Author : Madonna Adel

What Is a Trial Balance: A Comprehensive Guide

Table of contents:

- Key Takeaways

- What Is a Trial Balance?

- What Does The Trial Balance Include?

- Trial Balance Example

- Importance of Using the Trial Balance

- What are The Purposes of The Trial Balance?

- Who Uses a Trial Balance?

- What are The Three Types of Trial Balance?

- How To Prepare a Trial Balance?

- Common Accounting Errors When Preparing a Trial Balance

- How to Avoid Trial Balance Errors?

- Trial Balance VS Balance Sheet

- Simplify Creating a Trial Balance with Enerpize

- FAQs

Even the most skilled accountants can make mistakes. Accounting errors come from basic bookkeeping issues. When those errors go unnoticed, they can create stress and potentially harm a business. That’s why tools that help catch mistakes early are so important—and one of the most effective is the trial balance.

So, what exactly is a trial balance, and how is it prepared? Having a clear understanding of the trial balance sheet can help minimize accounting errors and reduce the pressure of managing your books.

Key Takeaways

- A trial balance is an internal accounting report that summarizes all general ledger account balances at a specific point in time, ensuring that total debits equal total credits.

- It plays a critical role in detecting bookkeeping errors early, helping businesses correct issues before preparing financial statements.

- A trial balance is typically presented in a three-column format: account name, debit balance, and credit balance.

- There are three types of trial balances—unadjusted, adjusted, and post-closing—each prepared at different stages of the accounting cycle for specific purposes.

- While a trial balance confirms mathematical accuracy, it does not detect all errors, such as omissions or principle-based mistakes.

- The trial balance serves as the foundation for preparing financial statements, including the income statement and balance sheet.

- A trial balance is not the same as a balance sheet; it is an internal checkpoint, whereas the balance sheet is a formal financial statement prepared according to accounting standards.

- Using reliable accounting software and regular reviews can significantly reduce trial balance errors and improve overall financial accuracy.

What Is a Trial Balance?

A trial balance is an accounting report that summarizes the balances of all general ledger accounts at a specific point in time. It presents each account’s balance in two columns, debits and credits, to verify that total debits equal total credits, as required under double-entry accounting.

By confirming this balance, the trial balance helps ensure that transactions were recorded accurately and that no mathematical errors occurred. It is usually prepared at the end of a reporting period, before formal financial statements such as the income statement and balance sheet, allowing any errors to be identified and corrected in advance.

What Does The Trial Balance Include?

A trial balance in accounting is a structured report that aggregates all general ledger accounts for a specific reporting period and presents their balances in a clear, summarized format.

It includes key details such as account names (and sometimes account numbers), the reporting period, individual debit or credit balances for each account, and the total debits and total credits for the period.

The trial balance format presents the report in a clear three-column layout.

1- Account Names

Listing only the accounts that had activity during the period, such as cash, accounts receivable, accounts payable, revenue, and expenses.

2- Debit Balances

These commonly include assets and expenses.

3- Credit Balances

Which usually include liabilities, equity, revenue, gains, and losses.

Unlike the general ledger, which records every individual transaction in detail, the trial balance shows only the total debit or credit balance for each account. Its purpose is to confirm that the sum of all debit balances equals the sum of all credit balances.

If these totals do not match, it indicates a bookkeeping error that must be identified and corrected before preparing financial statements.

Explore more on this topic: Trial Balance VS General Ledger: Key Differences

Trial Balance Example

This table provides a practical example of a trial balance for a business during a specific reporting period. It includes three main columns: Account Name, Debit Balances, and Credit Balances.

Each account shows its total balance in the appropriate column (debit or credit) without listing individual transactions. The accounts included are Cash, Accounts Receivable, Accounts Payable, Revenue, Expenses, and Equity.

| Account name | Debit | Credit |

| Cash | $4000 | |

| Accounts Receivable | $10000 | |

| Accounts Payable | $5000 | |

| Revenue | $6000 | |

| Expenses | $7000 | |

| Equity | $10000 | |

| Total | $21000 | $21000 |

In this example, the total debits ($21,000) equal the total credits ($21,000), indicating that the accounts are balanced and no obvious bookkeeping errors exist. This confirms that the financial transactions have been recorded correctly up to this point.

With Enerpize accounting software, a trial balance can be prepared quickly and accurately. The software also reduces data entry and calculation mistakes, making it a reliable tool to ensure all accounts are balanced and to identify any discrepancies in the books.

