Author : Haya Assem

What Is Accrued Liability for Small Business: A Detailed Guide

Table of contents:

- Key Takeaway Points

- What Are Accrued Liabilities?

- Types of Accrued Expenses

- Importance Of Accrued Liabilities In Accounting

- When Do Accrued Liabilities Typically Arise In A Business?

- Examples of Accrued Liabilities

- Accrued Liabilities Vs Accounts Payable

- Accrued Liabilities Vs Prepaid Expenses

- Journal Entries For Accrued Liabilities

- How To Calculate Accrued Liabilities?

- Automate Accrued Liabilities Calculating With Enerpize

- FAQs About Accrued Liabilities

Accrued liabilities are a crucial aspect of small business accounting, ensuring that expenses are recognized in the correct period, even if payment is delayed. They provide an accurate picture of financial obligations, helping business owners manage cash flow, maintain transparency, and make better financial decisions.

Understanding accrued liabilities, how they differ from other obligations, and how to record them correctly is key to keeping your books accurate and compliant.

Key Takeaway Points

- Accrued liabilities are amounts owed that are not yet paid, representing obligations still awaiting settlement.

- They ensure accurate financial reporting, matching expenses to the right accounting period.

- Routine accrued liabilities are regular, like salaries or utilities, while non-routine are irregular, such as bonuses or penalties.

- ِِAccrued liabilities from accounts payable and prepaid expenses, since no invoice has been received yet and no advance payment has been made.

- Journal entries debit expenses and credit liabilities, keeping reports accurate.

- Calculation involves identifying, estimating, and recording expenses to ensure liabilities accurately reflect real obligations.

What Are Accrued Liabilities?

Accrued liabilities (Accrued Expenses) are expenses that a company has incurred but has not yet paid or recorded through a formal invoice. They represent obligations for goods or services already received, where payment will be made in the future.

Read Also: What Are Liabilities: Meaning, Types, and How They Work in Accounting

Types of Accrued Expenses

Accrued expenses can be grouped into two main types depending on how frequently they occur and their nature:

1- Routine Accrued Liabilities

These are regular, recurring expenses that a company incurs in its day-to-day operations but has not yet paid. They are predictable and happen consistently over accounting periods, such as:

- Wages and Salaries: Employee pay earned in the current period but paid in the next payroll cycle.

- Interest Expense: Interest on loans that accumulates over time but is paid at a later date.

- Utilities: Electricity, water, or internet services used but not yet billed.

2- Non-Routine Accrued Liabilities

These are irregular or unusual expenses that do not occur every accounting period. They are less predictable and may arise from unexpected events or one-time obligations.

Examples:

- Legal Fees: Costs from an unexpected legal case that are incurred but not yet paid.

- Bonuses: Employee performance bonuses are accrued at year-end but paid in the following period.

- Repairs or Maintenance: Major unplanned repair expenses that have been incurred but will be settled later.

Enerpize accounting software helps businesses easily categorize accrued liabilities, ensuring accuracy in recognition and reporting. With automated expense tracking, you can avoid missed entries and keep liabilities aligned with real-time operations. Start for free.

You might also find this helpful: What Is Contingent Liability in Accounting?

Importance Of Accrued Liabilities In Accounting

Accrued expenses maintain the accuracy and integrity of financial reporting. Accrued liabilities ensure that expenses are recorded in the correct period, even if cash has not yet been paid. This is crucial for reflecting a company’s true financial position and performance.

Ensures Accurate Financial Reporting

Accrued liabilities’ most important role is allowing businesses to comply with the matching principle in accounting by preventing underreporting of expenses or overstating of profits, as expenses are recognized in the same period as the revenues they support.

Supports Better Decision-Making

Including unpaid expenses helps with budgeting, forecasting cash flows, and making informed investment and operational decisions, as managers and business owners gain a clearer picture of the company’s obligations through them.

Builds Stakeholder Trust

Investors, lenders, and regulators rely on financial statements to assess a company’s stability. Accurate recognition of accrued liabilities demonstrates transparency and strengthens stakeholder confidence.

