Author : Haya Assem

Tax Liabilities: Definition, Types & How to Reduce

Table of contents:

- Key Takeaways

- What Is Tax Liability?

- Tax Liabilities Meaning

- Types of Tax Liabilities

- Tax Liability by Entity Type

- Tax Liabilities Examples

- What Are the Deferred Tax Liabilities?

- What Are Federal Income Tax Liabilities?

- What Are Tax Liabilities on W2?

- How To Calculate Tax Liabilities

- How to Estimate Tax Liability for the Year?

- Tax Liability vs Tax Owed vs Tax Refund

- Where to Find Tax Liability on Form 1040?

- How To Reduce Tax Liability?

- Common Mistakes When Calculating Tax Liability

- Streamline Tax Liabilities Calculating With Enerpize

- FAQs About Tax Liabilities

Tax obligations are not simply numbers and amounts paid at the end of each year; they are a fundamental element that directly impacts individual profitability and business sustainability. Inaccurate tax management can lead to unexpected financial penalties and losses that could be easily avoided with a thorough and accurate understanding.

A tax obligation is the total amount of tax owed by individuals and businesses to the relevant authorities, and it is determined based on income, sales, or taxable activities.

It is important to distinguish between the tax obligation and the final amount due when filing the tax return. This final amount can vary due to tax deductions, exemptions, or payments.

Key Takeaways

- Tax liability is the total tax due before any deductions or adjustments.

- Tax liability is calculated on gross income, taking into account deductions, exemptions, and tax brackets.

- There are many types of taxes, including income tax, corporate tax, payroll tax, sales tax, self-employment tax, and capital gains tax.

- Taxes depend on the type of income and activity, meaning they don't apply to everyone.

- Tax liability can be reduced through several factors.

- Tax liability can be current or deferred.

- Forgetting to include income or deductions, or using incorrect tax rates, are among the most common mistakes.

What Is Tax Liability?

Tax liabilities are the total amount of taxes legally owed by individuals and businesses to the government or relevant tax authorities, based on income, sales, salaries, or any other taxable activity.

From an accounting perspective, they represent a debt that must be legally paid within a specific tax period, whether paid in advance or as due.

To make things clearer, let's distinguish between tax obligations and related concepts:

- Tax Liabilities: The total tax calculated on income before any deductions or payments.

- Withholdings: Amounts deducted from income and transferred directly to the tax authorities during the year.

- Advance Payments: Payments that an individual or company may make periodically during the year to cover part of the expected tax.

- Final Balance Refunded or Due: The final difference between tax liabilities and total withholdings and payments.

Tax liability starts the moment income is earned. Enerpize tracks every taxable transaction in real time — so you always know what you owe before it's due. Start for free.

Tax Liabilities Meaning

Tax liabilities meaning refers to the total financial obligation a person or business owes to tax authorities for a specific period. In accounting terms, a tax liability is a legally enforceable debt — it arises the moment taxable income is earned, a taxable sale is made, or a taxable event occurs, and must be settled within the applicable tax period.

Types of Tax Liabilities:

Tax liabilities vary depending on the source of income and the nature of the economic activity, as individuals and companies are subject to various types of taxes. Some of the most prominent tax obligations include:

Income Tax:

This is the tax levied on the income earned by an individual or company during a specific tax period.

Corporate Tax:

This is the tax levied on company profits after deducting all operating expenses.

Payroll Tax:

This is the tax levied on payroll, divided between the employee and the employer, and usually includes social security contributions.

Sales Tax:

This is a tax applied to the sale of goods and services and is borne by the consumer.

Self-Employment Tax:

This is a particularly important tax in the United States, levied on self-employed individuals and small business owners. The individual is responsible for paying their own share, as well as the employer's share.

Capital Gains Tax:

This is a tax resulting from the sale of assets such as stocks, real estate, or businesses.

Here is a comparison table between the tax liability types:

| Type | Who does it apply to | Example |

| Income Tax | Individuals and companies | salaries |

| Corporate Tax | Companies | Company Profits |

| Payroll Tax | Employees | salary deduction |

| Sales Tax | consumers | Products or services |

| Self-Employment Tax | Independents | Freelancers |

| Capital Gains Tax | investors | Sale of assets or shares |

Read Also: A Comprehensive Guide to Current Liabilities

Tax Liability by Entity Type

Tax obligations vary depending on the type of legal entity. Individuals, companies, and other entities are treated differently in terms of tax calculation and payment deadlines.

