Author : Haya Assem

Reviewed By : Enerpize Team

Adjusting Entries: Definition, Types, and Examples

Table of contents:

- Key Takeaways

- What are Adjusting Entries?

- The Main purpose of Adjusting Entries

- Main Types of Adjusting Entries

- Adjusting Entries Examples

- How To Make Adjusting Entries?

- Importance of Adjusting Entries

- Adjusting Entries and Financial Statements

- Common Mistakes to Avoid When Making Adjusting Entries

- Adjusting Entries Best Practices

- How Can Enerpize Help You in Adjusting Journal Entries?

- FAQs

- Conclusion

Journal entries are the main pillar of accurate accounting records, they play a critical role in tracking a business's financial position. Each entry records a financial transaction, ensuring all activities are properly documented and accounted for.

According to the recurring nature of this process, with companies generating numerous journal entries daily, there is always the potential for errors or the need to account for transactions that still need to be recorded. This is where adjusting entries becomes essential.

Adjusting entries are crucial for correcting inaccuracies, accounting for unrecorded transactions, and ensuring that all income and expenses are accurately reflected in the appropriate accounting period. By making these adjustments, businesses can maintain the integrity of their financial records and produce reliable financial statements that accurately reflect their financial position.

Key Takeaways

- Adjusting entries ensure that all revenues and expenses are recorded in the correct accounting period, maintaining accurate financial statements.

- The main types of adjusting entries include accruals, deferrals, and non-cash adjustments such as depreciation, amortization, and provisions.

- Adjusting entries directly affect both the income statement and the balance sheet, reflecting a business's true financial performance and position.

- Common mistakes include failing to record accruals, misclassifying accounts, skipping depreciation, creating overly complex entries, and inconsistently timing adjustments.

- Best practices include documenting calculation methods, using accounting software to automate recurring entries, maintaining a closing checklist, keeping supporting documentation, and reviewing prior-period entries for consistency.

- Automation tools, like Enerpize, help streamline the adjustment process, minimize errors, track recurring adjustments, and provide audit trails alongside real-time financial data.

What are Adjusting Entries?

Adjusting entries are essential modifications made to the accounting records at the end of an accounting period. These entries are required to ensure that all income and expenses are recorded in the correct period, accurately reflecting the business's financial position.

Adjusting entries often involve accrued revenues, accrued expenses, deferred revenues, deferred expenses, and depreciation. By making these adjustments, businesses can ensure their financial statements comply with accounting standards and accurately reflect their financial performance and condition.

Read Also: How to Track Business Expenses?

The Main purpose of Adjusting Entries

The main purpose of adjusting entries is to ensure that a company’s financial records accurately reflect its financial position and performance at the end of an accounting period. These adjustments are recorded through journal entries to align the timing of revenues and expenses with the periods in which they actually occur, rather than when cash is received or paid.

Adjusting journal entries account for revenues earned but not yet recorded, expenses incurred but not yet paid or recorded, and other timing differences, ensuring that financial statements present a true and fair view, comply with accounting standards, and support informed decision-making.

Main Types of Adjusting Entries

Adjusting entries are classified by the type of transaction they address. They are essential for ensuring that all financial activities are properly recorded and accurately reflected in the financial statements at the end of an accounting period. The main types of adjusting entries include the following:

1- Accruals

Accruals record revenues and expenses that have been earned or incurred but not yet received or paid. These entries ensure that financial statements reflect actual business activities within the accounting period, regardless of cash movements.

Accrued Expenses

Accrued expenses are costs incurred but not yet paid or recorded in the accounting records. For example, wages earned by employees but unpaid at the end of the accounting period must be recognized as accrued expenses to reflect the company’s true liabilities.

Accrued Revenues

Accrued revenues represent income that has been earned but not yet received or recorded. This commonly occurs when services have been provided to customers but have not yet been billed. Adjusting journal entries for accrued revenues ensures that revenue is recognized in the period it is earned, not when cash is collected.

2- Deferrals

Deferrals involve cash transactions that occur before the related revenue is earned or the expense is incurred. Recognition is postponed until the appropriate accounting period to ensure proper matching of income and expenses.

Deferred Expenses

Deferred expenses, also known as prepaid expenses, arise when payments are made in advance for goods or services to be received in future periods. For instance, rent paid one year in advance is initially recorded as an asset and then systematically expensed over the period to which it relates.