Improves Cash Flow Management

Knowing which expenses have been incurred but not yet paid helps companies plan their cash needs. Businesses can set aside funds for future payments and avoid liquidity problems.

Enhances Compliance with Standards

Accounting frameworks like GAAP and IFRS require accrued liabilities to be recorded. Recognizing them properly ensures compliance with regulations and reduces the risk of audit issues.

Enerpize ERP software ensures that all accrued liabilities are properly captured with built-in automation that prevents underreporting or overstating expenses. Start for free.

You may also like: What Are Long-Term Liabilities: Examples And How To Calculate

When Do Accrued Liabilities Typically Arise In A Business?

Accrued liabilities arise when a business incurs obligations or expenses within an accounting period but postpones payment to a later date. They usually appear at the end of a reporting period, when adjustments are made to ensure expenses are matched with the revenues they relate to, in line with the accrual basis of accounting.

Enerpize simplifies end-of-period adjustments by automatically detecting unpaid obligations and creating the necessary accrual entries. Start for free.

Examples of Accrued Liabilities

Accrued liabilities can take many forms depending on the nature of a company’s operations. Some common accrued liabilities examples include:

Accrued Salaries and Wages

Expenses for employee services that have been earned but not yet paid by the end of the accounting period.

Accrued Interest

Interest owed on loans or borrowings that has accumulated but is not yet paid.

Accrued Taxes:

Tax obligations, such as income or property taxes, that are incurred but unpaid at the reporting date.

Accrued Utilities

Expenses for electricity, water, or other services that have been consumed but not yet billed.

Accrued Rent

Rent expense recognized when due, but payment is scheduled for a later period.

Accrued Bonuses or Commissions

Amounts earned by employees or sales staff but payable in a future period.

Enerpize’s reporting dashboard allows you to track all these accrued liabilities in one place to stay ahead of upcoming payments. Start for free.