Individuals

Individuals are subject to tax on their personal income, including salaries, freelance work, and investment income.

Tax is calculated based on gross income after deducting all exemptions and deductions, and then the appropriate tax bracket is applied.

Companies

Companies are subject to tax on their total net profits after deducting all operating expenses. Tax obligations here include income tax, sales tax in some cases, and payroll taxes for employees.

Small Businesses or Sole Proprietorships

Tax obligations are calculated within the individual business owner's personal tax return, with profits added to their gross income.

Non-Profit Entities

These activities and entities enjoy tax exemptions, but they remain subject to certain obligations, such as payroll taxes or taxes on any activities unrelated to the business or entity.

Tax Liabilities Examples

To better understand how tax liabilities work in real-world situations, here are some practical examples of the most common types of tax liabilities:

Income Tax Liability Example

An employee earns $60,000 annually. After a $12,000 standard deduction, taxable income is $48,000. Applying progressive brackets, the gross income tax liability is approximately $5,426. The employer withholds $450 per month ($5,400 annually). At filing, the employee owes $26 additional.

Sales Tax Liability Example

A retailer sells $50,000 of goods in a state with 10% sales tax. Sales tax collected from customers: $5,000. This $5,000 is a current liability on the balance sheet until remitted to the state tax authority, typically monthly or quarterly.

Payroll Tax Liability Example

A company runs a $40,000 monthly payroll. Employee FICA withholding (7.65%): $3,060. Employer FICA match (7.65%): $3,060. Total payroll tax liability for the month: $6,120, split equally between employee withholding and employer contribution.

Enerpize invoicing software can automatically apply sales tax to invoices. After you set up sales tax, the system applies it to invoices whenever the “Sales Tax” option is selected.

What Are the Deferred Tax Liabilities?

Deferred tax liabilities are taxes a company owes but postpones paying to future periods. They arise due to temporary differences between financial statements and tax returns, often from depreciation methods or revenue recognition timing.

Although the tax isn’t due now, it represents a future obligation the company will eventually have to settle with the tax authorities.

Recommended for you: Long Term Liabilities In Accounting: Examples And How To Calculate

What Are Federal Income Tax Liabilities?

Federal income tax liabilities are the total income tax owed by individuals or businesses to the federal government, determined based on taxable income during a specific period. Failure to pay federal income tax liabilities can result in penalties, interest, or legal action by the Internal Revenue Service (IRS).

This obligation depends on key factors that affect its final value:

- Taxable income: where the tax liability is calculated after deducting all exemptions and deductions.

- Tax brackets: where taxes are applied progressively according to the income bracket.

- Tax credits: which reduce the total amount owed to the government, such as education credits.

- Advance payments and withholdings: which include taxes withheld from salaries or payments made during the year.

Read Also: What Are Contingent Liabilities in Accounting?

What Are Tax Liabilities on W2?

The tax liabilities on Form W2 indicate the amount of federal, state, and other taxes withheld directly from an employee's paycheck during the tax year.

W2 is an essential document because it shows the total taxes withheld that have already been paid by the employer, such as income tax and social security contributions.

This form is crucial to the tax filing process because it compares the total taxes withheld with the actual amount paid. Therefore, it plays a vital role in clarifying the amount paid upfront and whether the taxpayer owes additional amounts or is eligible for a refund.