Recommended for you: Prepaid Expense Journal Entries: Importance, Examples & How to Record

Deferred Revenues

Deferred revenues, or unearned revenues, occur when a business receives payment before providing goods or services. A common example is an advance payment for subscription-based services. Adjusting journal entries ensures that such revenue is recognized only when it is earned.

3- Non-Cash Adjustments

Non-cash adjustments include entries such as depreciation and amortization, which allocate the cost of long-term assets over their useful lives, as well as provisions that account for estimated future liabilities. These adjustments rely on accounting estimates and ensure that financial statements accurately reflect asset usage, wear and tear, and expected obligations.

Read Also: Reversing Entries: Definition and Examples

Adjusting Entries Examples

Adjusting entries can be classified into accruals, deferrals, and non-cash items, as explained previously. Each category addresses specific transactions that require adjustment to ensure revenues and expenses are properly matched with the correct accounting period. Below is an example of an adjusting entry for each type.

Accrued Revenues

A consulting firm provided services worth $5,000 in December but had not yet issued an invoice to the client by the end of the month. Even though the invoice has not been sent and payment has not been received, the firm must recognize the revenue in December to accurately reflect its financial performance.

Adjusting Journal Entry:

- Debit: Accounts Receivable — $5,000

Records the amount owed by the client for services already provided. - Credit: Service Revenue — $5,000

Recognizes revenue earned during December, in accordance with the accrual basis of accounting.

| Date | Account | Debit ($) | Credit ($) |

| 31 Dec | Account Receivable | 5,000 | |

| 31 Dec | Service Revenue | 5,000 |

Deferred Expenses (Prepaid Expenses)

A company prepaid $1,800 for six months of rent beginning in July. By September 30, three months of the rental period have expired. Therefore, the portion of rent related to those three months must be recognized as an expense.

Adjusting Journal Entry:

- Debit: Rent Expense — $900

Recognizes the cost of rent that has been used during the period. - Credit: Prepaid Rent — $900

Reduces the Prepaid Rent asset to reflect the expired portion of the prepaid rent.

| Date | Account | Debit ($) | Credit ($) |

| 31 Dec | Rent Expense | 900 | |

| 31 Dec | Prepaid Rent | 900 |

Read Also: Lease Accounting Journal Entries

Non-Cash Adjusting Entries

Non-cash adjusting entries involve accounts that do not require immediate cash transactions but are essential for presenting accurate and reliable financial statements.

Depreciation

A company purchased machinery for $12,000 with a useful life of five years. At year-end, the company must record $2,400 in depreciation expense to reflect the machinery’s usage during the period.

Adjusting Journal Entry:

- Debit: Depreciation Expense — $2,400

Recognizes the portion of the asset’s cost consumed during the accounting period. - Credit: Accumulated Depreciation — $2,400

Increases accumulated depreciation, thereby reducing the machinery's carrying value on the balance sheet.

This entry systematically allocates the machinery's cost over its useful life, ensuring that expenses are matched with the revenues they help generate.

| Date | Account | Debit ($) | Credit ($) |

| 31 Dec | Depreciation Expense | 2,400 | |

| 31 Dec | Accumulated Depreciation | 2,400 |

Explore more on this topic: What is Depreciation Journal Entry: Examples & How to Record

Read Also:

Payroll Journal Entries in Accounting: Definition, Types, & Examples

Intercompany Transactions Journal Entries: Importance & Examples

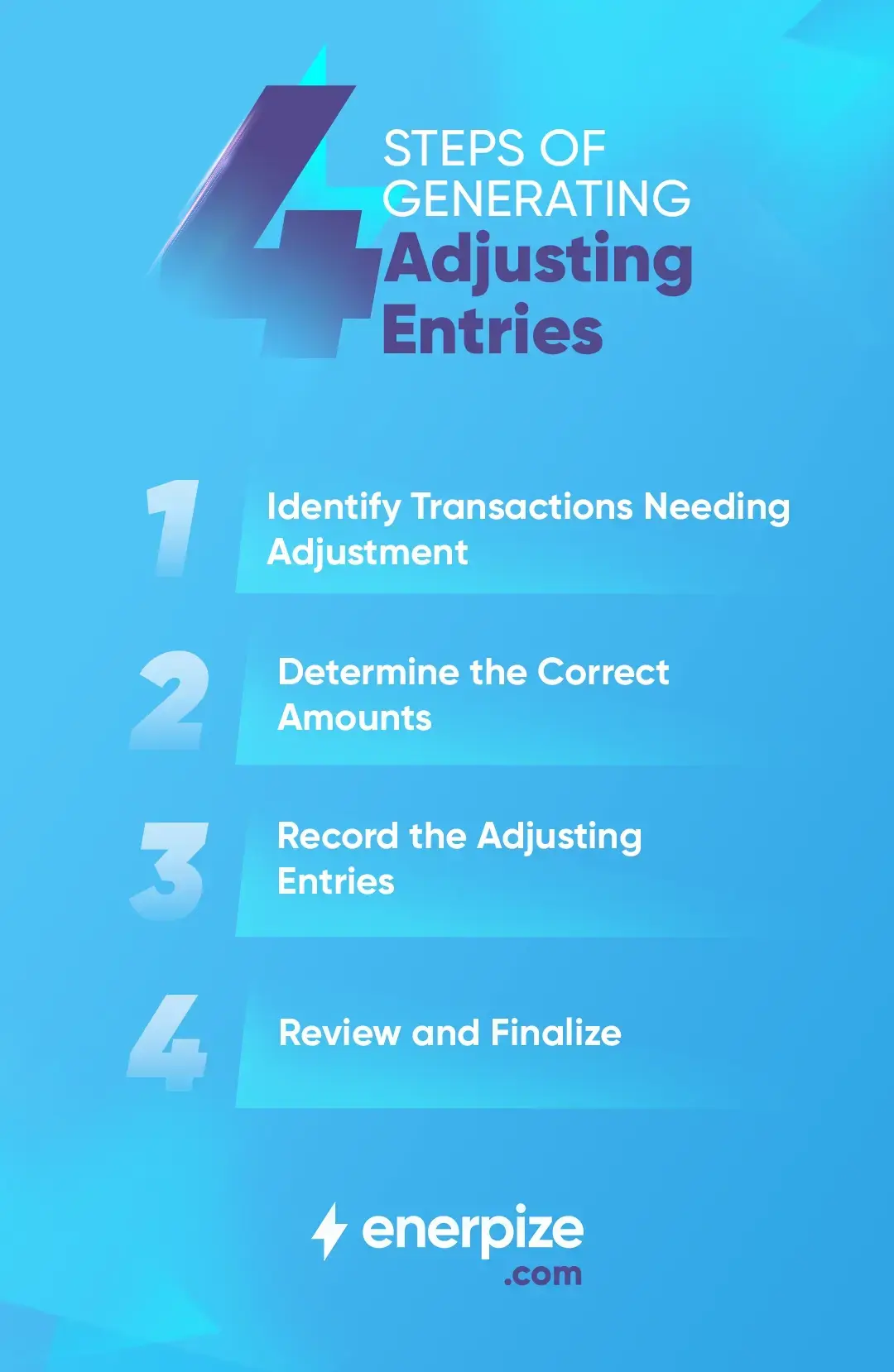

How To Make Adjusting Entries?

Adjusting journal entries are used to make necessary updates to a company’s financial records at the end of an accounting period. Their purpose is to ensure that revenues and expenses are recognized in the correct period, allowing the financial statements to accurately reflect the company’s true financial position and performance.

The process of preparing adjusting journal entries generally follows these steps:

1- Identify Transactions Requiring Adjustment

The first step is to identify transactions that have occurred during the period but have not yet been recorded. These typically include accrued revenues, accrued expenses, prepaid expenses, deferred revenues, and non-cash items such as depreciation.

2- Determine the Correct Amounts

For each identified transaction, the appropriate amount to be recorded must be calculated. This may involve determining interest earned, expenses incurred but not yet paid, the portion of prepaid expenses that has expired, or the depreciation expense for the period.

3- Record the Adjusting Journal Entries

After determining the correct amounts, the adjusting journal entries are recorded in the accounting system. These entries involve debits and credits to the relevant accounts to ensure that both the income statement and balance sheet reflect accurate figures.

4- Review and Finalize

Once all adjusting entries have been recorded, they are reviewed for accuracy and completeness. After verification, the accounting period is closed, and the financial statements are prepared, providing a clear and reliable representation of the company’s financial position and operating results.