Download Now: Accrued Expenses Reconciliation Template Excel

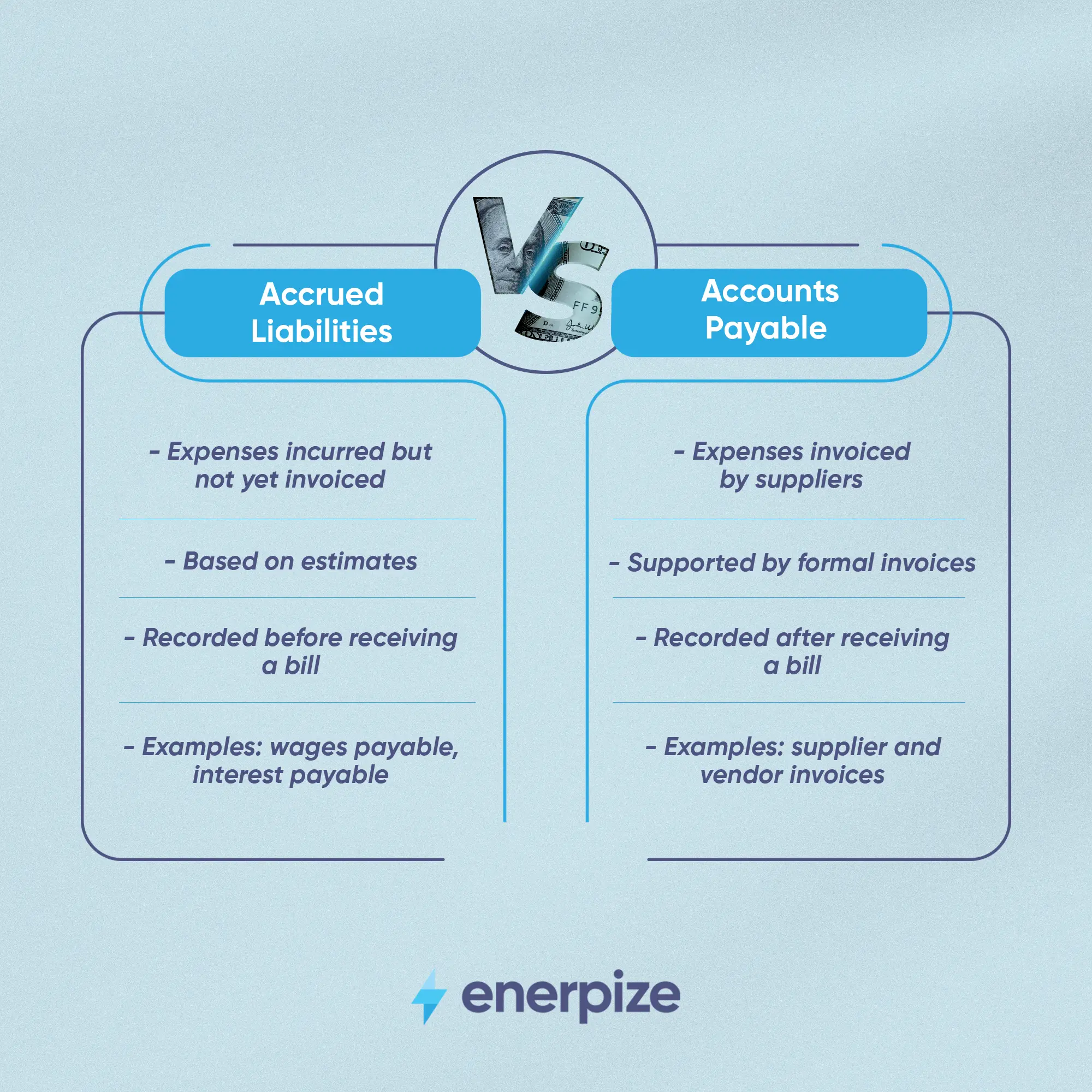

Accrued Liabilities Vs Accounts Payable

Accrued liabilities and accounts payable are both obligations that appear under current liabilities, but they differ in timing and recognition.

Accrued liabilities are recorded when a business has incurred an expense but has not yet received an invoice or billing request, making them largely based on estimates, such as wages earned but not yet paid or interest accumulating on loans.

While accounts payable arise once a company receives an invoice from a supplier or vendor for goods or services already delivered, meaning that accounts payable are always supported by documentation.

So, while accrued liabilities may lack immediate paperwork, accounts payable are backed by formal invoices.

Enerpize clearly distinguishes between accrued liabilities and accounts payable in your balance sheet, ensuring more accurate liability management and financial clarity.