Importance of Using the Trial Balance

A trial balance is more than just a bookkeeping tool—it’s a key step in keeping your financial records accurate and organized. Summarizing all account balances in a clear, structured format helps businesses detect errors early, save time during audits, and ensure the reliability of financial statements.

The following points highlight the main benefits of using a trial balance:

1- Simplifies Bookkeeping Review

The clear, organized layout makes it easy for anyone—whether experienced or new to accounting—to understand and check account balances quickly.

2- Helps Spot Errors Quickly

By comparing total debits and total credits, unbalanced entries or missing transactions can be identified early, preventing bigger issues later.

3- Saves Time During Audits

Provides a concise overview of accounts, enabling auditors or business owners to identify arithmetic errors before reviewing detailed records.

4- Ensures Accuracy of Financial Records

Helps confirm that all transactions follow double-entry accounting rules, reducing the chance of mistakes in financial data.

5- Supports Financial Reporting

Acts as a foundation for preparing key reports such as the income statement and balance sheet, which are critical for decision-making, funding, and business planning.

6- Verifies Completeness of Entries

While it can’t detect every type of error (such as entries in the wrong account or missing transactions), the trial balance confirms that all debits and credits balance mathematically, providing confidence in the overall bookkeeping process.

Read Also: Statement Of Account: Definition and Examples

What are The Purposes of The Trial Balance?

The trial balance serves as a fundamental tool in accounting, designed to ensure that a company’s financial records are accurate and balanced. Beyond simply listing debits and credits, it helps detect errors, facilitates review and correction of accounts, and provides a reliable foundation for preparing financial statements.

The following points outline the key functions and purposes of a trial balance:

1- Preliminary Validation

A trial balance goes beyond simply listing debits and credits; it serves as an initial check of the accounts.

2- Error Detection

It helps accountants identify potential mistakes in recording or posting transactions.

3- Promotes Review and Correction

Any discrepancies or imbalances highlighted by the trial balance trigger a careful review of accounts and corrective actions.

4- Ensures Accurate Financial Statements

Addressing errors before finalizing reports supports the accuracy of financial statements.

5- Maintains Integrity of Reporting

This anticipatory function helps uphold the reliability and trustworthiness of the business’s financial information.

Who Uses a Trial Balance?

A trial balance helps give a quick overview of all account balances, making it easier to detect errors and maintain reliable financial information. The main users of a trial balance include:

- Accounting and bookkeeping professionals: For conducting internal audits or periodic reviews.

- Small business owners: To gain a clear overview of the company’s financial position.

- Senior management: To quickly understand the overall financial status of the business in one place.

What are The Three Types of Trial Balance?

A trial balance is not just a single report; businesses often prepare multiple trial balances throughout the accounting cycle to ensure their books are accurate at different stages. There are three main types of trial balances: unadjusted, adjusted, and post-closing.

While all three follow the same basic structure, each serves a distinct purpose in the accounting process, from checking initial entries to preparing financial statements and starting a new fiscal period.

1- Unadjusted Trial Balance

Format:

The unadjusted trial balance lists all general ledger accounts and shows debit and credit balances as recorded, without any adjustments. It follows the traditional three-column layout: Account Name, Debit, and Credit, with each account’s balance clearly displayed.

Usage:

It is prepared immediately after recording the period's transactions and serves as a “rough draft” of the financial records. It helps catch immediate errors and ensures that debits and credits are aligned before making adjusting entries. It also serves as a starting point for analyzing accounts before adjustments.

2- Adjusted Trial Balance

Format:

The adjusted trial balance maintains the same basic layout but includes all adjustments, such as accruals, depreciation, and corrections to previous entries. It shows the final debit and credit balances for each account, providing an updated and accurate snapshot of the books.

Usage:

It is prepared after completing all adjusting journal entries and forms the basis for preparing official financial statements, such as the income statement and balance sheet. It ensures that all accounts reflect the accurate final balances for the reporting period.

3- Post-Closing Trial Balance

Format:

The post-closing trial balance follows the traditional three-column layout but focuses only on permanent accounts, such as assets, liabilities, and equity, excluding temporary accounts like revenues and expenses. It clearly shows the balances of these accounts, confirming that everything is in order before the new accounting period begins.

Usage:

It is prepared after all temporary accounts are closed at the end of the accounting period. It confirms that all debits and credits are balanced and that the books are ready for the new fiscal year, serving as the opening trial balance for the next accounting cycle.

