting in improving overall compliance with accounting standards and laws.

How to Record Journal Entries for Prepaid Expenses

Recording journal entries for prepaid expenses involves recognizing expenses that are paid in advance but are not yet incurred. Here's how to do it step-by-step:

Initial Recording

When you initially pay for a prepaid expense, you record it as an asset because it represents a future financial benefit. This can be done by the following journal entry:

- Prepaid Expenses (Asset Account): This account is debited because the business pre-paid an expense. It is an asset account, as it represents a future benefit.

- Cash/Bank (Asset Account): This account is credited when a payment reduces the company's cash or bank balance.

Journal Entry

- Date: Date of Payment

- Account Debited: Prepaid Expense (Asset account)

- Account Credited: Cash/Bank (Asset account)

Example

If you pay $1,200 for an insurance policy that covers the next 12 months:

Recognizing the Expense (As the Benefit is Received)

As time passes and you incur the benefit of the prepaid expense, you need to adjust the prepaid expense account and recognize the expense in the correct period. This is done through an adjusting entry:

Adjusting Journal Entry

- Date: End of the Month

- Account Debited: Insurance Expense (Expense account)

- Account Credited: Prepaid Expense (Asset account)

Example

For the insurance policy, you will recognize $100 of insurance expenses each month ($1,200/12 months).

Read Also: How To Do Closing Entries: Explanation with Examples

How to Write Expenses in A Journal Entry?

Writing expenses in a journal entry means recording the costs your business has incurred during a specific period. The key rule is that expenses are recorded on the debit side, while cash or payables are recorded on the credit side. Recording expenses ensures that your costs are accurately reflected in the books while also showing the reduction in your available cash.

For example, if you pay $500 for office supplies in cash, the entry would be:

Debit Office Supplies Expense $500, Credit Cash $500.

| Account | Debit | Credit |

| Office Supplies Expense | 500 | |

| Cash | 500 |

How to Pass a Journal Entry for Expenses?

To pass a journal entry for expenses, start by identifying the type of expense incurred and the accounts affected. The expense account is debited to record the cost, while the account used to pay for it is credited either “cash” if it’s paid immediately, or “accounts payable” if payment will be made later.

This process ensures that expenses are recognized in the period they occur, following the accrual accounting principle.

For example, if your business receives a $1,200 electricity bill to be paid next month, the journal entry would be:

Debit “utilities expense” $1,200, Credit “accounts payable” $1,200.

| Account | Debit | Credit |

| Utilities Expense | 1,200 | |

| Accounts Payable | 1,200 |

Prepaid Expense Journal Entries in Financial Statements

Recording the prepaid expenses impacts both the balance sheet and the income statement.

Initial Entry: Recording Prepaid Expense

When you initially pay for a prepaid expense, such as an insurance policy, the transaction is recorded as an asset. This impacts the balance sheet but does not affect the income statement at the time of the payment.

Balance Sheet Impact

- Asset Increase: The prepaid expense account (e.g., Prepaid Insurance) increases because it represents a future benefit.

- Cash Decrease: The cash or bank account decreases because the payment reduces available cash.

The total assets remain unchanged, as the increase in prepaid insurance is offset by the decrease in cash.

Expense Recognition: Adjusting Expense

Over time, as the prepaid expense is utilized, it needs to be recognized as an expense. This adjustment impacts both the income statement and the balance sheet.

Income Statement Impact

- Expense Increase: The expense account (e.g., Insurance Expense) increases, which reduces net income.

Balance Sheet Impact

- Asset Decrease: The prepaid expense account decreases as the benefit is consumed.

- Current Assets Decrease: The reduction in prepaid expenses lowers the current assets on the balance sheet.

Example

If $100 of the prepaid insurance is recognized as an expense after one month:

- Insurance Expense (Income Statement): +$100

- Prepaid Insurance (Balance Sheet): -$100

The remaining prepaid insurance balance would be $1,100, reflecting the reduction in assets and corresponding impact on the income statement.

Read Also:

Payroll Journal Entries in Accounting: Definition, Types, & Examples

Journal Entries for Bank Reconciliation: A Comprehensive Guide

Intercompany Transactions Journal Entries: Importance & Examples

Lease Accounting Journal Entries: Types, Standards & Calculating Steps

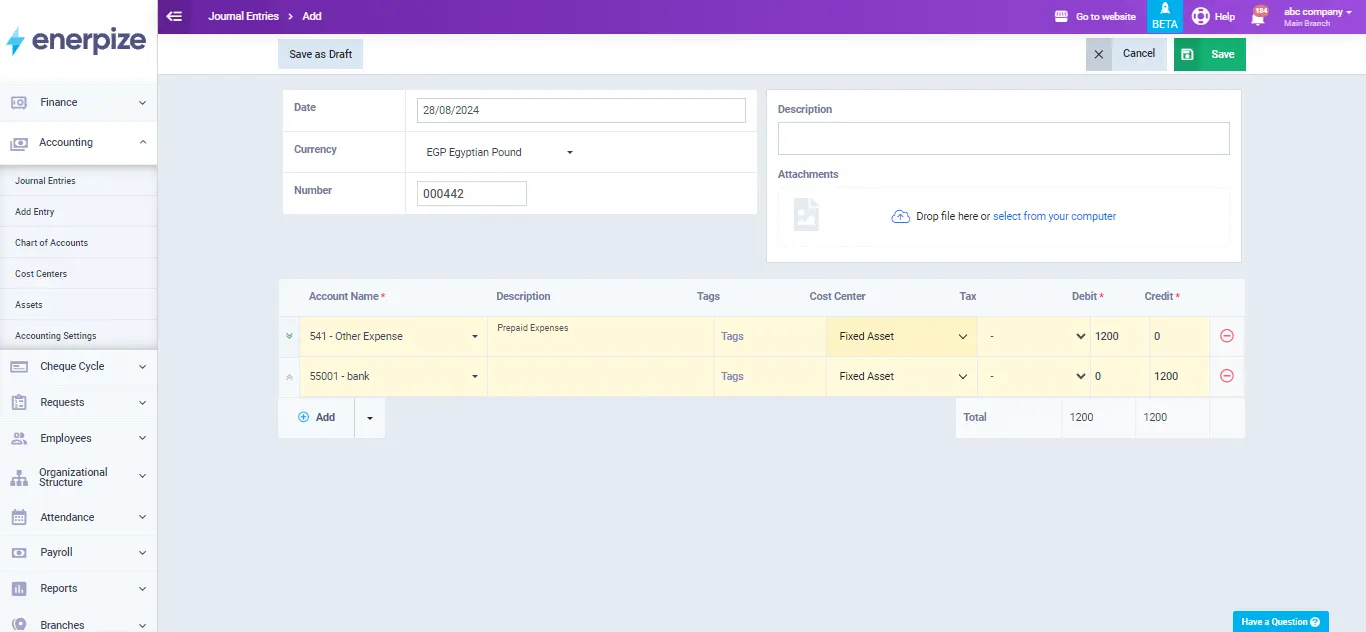

Prepaid Expenses Journal Entry Example

Imagine a company pays $1,200 on January 1st for a 12-month insurance policy that covers the period from January 1st to December 31st. This payment is made in advance, so it's considered a prepaid expense.

Initial Entry

Recording the Prepaid Expense.

On January 1st, you record the payment as a prepaid expense, which is an asset.

Journal Entry

- Prepaid Insurance (Asset): The debit increases the prepaid insurance account because the company now has a future benefit.

- Cash/Bank (Asset): The credit decreases the cash account because the company has paid out $1,200.

Monthly Expense Recognition

At the end of each month, you need to recognize the portion of the prepaid insurance that has been "used up" as an expense. Since the policy covers 12 months, you will recognize $100 of insurance expense each month ($1,200 / 12 months).

Journal Entry for January 31st

- Insurance Expense (Expense): The debit increases the insurance expense account, which will appear on the income statement and reduce net income for January.

- Prepaid Insurance (Asset): The credit decreases the prepaid insurance account, reflecting that part of the asset has been used up.

Repeating the Monthly Entry

You will repeat the above journal entry at the end of each month for the remaining 11 months. Each month, you'll recognize $100 in insurance expenses until the prepaid insurance account is fully amortized.

How Enerpize Help in Recording Prepaid Expenses Journal Entries

Enerpize comprehensive online accounting software allows businesses to accurately manage transactions and automates the tracking of prepaid expenses. You can easily log prepaid expenses, including cost centers, taxes, and descriptions, ensuring these transactions are automatically reflected in journal entries, reducing manual effort and errors. Enerpize's automation features allow for recurring journal entries, ensuring expenses like insurance or rent are recognized in the correct period.

The system supports tax management, offers detailed financial reports that update as expenses are amortized, and provides tools to track, reverse, and attach documents, giving full control over your financial statements.

FAQs About Prepaid Expense Journal Entries

What is the journal entry for expenses?

The journal entry for expenses records the cost incurred during a specific period. It typically involves debiting an expense account to show an increase in expenses and crediting either cash or accounts payable, depending on whether the expense has been paid or is still outstanding.

For example, if you pay $2,000 in cash for monthly office rent, the entry would be:

| Account | Debit | Credit |

| Rent Expenses | 2,000 | |

| Cash | 2,000 |

How to write a journal entry expenses?

To record an expense in a journal entry, start by identifying the nature of the expense (e.g., rent, utilities, or salaries).

- Debit the corresponding expense account to recognize the cost.

- Credit the payment source, such as cash (if paid immediately) or accounts payable (if payment is due later).

What is the journal entry for advance payments?

Prepaid expenses are considered assets until they are used. For example, if you pay $1,200 in advance for a year’s insurance, the entry is:

Debit Prepaid Insurance $1,200, Credit Cash $1,200.

As each month passes, you gradually move the amount from Prepaid Insurance to Insurance Expense.

How to record expenses in a journal entry?

Recording an expense follows the same logic:

- Debit the expense account to show that a cost has been incurred.

- Credit cash if it’s paid immediately, or accounts payable if payment is pending.

Recording prepaid expense entries is easy with Enerpize.

Try our accounting module to manage your expenses.

Recording prepaid expense entries is easy with Enerpize.

Try our accounting module to manage your expenses.