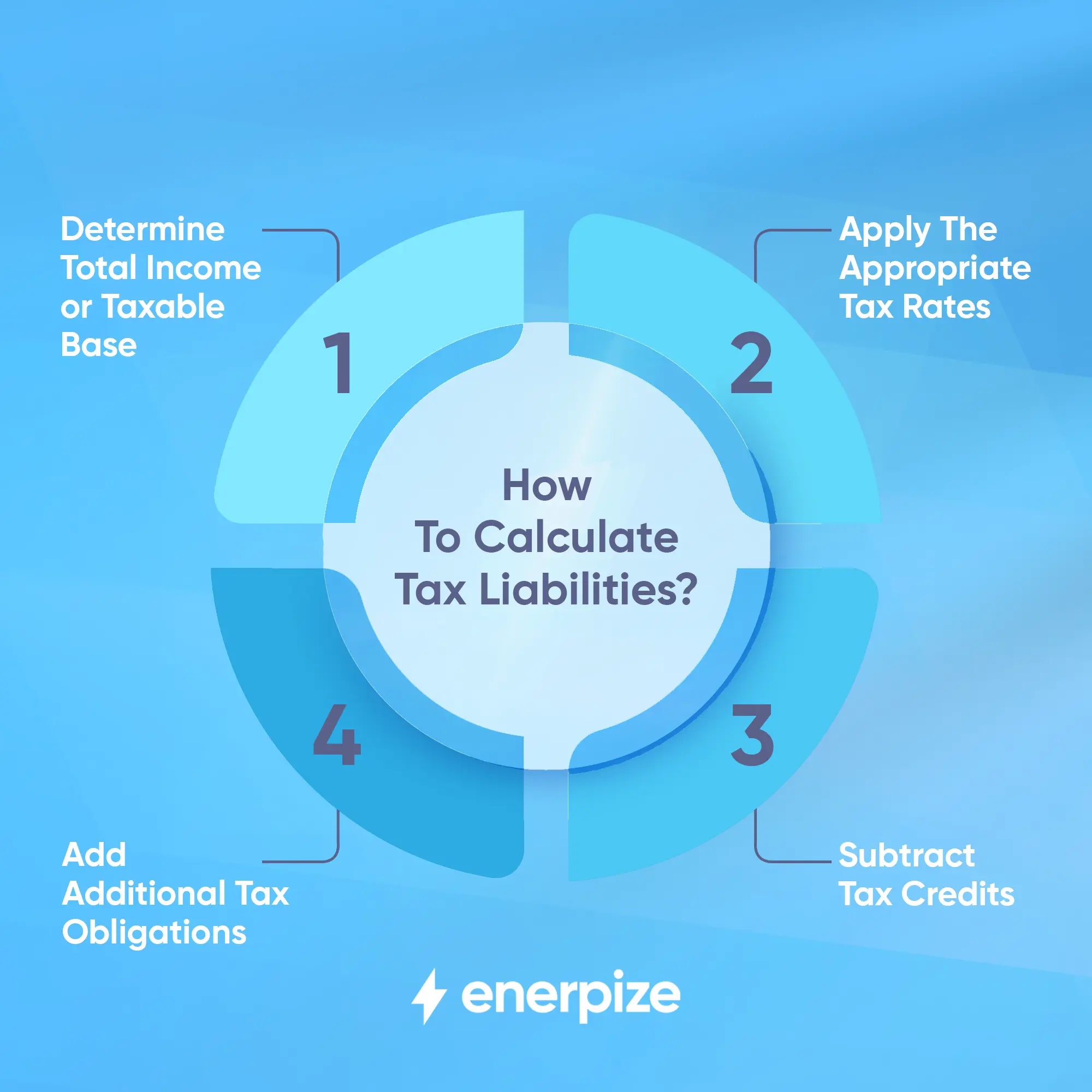

How To Calculate Tax Liabilities

Calculating your tax liability may seem complex, but it becomes manageable when broken into clear steps. Here's a simple breakdown of the process:

1- Determine Total Income or Taxable Base

First, add up all sources of income, including salaries, bonuses, profits, and returns from the company, and then subtract the allowed deductions to arrive at taxable income.