Read also: Closing Entries in Accounting: What Are They & Examples

Importance of Adjusting Entries

Adjusting entries are a fundamental part of the accounting process, ensuring that a business’s financial records are accurate, complete, and reliable. By recording these necessary adjustments at the end of an accounting period, businesses preserve the integrity of their financial data and ensure compliance with accounting principles.

The following points highlight the key importance of adjusting entries in achieving precise and dependable financial reporting:

1- Maintain Accurate Financial Records

Adjusting entries play a vital role in maintaining accurate financial records by ensuring that all transactions are recorded in the correct accounting period. This helps prevent discrepancies and ensures that journal entries accurately reflect the business's financial position.

2- Track Payables and Receivables Efficiently

These entries help accurately track payables and receivables by ensuring that all amounts owed to and by the company are properly recorded. This is essential for effective cash flow management and on-time payment of financial obligations.

3- Accurately Record Expenses

Through adjusting entries, businesses can ensure that all expenses are recognized in the appropriate accounting period. This supports proper matching of expenses with revenues, resulting in more accurate financial reporting.

4- Correct Inaccuracies in Entries

Adjusting entries enable businesses to correct errors in previous records, such as omissions or misstatements. Addressing these inaccuracies helps maintain the reliability and credibility of financial records.

Read Also: Transposition Error: Definition, Example, And How To Correct

5- Ensure Financial Statements Accuracy

The accuracy of financial statements depends heavily on the use of adjusting entries. These adjustments ensure that all financial activities are fully and properly recorded, providing a true and fair view of the company’s financial position and performance.

Read Also: What Is The Journal Entry For Sales: Examples And How To Record

Adjusting Entries and Financial Statements

Adjusting entries serve as the critical link between day-to-day accounting records and accurate financial statements. While many transactions are recorded throughout an accounting period, not all revenues earned or expenses incurred are captured at the moment they occur. Adjusting entries ensure that financial statements reflect the true financial position and performance of a business at the end of the reporting period.

At the end of the accounting period, accountants typically prepare an unadjusted trial balance, which lists all ledger account balances before adjustments. Although this trial balance verifies the mathematical equality of debits and credits, it does not guarantee that all revenues and expenses have been properly recognized. Adjusting entries are therefore required to update these balances so they comply with the accrual basis of accounting.

Under the accrual basis of accounting, revenues must be recognized when earned and expenses when incurred—regardless of when cash is received or paid. Financial statements prepared directly from an unadjusted trial balance risk being incomplete or misleading. Adjusting entries correct this by modifying account balances and producing an adjusted trial balance, which forms the direct basis for preparing the income statement and balance sheet.

Impact on the Income Statement

The income statement measures a company’s performance over a specific period. Adjusting entries directly affect this statement by ensuring that all relevant revenues and expenses appear in the correct accounting period. These adjustments are reflected in the adjusted trial balance before the income statement is prepared.

For example:

- Accrued revenues ensure income is recognized for services performed or interest earned, even if not yet billed or received.

- Accrued expenses capture costs such as wages, utilities, or interest that have been incurred but not yet paid.

- Deferred expenses (such as prepaid insurance or supplies) allocate costs only to the periods in which they are actually consumed.

- Depreciation and amortization spread the cost of long-term assets over their useful lives, matching expenses with the revenues they help generate.

- Estimates, such as allowances for doubtful accounts, adjust expenses to reflect expected losses.

Without these adjustments being incorporated into the adjusted trial balance, net income may be overstated or understated, undermining the reliability of the income statement.

Impact on the Balance Sheet

The balance sheet presents a snapshot of a company’s financial position at a specific point in time. Adjusting entries ensure that assets, liabilities, and equity accounts shown in the adjusted trial balance are stated at accurate amounts as of the reporting date.

Examples include:

- Recording accounts receivable for earned but unbilled revenues.

- Recognizing liabilities such as interest payable, wages payable, or accounts payable for incurred but unpaid expenses.

- Adjusting asset balances for supplies used, insurance expired, or accumulated depreciation.

- Properly reporting unearned revenues as liabilities until the related goods or services are delivered.

Each adjusting entry affects at least one income statement account and one balance sheet account, and these effects are summarized in the adjusted trial balance, reinforcing the interdependence of the financial statements.