Recommended for you: Chart Of Accounts: Definition & Examples

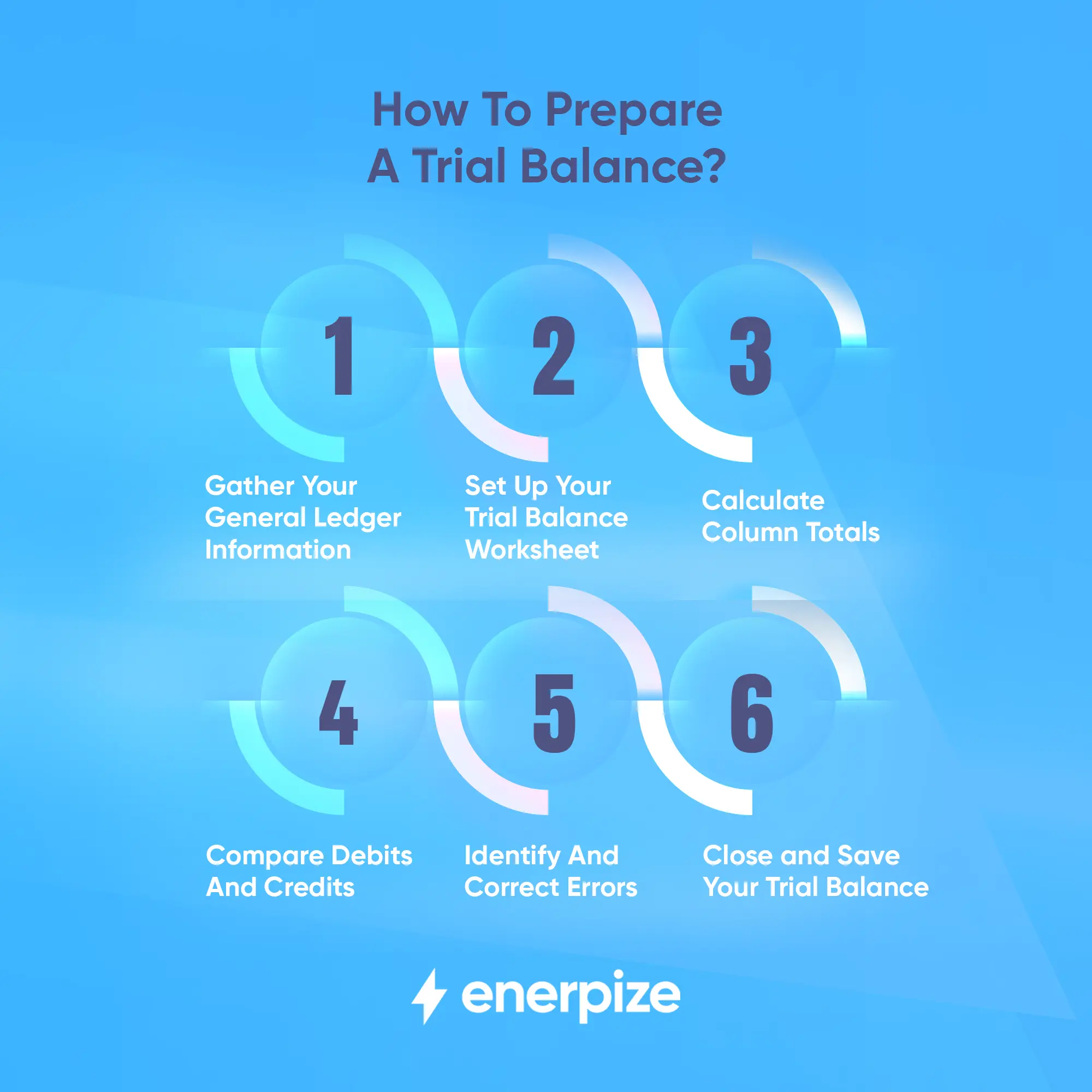

How To Prepare a Trial Balance?

Preparing a trial balance is a straightforward process once you understand the steps. The trial balance helps ensure that your books are accurate and that all debits and credits are correctly recorded. Here’s how to prepare one:

1- Gather Your General Ledger Information

Start by collecting information from your general ledger. You don’t need every individual transaction, only the account names and their closing balances for the period you are reviewing. This could be a month, a quarter, or any other defined accounting period.

Make sure to total any sub-accounts or multiple entries for the same account, such as multiple invoices in accounts payable.