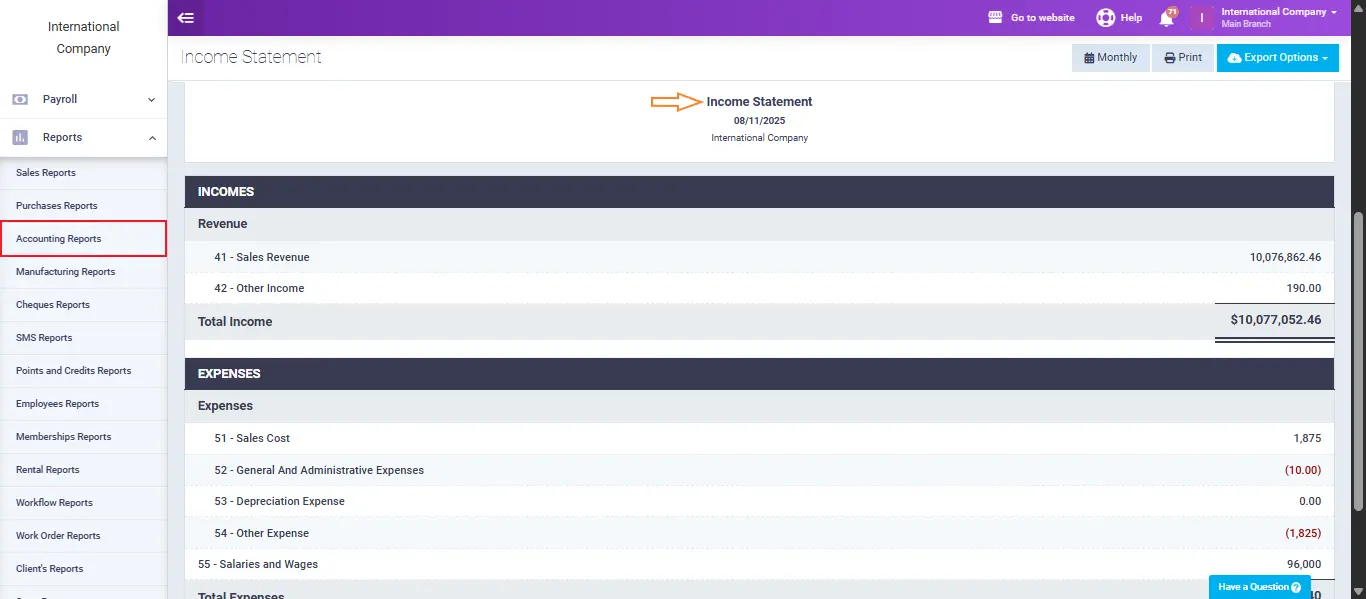

Enerpize centralizes your income and expense records, allowing you to instantly generate an income statement that clearly shows the net profit, helping to confirm the taxable income before applying deductions.

You can use: Google Sheets Income Statement Template

The result — your taxable income before credits are applied — is the basis for calculating your gross tax liability.

2- Apply the Appropriate Tax Rates

In a progressive tax system, taxable income is taxed across brackets. For example, income is taxed at 10% up to a threshold, then 12%, 22%, and so on as income rises. The tax owed is the sum calculated by applying each bracket’s rate to the income in that range.

Here, you should distinguish between two concepts:

- The marginal tax rate: the percentage of tax paid on the last portion of income earned.

- The effective tax rate: the average tax paid on income.

