Author : Haya Assem

What Is Contingent Liability in Accounting: A Comprehensive Guide

Table of contents:

- Key Takeaways

- What Are Contingent Liabilities?

- Contingent Liabilities Examples

- Importance Of Considering Contingent Liabilities

- Main Types Of Contingent Liabilities

- How To Record Contingent Liability?

- How to Treat Contingent Liabilities in Accounting

- What Is The Contingent Liabilities Journal Entry?

- How Does Enerpize Help Businesses In Contingent Liabilities Treatment?

- FAQs About Contingent Liabilities

Contingent liabilities are important in accounting because they indicate potential financial obligations based on uncertain future occurrences. While they may not always occur, their identification and disclosure are critical for accurate financial reporting, investor credibility, and smart decision-making.

Learning how contingent liabilities are defined, reported, and addressed under accounting standards such as GAAP and IFRS may help businesses stay transparent and prepared for possible financial risks.

Key Takeaways

- Contingent liabilities are potential obligations that depend on the outcome of uncertain future events.

- They are classified as probable, possible, or remote, depending on the likelihood of occurrence.

- Only probable and measurable liabilities are recorded in the financial statements; others are disclosed or omitted.

- Common examples include lawsuits, warranties, loan guarantees, and tax disputes.

- Proper treatment ensures compliance with GAAP/IFRS and builds stakeholder trust.

What Are Contingent Liabilities?

Contingent liabilities are potential financial obligations that may or may not occur, depending on the result of a future event. Contingent liabilities are not certain and are typically recorded in a company’s financial statements only if the likelihood of the event is probable and the amount of the liability can be reasonably estimated.

Contingent Liabilities Examples

Contingent liabilities are only recorded in financial statements if the loss is probable and the amount is reasonably estimable. Otherwise, they are disclosed in the notes or omitted entirely, depending on the likelihood and measurability.

Here are common examples of contingent liabilities:

Pending Lawsuits

If a company is being sued and it's likely to lose the case, it must record a liability for the estimated legal settlement or penalty.

Product Warranties

When a business sells products with warranties, it must estimate future repair or replacement costs and record them as contingent liabilities.

Loan Guarantees

If a company guarantees a loan for another party, it may become responsible for repayment if that party defaults.

Tax Disputes

If the company is involved in a dispute with tax authorities, and there’s a chance of an unfavorable outcome, the estimated tax due is considered a contingent liability.

Read Also: What Is Tax Liability: A Complete Guide

Importance Of Considering Contingent Liabilities

Although contingent liabilities are uncertain, they can have a significant impact on a company's financial future. Whether it's a pending lawsuit or a potential warranty claim, understanding and evaluating contingent liabilities is important for accurate financial reporting, strategic planning, and maintaining stakeholder trust.

Affects Financial Health

Contingent liabilities can reduce a company’s assets and net profitability, impacting overall financial performance.

Critical for Financial Statement Users

Investors and creditors rely on this information to assess future cash flow risks and financial obligations.

Influences Lending Decisions

Lenders consider contingent liabilities when setting loan terms, as they reflect potential financial risk.

Guides Strategic Planning

Business leaders use knowledge of these liabilities to make informed decisions about expansion, investments, or cost control.

Ensures Transparency

Accurate recognition and disclosure support better financial reporting and build trust with stakeholders.

Enerpize accounting software makes this process easier by providing automated journal entries, liability tracking, and clear financial statement presentation. This ensures contingent liabilities are recognized and disclosed accurately.

Read Also: Accrued Liabilities in Accounting: Definition and Examples

Main Types Of Contingent Liabilities

Contingent liabilities are categorized based on the likelihood of the event occurring and whether the amount of loss can be reasonably estimated. Understanding the types of contingent liabilities helps businesses determine how and when to recognize or disclose such liabilities.

Probable Contingent Liabilities

These are liabilities where the likelihood of the event occurring is high (more than 50%), and the amount can be reasonably estimated. In such cases, the liability is both recorded in the financial statements and disclosed in the notes.

Example: A pending lawsuit where legal counsel believes the company will likely lose and estimates the settlement cost.

Possible Contingent Liabilities

These are situations where the event might occur, but it's not likely enough to warrant recording the liability in the accounts. However, they should be disclosed in the notes to the financial statements.