Ensuring Complete and Reliable Financial Reporting

Adjusting entries are recorded after the unadjusted trial balance and before the preparation of financial statements, completing the accounting cycle. Once all adjustments are posted, the adjusted trial balance serves as the primary tool for preparing accurate financial statements in accordance with accounting standards such as GAAP or IFRS.

In essence, adjusting entries are not merely technical corrections; they are foundational to financial integrity. Without them, the trial balance would not provide a reliable basis for financial reporting. With them, organizations can confidently present financial statements that accurately portray both performance over time and financial position at period-end.

Common Mistakes to Avoid When Making Adjusting Entries

Adjusting entries are essential for producing accurate financial statements, yet they are also one of the most common sources of accounting errors. These mistakes often follow predictable patterns and can distort both profitability and financial position if left uncorrected.

Understanding where errors typically occur—and how to prevent them—helps ensure reliable financial reporting.

1. Failing to Record Accruals and Omitted Transactions

One of the most frequent problems is neglecting to record revenues earned or expenses incurred during the reporting period. This often happens when invoices, utility bills, or payroll information arrive after the books are closed, or when small transactions are overlooked entirely.

How to avoid it:

Maintain a period-end accrual checklist that includes recurring items such as wages, utilities, interest, and unbilled revenue. Use systematic transaction capture processes—daily entries, receipt tracking, and regular account reviews—to ensure nothing is missed.

2. Misclassifying Accounts

Account misclassification occurs when transactions are recorded in the wrong category—for example, treating an asset as an expense, or recording deferred revenue as earned income. These errors are especially damaging when they cross between the income statement and balance sheet, as they affect retained earnings and carry forward into future periods.

How to avoid it:

Establish clear account coding rules and documentation standards. Require secondary review for non-routine or judgment-based entries to ensure proper classification.

3. Incorrect Treatment of Deferred Revenues and Prepaid Expenses

Prepayments are a common source of confusion. Businesses may mistakenly record advance customer payments as revenue rather than liabilities, or expense prepaid items immediately rather than recognizing them as assets to be amortized over time.

How to avoid it:

Apply a simple principle consistently:

- Cash received before earning revenue represents a liability.

- Cash paid before consuming a benefit represents an asset.

Clear policies and examples help reinforce correct treatment.

4. Skipping Depreciation and Other Non-Cash Adjustments

Because depreciation, amortization, and similar adjustments do not involve cash, they are often overlooked. Missing these entries can significantly overstate income and asset values.

How to avoid it:

Use automated accounting software or set recurring reminders based on predefined schedules. Review fixed asset registers regularly to ensure all assets are depreciated correctly.

5. Creating Overly Complex or Poorly Documented Entries

Unnecessarily complicated adjusting entries increase the risk of errors and make future reviews difficult. Vague descriptions such as “adjustment” or “correction” provide little audit trail and weaken internal controls.

How to avoid it:

Keep entries simple and focused on a single purpose. Every adjusting entry should include a clear explanation describing why the adjustment is needed and how the amounts were calculated. Break complex adjustments into multiple, easy-to-follow entries if necessary.

6. Imbalanced Debits and Credits

Errors in balancing debits and credits violate the foundation of double-entry accounting. These issues usually arise from manual calculations, data entry mistakes, or system overrides.

How to avoid it:

Rely on system controls that prevent posting unbalanced entries, and complement them with manual reviews—especially for large or unusual adjustments.

7. Lack of Review and Reconciliation Procedures

Posting manual adjustments without review increases the risk of numerical errors, incorrect account selection, and duplicate entries. In addition, failing to reconcile accounts regularly allows errors to accumulate over time.

How to avoid it:

Implement a dual-review or approval process for adjusting entries, particularly material ones. Reconcile key accounts—such as cash, receivables, payables, and inventory—at least monthly to identify discrepancies early.

8. Inconsistent Timing of Adjustments

Applying adjustments inconsistently from one period to another distorts trends and reduces comparability between reporting periods.

How to avoid it:

Establish a formal month-end or period-end closing schedule with defined deadlines for each adjustment type. Document procedures to ensure the same steps are followed every period.