2- Set Up Your Trial Balance Worksheet

Create a worksheet with three columns: Account Name, Debit, and Credit. Transfer the closing balances from your general ledger to this worksheet, ensuring each account matches the ledger exactly.

Enter the total debit amounts in the debit column and the total credit amounts in the credit column. Accuracy is key here—recording an amount in the wrong column or account will affect the trial balance totals.

3- Calculate Column Totals

Once all account balances are entered, sum the debits to find the debit total and the credits to find the credit total. If you are using spreadsheet software like Microsoft Excel, formulas can make this process faster and reduce the risk of calculation errors.

4. Compare Debits and Credits

Check whether the total debits equal the total credits. If they match, your trial balance is balanced, indicating that your books are mathematically correct. If they do not match, the discrepancy shows that there is an error somewhere in the accounts that needs to be found and corrected.

5. Identify and Correct Errors

If the debits and credits don’t match, review your entries carefully. Common mistakes include entering amounts in the wrong column, omitting an account, or totaling balances incorrectly. Once you find the error, correct it and recalculate the totals. Repeat this process until both columns are equal.

6. Close and Save Your Trial Balance

Once you confirm the trial balance is balanced, you can close the worksheet. Save it for your records, as it may be useful for future reference or financial statement preparation. If you are using spreadsheet software, keeping a template with formulas can save time for future trial balances.

To make the process even easier, you can use the free Enerpize trial balance template.

Common Accounting Errors When Preparing a Trial Balance

A trial balance is a useful tool for checking the mathematical accuracy of your accounts, ensuring that total debits and credits match. However, it is not foolproof—Mistakes can still exist. Studies indicate that 59% of accountants make multiple errors each month.

These errors, known as trial balance errors, can be broadly divided into those detected by the trial balance and those not detected (undetectable errors).

1- Errors Disclosed by a Trial Balance

These occur when total debits and credits do not balance, immediately signaling an issue. Common causes include:

- Simple data entry mistakes

- Posting transactions in the wrong column

- Missing entries or miscalculations

The trial balance helps identify these issues so they can be corrected before preparing financial statements.

2- Errors Not Disclosed by a Trial Balance (Undetectable Errors)

Some errors do not affect the equality of debits and credits. These are limitations of the trial balance and include:

- Error of Omission: A transaction is completely skipped and not recorded in the journal or ledger.

- Error of Original Entry: Both sides of a double-entry transaction include the wrong amounts.

- Error of Reversal: The amounts are correct, but the debit and credit accounts are swapped.

- Errors of Principle: Transactions violate accounting principles, such as treating capital expenditure as revenue expenditure or vice versa.

- Errors of Commission: The amount is correct, but it is posted to the wrong account. This is usually due to oversight, unlike principal mistakes, which result from misunderstanding accounting rules.

- Compensating Errors: A wrong entry in one account is offset by an incorrect entry of the same amount in another account, masking the mistake in the trial balance.

You may also like: What Is a Profit and Loss Statement? With Examples

How to Avoid Trial Balance Errors?

Avoiding accounting errors in a trial balance is essential to maintaining accurate financial records and ensuring reliable financial statements. Here are some effective strategies:

1- Use Reliable Accounting Software

Tools like Enerpize reduce calculation and data-entry errors and make preparing a trial balance easier.

2- Review Accounts Regularly

Periodically check account records to ensure all transactions are accurately recorded.

3- Enter Transactions Carefully

Double-check amounts, accounts, and debit/credit placement for each entry.

4- Segregate Responsibilities

Have another person review the trial balance to catch undetectable errors.

5- Continuous Training

Ensure accounting staff understand accounting principles to avoid principle-based mistakes.

6- Use Ready-Made Templates

Leveraging free trial balance templates can save time and reduce manual errors.

Understanding both detectable and undetectable errors, and how to prevent them, ensures accurate financial records and makes the trial balance a more effective tool for managing accounts.

Trial Balance VS Balance Sheet

Understanding the difference between a trial balance and a balance sheet is essential for accurate financial reporting. While both are key accounting tools, they serve distinct purposes at different stages of the accounting cycle.