Example: A legal dispute where the outcome is uncertain and cannot be predicted with reasonable assurance.

Remote Contingent Liabilities

These are liabilities with a very low likelihood of occurring. Neither recording nor disclosure is usually required unless the potential loss is unusually large or significant.

Example: A frivolous lawsuit with little to no chance of resulting in a financial obligation.

In Enerpize, you can easily track contingent liabilities by setting them up as provisional journal entries, linking them to expense categories. You can also schedule reminders to revisit and update these liabilities as new information becomes available.

How To Record Contingent Liability?

Recording a contingent liability depends on the likelihood of the event occurring and whether the amount can be reasonably estimated. Businesses must follow the accounting standards (such as IFRS or GAAP) to determine the proper treatment.

Step 1: Assess the Likelihood

Determine whether the liability is probable, possible, or remote. This classification is essential to decide whether it should be recorded or only disclosed in the notes.

Step 2: Estimate the Amount

If the liability is probable, make a reasonable and reliable estimate of the financial obligation. If the amount cannot be estimated, disclosure in the notes is still required.

Step 3: Make the Journal Entry (for Probable Liabilities)

Contingent liabilities must be recorded if the liability is probable and measurable; record it in the accounts:

- Debit: Expense account (e.g., Legal Expense)

- Credit: Liability account (e.g., Lawsuit Payable)

Enerpize streamlines this process by creating journal entries directly under your accounting and journal entries section, tagging them with specific expense categories like “Legal Costs.”

You can also add attachments (such as lawsuit documents or settlement letters) to the entry for reference, and set follow-up reminders to review the liability status.

Recommended for you: How to Calculate Liabilities: Formula and Examples

How to Treat Contingent Liabilities in Accounting

In accounting for contingent liabilities, the treatment depends on the probability of the event occurring and whether the amount can be reasonably estimated. The main rules under GAAP and IFRS are:

1- Probable and Measurable

If the future event is likely to occur (probable) and the amount can be reasonably estimated, the contingent liability must be recorded in the financial statements.

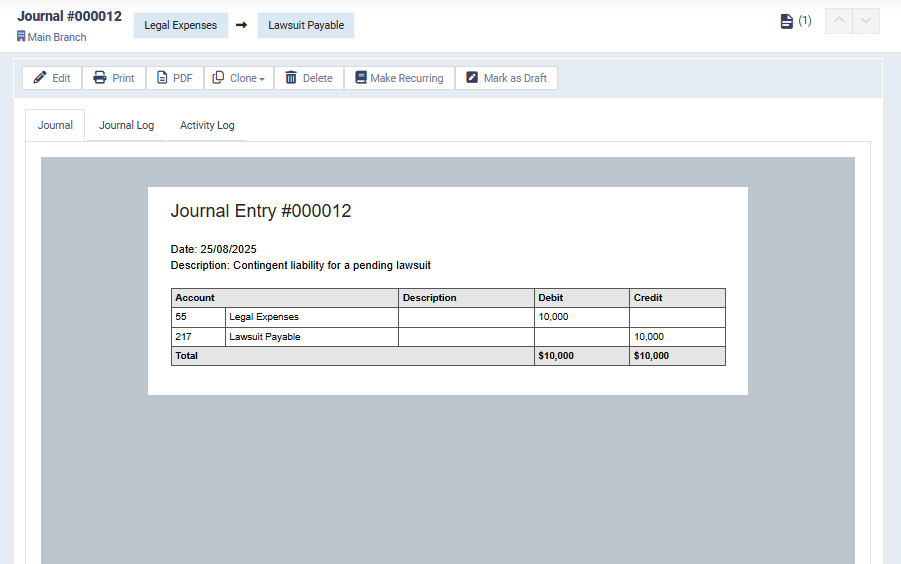

Example: A company is facing a lawsuit it will likely lose, with an estimated settlement of $50,000. This amount should be recorded as:

- Debit: Legal Expense – $50,000

- Credit: Lawsuit Payable – $50,000

2- Probable but Not Measurable

If the liability is probable but the amount cannot be reasonably estimated, it is not recorded but must be disclosed in the financial statement notes.

3- Possible

If the chance of occurrence is possible but not probable, the liability is only disclosed in the notes, with a description and estimated range if available.