Adjusting Entries Best Practices

Businesses can improve the accuracy of adjusting entries by implementing structured best practices as follows:

- Document calculation methods for recurring adjustments

- Use technology to automate repetitive entries

- Maintain a comprehensive closing checklist

- Keep supporting documentation for all adjustments

- Review prior-period entries to identify recurring patterns

- Focus on material adjustments that significantly impact financial statements

By recognizing common pitfalls and applying disciplined review processes, organizations can strengthen the accuracy and credibility of their financial information. Properly executed adjusting entries not only prevent errors but also enhance stakeholders’ confidence in financial reporting.

How Can Enerpize Help You in Adjusting Journal Entries?

Enerpize streamlines the creation of adjusting entries by automating accruals, deferrals, depreciation, and other required adjustments. By reducing reliance on manual processing, the system minimizes the risk of errors and saves valuable time.

Real-time access to financial data makes it easier to identify when adjustments are necessary, ensuring that financial statements remain accurate and up to date.

Enerpize online accounting software enables businesses to configure recurring adjusting entries, such as monthly prepaid expense allocations or annual depreciation schedules. The system automatically tracks and applies these entries consistently and on time.

In addition, Enerpize generates comprehensive reports and maintains detailed audit trails for all adjustments, providing full transparency to support financial review, statement preparation, and compliance with applicable accounting standards.

The software features user-friendly interfaces that guide users through the adjustment process, allowing even those with limited accounting experience to make adjustments accurately and easily.

FAQs

Why are adjusting entries journalized?

Adjusting entries are journalized to ensure that all financial transactions are recorded in the correct accounting period. They correct omissions, recognize revenues earned but not yet recorded, account for expenses incurred but not yet paid, and update non-cash items such as depreciation.

Journalizing these entries maintains the accuracy and integrity of the financial records and ensures that financial statements reflect a true and fair view of the company’s performance and position.

What is the difference between adjusting entries and correcting entries?

- Adjusting entries are made at the end of an accounting period to record accruals, deferrals, depreciation, and other timing differences, ensuring that income and expenses are recognized in the correct periods.

Correcting entries are made specifically to fix errors in previously recorded journal entries, such as misclassifications, incorrect amounts, or transactions posted to the wrong account.

In short, adjusting entries align financial records with the accrual basis of accounting, while correcting entries fix mistakes in the records.

Why are adjusting entries necessary?

Adjusting entries are necessary to:

- Ensure revenues and expenses are recognized in the correct accounting period.

- Correct inaccuracies and omissions in the financial records.

- Maintain accurate balances for assets, liabilities, and equity accounts.

- Comply with accounting standards such as GAAP or IFRS.

- Produce reliable financial statements that support informed decision-making by stakeholders.

When are adjusting entries recorded?

Adjusting entries are recorded at the end of an accounting period, after preparing the unadjusted trial balance but before finalizing the financial statements.

This timing ensures that all revenues, expenses, and other adjustments are properly reflected in the periods to which they relate, resulting in an accurate adjusted trial balance and reliable financial statements.

How to record adjusting entries?

Recording adjusting entries involves the following steps:

- Identify transactions requiring adjustment – e.g., accrued revenues, accrued expenses, prepaid expenses, deferred revenues, or non-cash items like depreciation.

- Determine the correct amounts – calculate the revenue earned, expense incurred, or portion of prepaid items or depreciation applicable for the period.

- Journalize the adjustments – create journal entries that debit and credit the relevant accounts to reflect the adjustments accurately in both the income statement and balance sheet.

Review and finalize – verify all entries for accuracy and completeness before closing the accounting period and preparing financial statements.

Conclusion

Adjusting entries are a cornerstone of accurate and reliable financial reporting. By recording these entries at the end of an accounting period, businesses ensure that revenues, expenses, and non-cash items are properly matched to the periods in which they occur.

This not only enhances the integrity of financial statements but also supports informed decision-making, compliance with accounting standards, and efficient financial management.

Adopting structured best practices and leveraging automation tools, such as Enerpize, helps organizations reduce errors, maintain consistency, and save time while producing financial statements that accurately reflect both performance and financial position.

In essence, well-executed adjusting entries form the backbone of trustworthy accounting and sound business decision-making.

Journal Entries Adjusting is easy with Enerpize.

Try our accounting module to manage your entries.

Journal Entries Adjusting is easy with Enerpize.

Try our accounting module to manage your entries.