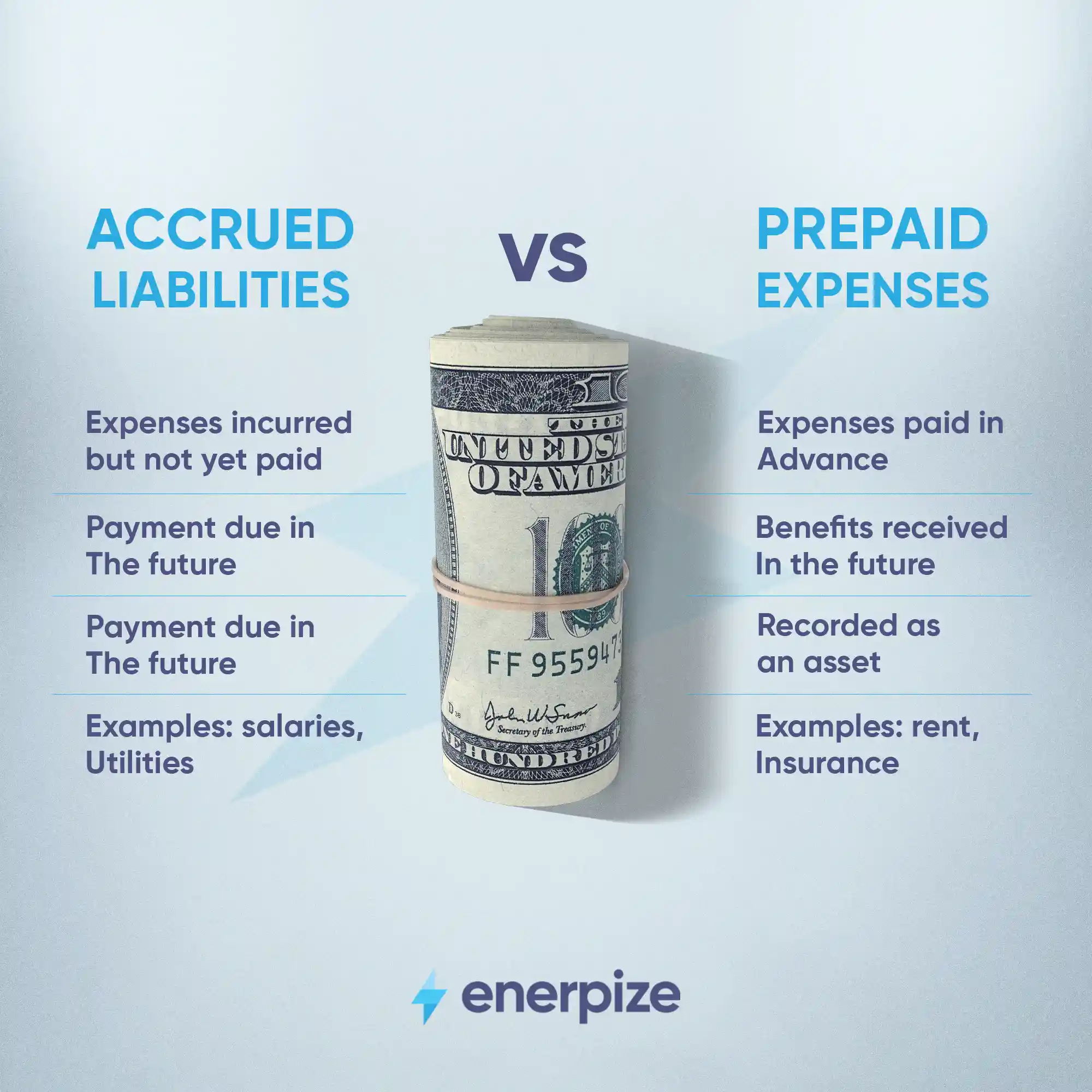

Accrued Liabilities Vs Prepaid Expenses

Accrued liabilities and prepaid expenses represent opposite sides of expense timing in accounting.

Accrued liabilities occur when a company owes money for expenses already incurred but not yet paid, such as salaries or utilities at the end of a reporting period. They increase liabilities on the balance sheet because the business has an obligation to settle them in the future.

Prepaid expenses, on the other hand, arise when a business pays for goods or services in advance of receiving them, like rent or insurance paid upfront. Instead of being a liability, they are recorded as assets because they provide future economic benefits.

Enerpize automatically separates accrued liabilities and prepaid expenses, recording them correctly as liabilities or assets.

Journal Entries For Accrued Liabilities

An accrued liabilities journal entry is recorded to recognize expenses that have been incurred but not yet paid. Under the accrual basis of accounting, these entries ensure expenses are matched with the revenues they help generate within the same period.

The general journal entry involves debiting the expense account to reflect the cost incurred and crediting an accrued liability account (such as accrued expenses payable) to recognize the obligation. Later, when the payment is made, the entry is reversed: the accrued liability account is debited, and cash is credited to show the outflow of funds.

Enerpize allows you to create and automate accrued liabilities journal entries, so businesses don’t need to manually adjust their books at the end of each period.

How To Calculate Accrued Liabilities?

1- Identify the Expense

The first step is to determine which expenses have been incurred but not yet paid by the business. These are obligations that the company owes, such as employee wages, utilities, loan interest, or supplier costs for services already delivered.

Explore more on this topic: What Is Business Expense Tracking and How To Do

2- Determine the Total Expense Amount

Once the expense is identified, the next step is to determine its full amount for the entire coverage period. This could involve reviewing contracts, vendor agreements, payroll details, or interest schedules.

3- Measure the Incurred Portion

Accrued liabilities focus only on the part of the expense that has already been incurred within the current accounting period. This step requires measuring the share of the total expense that corresponds to the elapsed time or services consumed.