4- Remote

If the likelihood is remote, no recording or disclosure is required.

Key point: Businesses must review contingent liabilities at each reporting date and update their recognition or disclosure based on the latest information.

You might also find this helpful: Long Term Liabilities In Accounting: Examples And How To Calculate

What Is The Contingent Liabilities Journal Entry?

A contingent liabilities journal entry is the accounting record made when a company recognizes a potential financial obligation that is both probable and can be reasonably estimated.

This entry ensures that the financial statements reflect not only current obligations but also likely future ones, giving creditors, investors, and management a transparent view of potential risks.

The journal entry typically looks like this:

- Debit: Expense account

- Credit: Liability account

Example: Suppose a company is facing a lawsuit where legal advisors believe it is probable the company will lose, and the estimated settlement is $50,000. The contingent liabilities journal entry would be:

- Debit: Legal Expense, $50,000

- Credit: Lawsuit Payable, $50,000

This entry records the expense in the income statement and the liability on the balance sheet, ensuring stakeholders are aware of the potential obligation.

Enerpize accounting software enables businesses to easily add and track contingent liabilities journal entries. Enerpize ensures proper classification under expenses and liabilities, making financial reporting more accurate and efficient.

How Does Enerpize Help Businesses In Contingent Liabilities Treatment?

Contingent liabilities can be tricky because they involve uncertainty, but Enerpize online accounting software makes the process more organized and transparent. Instead of managing potential obligations manually, businesses can rely on Enerpize’s accounting tools to stay compliant and in control.

- Accurate Classification: Enerpize allows you to categorize liabilities as probable, possible, or remote using journal entries and notes.

- Streamlined Journal Entries: For probable liabilities, you can easily record expenses and create liability accounts (e.g., Lawsuit Payable) directly within Enerpize’s accounting module..

- Disclosure & Documentation: Enerpize lets you attach supporting documents, such as legal opinions, settlement estimates, or contracts, directly to journal entries.

- Automated Reminders & Tracking: Since contingent liabilities often evolve over time, Enerpize helps you set reminders and track updates. For example, you can schedule follow-ups to reassess the liability if court hearings or negotiations change the outcome.

- Customizable Reporting: Enerpize generates real-time financial reports where contingent liabilities can be highlighted, helping management and auditors quickly identify potential risks before they impact cash flow.

FAQs About Contingent Liabilities

Which Accounting Standards Provide a Lower Threshold for Recording Contingent Liabilities?

Under IFRS, the threshold for recognizing a contingent liability is lower compared to GAAP.

IFRS uses the term “probable” with a likelihood of more than 50%, while GAAP requires a higher standard of likelihood.

Where Are Contingent Liabilities Recorded?

Contingent liabilities are only recorded in the balance sheet if the liability is both probable and measurable. Otherwise, they are disclosed in the notes to the financial statements.

Is Contingent Liability Good or Bad?

A contingent liability isn’t inherently good or bad; it depends on its outcome. However, it signals potential financial risk, which is why disclosure and monitoring are essential.

What Are Examples of Contingent Liabilities?

- Pending lawsuits

- Product warranties

- Guarantees on loans

- Environmental obligations

- Tax disputes

What Is the Rule for Contingent Liabilities?

The rule is:

- Probable & measurable → Record in the accounts.

- Reasonably possible → Disclose in the notes.

- Remote → No recording or disclosure required.

Is Contingent Liability Shown in the Balance Sheet?

Yes, but only if it is probable and the amount can be reasonably estimated. Otherwise, it stays off the balance sheet and is disclosed in the notes.

How Do You Identify Contingent Liabilities?

Businesses identify them by reviewing contracts, lawsuits, guarantees, pending disputes, and warranties that may create future obligations.

What Is the Difference Between a Current Liability and a Contingent Liability?

- Current liability: A definite, known obligation (e.g., accounts payable).

- Contingent liability: A potential, uncertain obligation (e.g., pending lawsuit).

What Is the Journal Entry for a Contingent Liability?

If the liability is probable and measurable:

- Debit: Expense account

- Credit: Liability account

Managing contingent liabilities is easy with Enerpize.

Try Enerpize accounting software to control your obligations.

Managing contingent liabilities is easy with Enerpize.

Try Enerpize accounting software to control your obligations.