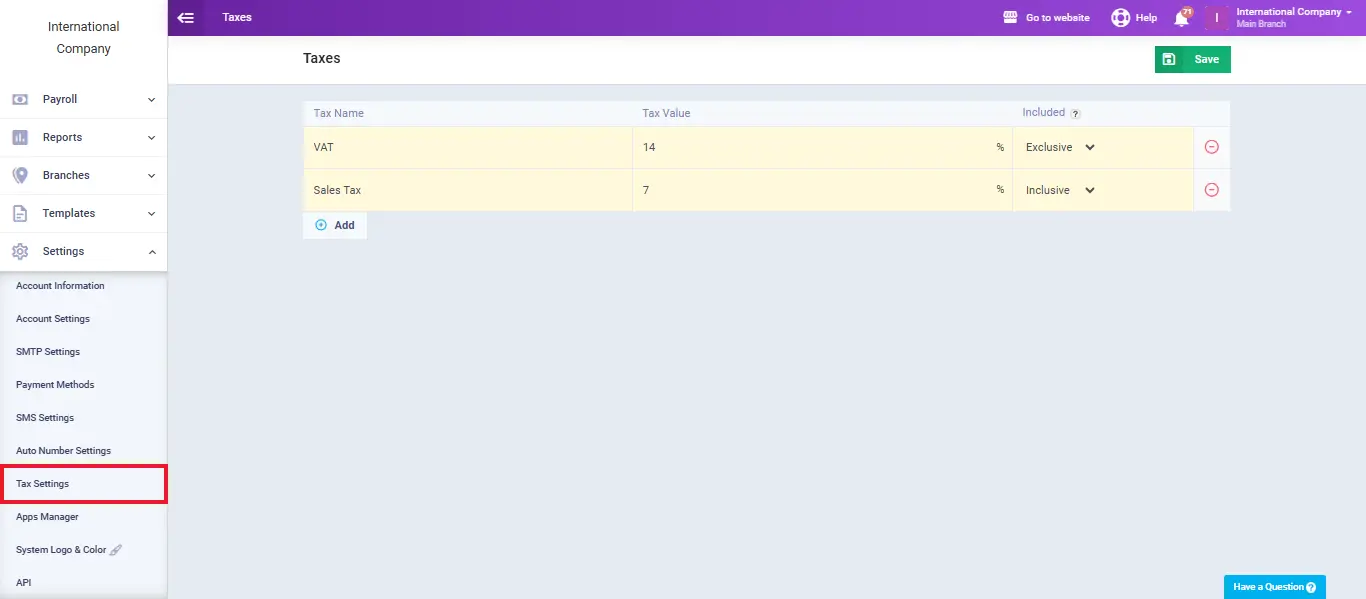

You can set up tax rates within Enerpize, which are then automatically applied to invoices and related transactions.

3- Subtract Tax Credits

After computing gross tax based on brackets, reduce that amount by any applicable tax credits, which directly lower your tax owed dollar-for-dollar, including education credits, child tax credit, or energy incentives.

Deductions reduce taxable income before tax calculation, while tax exemptions reduce the tax due directly.

4- Add Additional Tax Obligations

Include other taxes such as payroll taxes, self-employment taxes, alternative minimum tax (AMT), or deferred tax liabilities, if applicable.

Examples:

- Self-employment tax applies to self-employed individuals and includes contributions for social security and healthcare.

- The Alternative Minimum Tax (AML) is an additional tax scheme that ensures certain high-income earners pay a minimum amount of tax.

- Capital gains tax is a tax levied on the sale of assets and stocks.

Enerpize’s payroll module automatically records payroll-related liabilities and integrates them into your overall accounting records.

Full Worked Example

A small business owner has the following for the tax year:

| Item | Amount |

|---|---|

| Gross Revenue | $120,000 |

| Business Expenses (deductible) | $35,000 |

| Taxable Income | $85,000 |

Applying 2024 US federal tax brackets (single filer):

- First $11,600 at 10% = $1,160

- $11,601 to $47,150 at 12% = $4,266

- $47,151 to $85,000 at 22% = $8,327

Gross Tax Liability: $13,753

Less: Child Tax Credit ($2,000) = Net Tax Liability: $11,753

Less: Quarterly estimated payments already made ($8,000) = Tax Owed at Filing: $3,753

You may also like: How to Calculate Liabilities

Four steps to calculate tax liability — or let Enerpize do it automatically. Income, rates, credits, payroll taxes — calculated, tracked, and reported in one place. Start for free.

How to Estimate Tax Liability for the Year?

Tax liabilities are estimated using these steps:

- Add up all sources of income for the year, or any other taxable income.

- Deduct all allowed expenses and allowances to arrive at taxable income.

- Subtract any tax credits to reduce the tax due.

- Subtract any withholdings or advances.

- Determine whether there is any additional amount due or a refund.

Tax Liability vs Tax Owed vs Tax Refund

These three terms are often confused, although each has a different meaning in a tax context. Understanding the differences between them is fundamental to reading your tax return correctly and making better financial decisions.

Tax Liability:

This is the total amount of taxes an individual or company owes for a specific period, before any payments or adjustments are made.

Tax Owed:

This is the amount that should be paid to the tax authority when filing your tax return. It is calculated after deducting any previously paid taxes or payments.

Tax Refund:

This occurs when the tax payments made are greater than the actual tax liability, and the tax authority is entitled to a refund of the difference.

| concept | Definition | When will it happen? |

| Tax Liability | This is the total income tax before any deductions. | When calculating taxes for the first time |

| Tax Owed | This is the amount payable after deducting payments. | When filing a tax return |

| Tax Refund | This is the amount refunded to the taxpayer if the actual tax liability exceeds the stated amount. | Upon completion of tax settlement |

Where to Find Tax Liability on Form 1040?

The tax liability can be clearly defined on Form 1040 under the "Tax and Credits" section, on line 24.

This line represents the total tax due for an individual for the tax year, after accounting for taxable income and applying all tax credits. This figure serves as the baseline for all other calculations on the tax return.

When determining tax liability, it is compared with the total tax payments made, such as payroll deductions or advances. Based on this comparison, the final result is determined: either an amount owed to the government or a tax refund.