4- Allocate the Expense

After determining the incurred portion, you must allocate it correctly to the accounting period. This often requires prorating the total amount based on time (days, weeks, or months) or usage levels.

The goal is to align the cost with the exact period in which the related benefit or service was received, ensuring proper expense recognition under the accrual basis of accounting.

5- Record the Liability

Finally, the calculated accrued expense is recorded in the books as a liability. Journal entries typically involve debiting the relevant expense account and crediting an accrued liabilities account.

Enerpize keeps all liabilities categorized and saved in one place, enabling you to easily identify and calculate the accrued ones without missing any obligations. Start for free.

Explore more on this topic: How to Calculate Total Liabilities: Formula and Examples

Automate Accrued Liabilities Calculating With Enerpize

Manually tracking and calculating accrued liabilities is a time-consuming process prone to errors, especially when a business manages multiple recurring expenses, such as accrued payroll liabilities, utilities, and loan interest. This is where Enerpize simplifies the process by automating the recognition and calculation of accrued liabilities within its accounting system.

Enerpize Online Accounting Software automatically identifies expenses that have been incurred but not yet paid, then matches them with the correct accounting period. Instead of relying on manual adjusting entries at the end of each month, Enerpize continuously monitors transactions, allocates expenses, and records them as liabilities in real time. This ensures accurate financial reporting that complies with the accrual basis of accounting.

Enerpize also provides detailed reports that make it easy to review outstanding obligations, track due dates, and plan cash flow accordingly. By automating the entire process, businesses reduce the risk of missing liabilities and eliminate repetitive calculations, instead relying on automated bookkeeping.

FAQs About Accrued Liabilities

Are Accrued Expenses Current Liabilities?

Yes. Accrued expenses are considered current liabilities because they represent short-term obligations that a company expects to settle within one year or one operating cycle, whichever is longer.

Are Accrued Liabilities Current Liabilities?

Yes. Accrued liabilities are also current liabilities since they are amounts owed for expenses that have already been incurred but not yet paid, typically due within the same accounting year.

How Do Adjusting Entries For Accrued Expenses Affect Liabilities And Expenses?

Adjusting entries increase both expenses and liabilities. For example, recording accrued wages means debiting wages expense (increasing expenses) and crediting accrued wages payable (increasing liabilities).

Is Accrued Liabilities An Operating Activity?

Yes. Most accrued liabilities, such as wages, utilities, and rent, relate to a company’s normal operations. Therefore, they are classified as operating activities on the cash flow statement.

Are Accrued Liabilities Current Or Noncurrent Liabilities?

Accrued liabilities are generally current liabilities. However, if an obligation is not due within one year (such as long-term accrued interest), it can be classified as a noncurrent liability.

What Are Accrued Liabilities On A Balance Sheet?

Accrued liabilities on balance sheet appear under current liabilities, representing expenses that have been incurred but not yet paid, such as salaries payable, interest payable, or utilities payable.

Is Accrued Liabilities An Asset?

No. Accrued liabilities are not assets. They are obligations (liabilities) that require the business to pay cash or deliver goods/services in the future.

What Is The Difference Between Accounts Payable And Accrued Liabilities?

- Accounts Payable: Obligations backed by an invoice from a supplier.

- Accrued Liabilities: Expenses recognized before receiving an invoice (e.g., wages earned but not yet paid).

What Is The Journal Entry For Accrued Liabilities?

The typical journal entry is:

- Debit: Expense account (e.g., Salaries Expense)

- Credit: Accrued Liabilities (e.g., Salaries Payable)

What Are Examples Of Deferred Liabilities?

Deferred liabilities are obligations postponed for future periods, such as pension obligations, deferred tax liabilities, or lease obligations.

What Is The Accrued Liability Rule?

The accrued liability rule follows the accrual accounting principle, which requires recognizing expenses when they are incurred, not when cash is paid.

Calculating accrued liabilities is easy with Enerpize.

Try Enerpize accounting software to manage your business expenses.

Calculating accrued liabilities is easy with Enerpize.

Try Enerpize accounting software to manage your business expenses.