The comparison below highlights how each report is used, who relies on it, and its role in presenting and verifying a company’s financial information.

| Feature | Trial Balance | Balance Sheet |

| Purpose | To verify if the total debits and credits of all ledgers are balanced, which helps detect accounting errors | To show the financial position of a company, including assets, liabilities, and equity, demonstrates the accuracy of the finances |

| Scope | Records all closing balances of general ledger accounts | Records assets, liabilities, and equity of the company |

| Users | Internal use within the company | Internal and external users, including investors, stakeholders, and auditors |

| Frequency | Can be prepared monthly, quarterly, or as needed | Prepared at the end of every financial year |

| Legal/official status | Not a financial statement; no auditor signature required | It is a financial statement; it requires an auditor's signature |

| Format | Accounts are divided into debit and credit balances; no strict rules for arrangement | Accounts are divided into assets, liabilities, and equity; arranged according to accounting standards (GAAP/IFRS) |

| Role in financial reporting | Helps ensure ledger accuracy; serves as the base for preparing financial statements | Part of the final accounts, used to assess financial health and net worth |

| Standards | Follows double-entry bookkeeping rules | Prepared according to accounting standards like GAAP or IFRS |

In summary, the trial balance serves as an internal control to verify the accuracy of ledger accounts before financial statements are prepared. In contrast, the balance sheet provides a formal, standardized snapshot of a company’s financial position.

Recognizing how these two reports complement each other helps ensure reliable accounting records and supports better financial analysis and decision-making.

Simplify Creating a Trial Balance with Enerpize

Enerpize accounting software makes creating a trial balance fast, accurate, and stress-free by automating core accounting processes in one cloud-based system. Every transaction recorded in sales, expenses, assets, inventory, and payroll is automatically posted to the general ledger and chart of accounts, eliminating manual data entry and reducing accounting errors.

With built-in journaling, real-time reporting, and organized debit and credit tracking, Enerpize allows you to generate a trial balance instantly at any point in the accounting cycle.

Because Enerpize is modular and customizable for more than 50 industries, your trial balance is always aligned with your business structure, cost centers, and reporting needs.

Whether you’re preparing internal checks, supporting audits, or getting ready for financial statements, Enerpize ensures your trial balance is accurate, up to date, and ready with just a few clicks—no complex setup, no extra tools, and no risk of manual mistakes.

FAQs

What is an adjusted trial balance?

An adjusted trial balance is a trial balance prepared after all adjusting journal entries have been recorded. These adjustments may include accruals, depreciation, or corrections. It shows the final, accurate debit and credit balances for all accounts and serves as the basis for preparing financial statements, such as the income statement and balance sheet.

What is an unadjusted trial balance?

An unadjusted trial balance is prepared before any adjustments are made. It lists all general ledger accounts, including their debit and credit balances, exactly as recorded after regular transactions. It serves as a preliminary check to ensure debits and credits match before making adjustments.

What does a trial balance look like?

A trial balance is typically shown in a three-column format:

- Account Name

- Debit Balance

- Credit Balance

Each account appears once, with its total balance placed in either the debit or credit column. At the bottom, total debits must equal total credits.

What is a post-closing trial balance?

A post-closing trial balance is prepared after all temporary accounts (revenues, expenses, gains, and losses) have been closed. It includes only permanent accounts such as assets, liabilities, and equity. Its purpose is to confirm that the books are balanced and ready for the next accounting period.

What does a trial balance show?

A trial balance shows:

- All general ledger account balances

- Whether total debits equal total credits

- A summarized snapshot of account balances at a specific point in time

It helps confirm mathematical accuracy and detect basic bookkeeping errors.

How to read a trial balance?

To read a trial balance:

- Review the list of account names.

- Check whether each account has a balance in the correct column (debit or credit).

- Compare the total debits and total credits at the bottom.

- If totals are equal, the books are mathematically balanced; if not, errors exist that need correction.

Is a trial balance the same as a balance sheet?

No, a trial balance and a balance sheet are not the same.

- A trial balance is an internal report used to verify that debits and credits are balanced.

- A balance sheet is a formal financial statement that presents assets, liabilities, and equity and follows accounting standards such as GAAP or IFRS.

The trial balance is prepared before the balance sheet and helps ensure its accuracy.

In conclusion, the trial balance is a vital accounting tool that helps ensure the accuracy and reliability of financial records. Summarizing all ledger account balances and confirming that total debits equal total credits allows businesses to detect errors early and prepare financial statements with confidence.

Whether prepared manually or using accounting software, maintaining an accurate trial balance supports better financial control, smoother audits, and more informed business decisions.

Creating trial balance is easy with Enerpize.

Try Enerpize accounting software to automate generate your trial balance.

Creating trial balance is easy with Enerpize.

Try Enerpize accounting software to automate generate your trial balance.