In other words, the tax liability on Form 1040 does not necessarily reflect the final amount to be paid or refunded, but rather the baseline tax amount before adjustments and payments.

How To Reduce Tax Liability?

Individuals and businesses can legally reduce their tax liabilities through various strategies. It's crucial to distinguish between these strategies, as some reduce the effective tax liability, while others aim to improve timing or cash flow management.

1- Strategies that reduce the effective tax liability

Deducting all expenses

Make sure to deduct all allowable expenses related to your business or personal finances. These may include business costs, home office expenses, medical bills, or educational expenses, which can significantly lower your taxable income.

Explore more on this topic: How to Track Business Expenses, or simplify the process with our ready-to-use Excel Tax Deduction Template.

Utilize Tax Credits

Tax credits reduce your actual tax bill, not just your income. Credits such as the earned income tax credit, R&D credits, or energy efficiency incentives can directly lower the amount you owe.

Contribute to Retirement Plans

Contributions into retirement accounts like a 401(k) or IRA not only prepare you for the future but also reduce your current taxable income, helping lower your tax burden now.

Defer Income

If possible, you can delay receiving certain income until the next tax year. This strategy can be useful in managing your tax bracket and keeping your liability lower in the current year.

Use Depreciation Strategies

Businesses can take advantage of accelerated depreciation methods to write off the cost of assets more quickly, lowering taxable income in the earlier years of asset use.

Work with a Tax Professional

A qualified tax advisor can help you identify tax-saving opportunities, ensure compliance, and implement effective strategies tailored to your financial situation.

2- Strategies for Improving Cash Flow and Planning

These strategies are not intended to reduce the total tax burden, but rather to help manage payment timing and improve cash flow.

- Deferring some revenue to the next tax year helps manage the tax bracket in the current year and improve cash flow.

- Consulting a tax expert can help improve financial planning, avoid mistakes, and develop payment strategies that suit the financial situation.

Recommended for you: What Is Accrued Liability for Small Business: A Detailed Guide

Common Mistakes When Calculating Tax Liability:

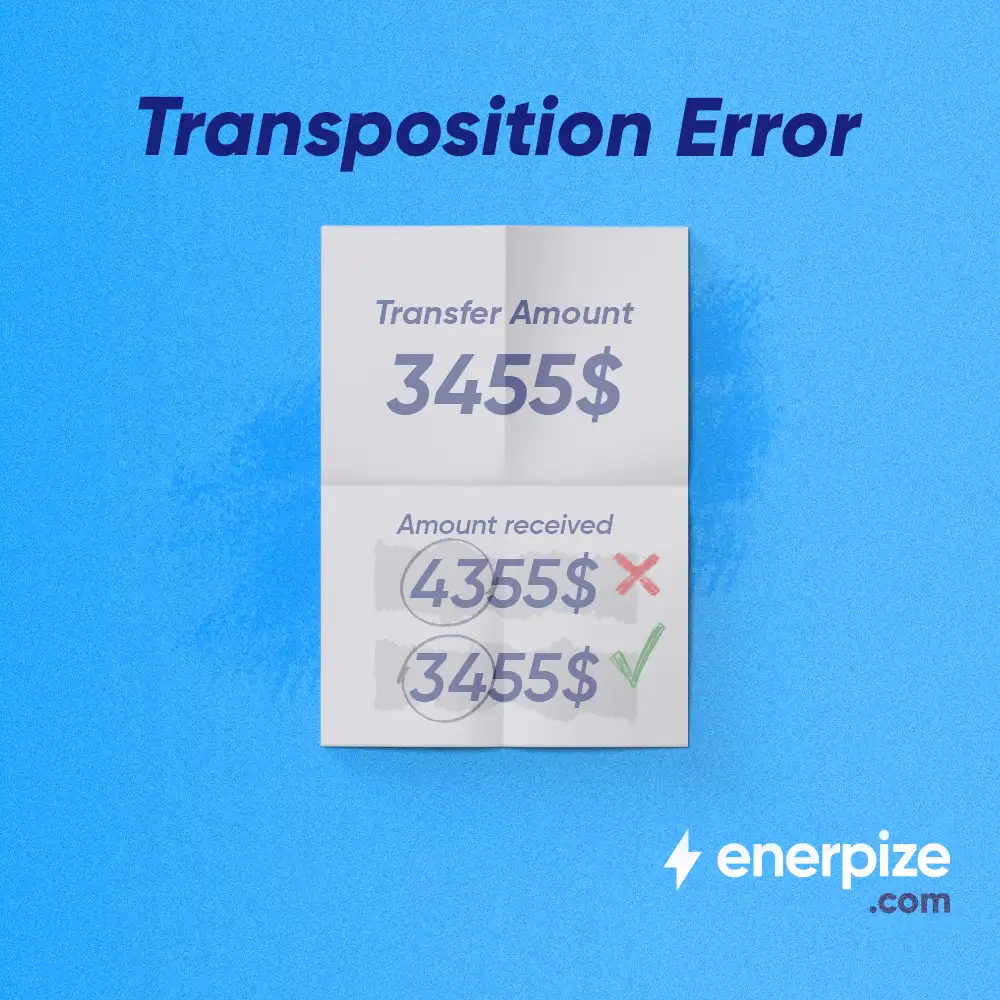

Many individuals and businesses may encounter difficulties when calculating their tax liability, which can lead to inaccurate estimates or various problems with tax authorities. Some of the most common mistakes include:

- Neglecting certain income sources, such as self-employment or investment income, can lead to an inaccurate underestimation of tax liability.

- Calculating tax on total income without deducting exemptions and allowed deductions.

- Failing to account for deductions such as operating expenses and personal exemptions, which can inflate the tax liability.

- Calculating tax liability based on outdated tax brackets or rates can lead to significant errors, especially when tax laws change.

- Neglecting to account for advance tax payments results in an inaccurate final amount.

Wrong rates, missed deductions, forgotten income — these mistakes cost businesses every year. Enerpize automates your tax calculations so the numbers are always right. Start for free.

Streamline Tax Liabilities Calculating With Enerpize

Enerpize online accounting management software is designed to help businesses manage their operations efficiently. It offers integrated tools for accounting, invoicing, HR, inventory, and more, all in one centralized system.

Enerpize simplifies the process of calculating tax liabilities by automating tax calculations across income, sales, and payroll transactions. With built-in tax rules and customizable settings, the system ensures accuracy while minimizing manual errors.

Enerpize automatically tracks taxable income, applies the correct tax rates, and generates detailed reports, helping businesses stay compliant and save valuable time during tax seasons.

FAQs About Tax Liabilities

What Are Tax Liabilities on W4?

On a W-4 form, tax liabilities relate to how much tax you expect to owe for the year. The information you provide, such as dependents and other income, helps your employer calculate how much tax to withhold from your paycheck to cover that liability.

How Do I Know If I Have Tax Liabilities?

You can check your tax liability by reviewing your income, deductions, and tax payments. If the taxes you owe exceed what’s been paid or withheld, you have a tax liability. You can also verify this when filing your tax return or by checking your IRS account online.

What Happens If I Don't Pay Tax Liability?

If you don’t pay your tax liability, you may face penalties, interest charges, wage garnishments, or even legal action by tax authorities. It’s important to pay on time or arrange a payment plan with the IRS or your local tax agency.

Where Can I Find Tax Liabilities?

You can find your tax liabilities on your tax return summary, through IRS or local tax authority portals, or within accounting software like Enerpize that tracks and reports taxes owed for your business.

What Does Tax Liabilities Mean?

Tax liabilities refer to the total amount of taxes a person or business owes to the government. This includes income tax, sales tax, payroll tax, and other applicable taxes based on earnings or operations.

Do I Have Tax Liabilities?

If you earn income, sell taxable goods or services, or run a business, you likely have tax liabilities. The exact amount depends on your financial activity and the tax rules that apply to your situation.

What Are My Tax Liabilities?

Your tax liabilities include any unpaid taxes for the current or previous tax years. They can be calculated by totaling the taxes you owe after applying deductions, credits, and payments already made.

How Do I Know If I Have No Tax Liability?

You have no tax liability if your total tax owed is zero or if your tax credits and withholdings fully cover what you owe. This can be confirmed when filing your tax return or through your tax software/account.

Does everyone have tax liability?

No, not everyone bears direct tax responsibility, but they do bear indirect tax responsibility through consumption taxes.

Calculating tax liabilities is easy with Enerpize.

Try Enerpize accounting software to calculate tax liabilities accurately.

Calculating tax liabilities is easy with Enerpize.

Try Enerpize accounting software to calculate tax liabilities accurately.