Author : Haya Assem

Statement of Account: Definition, How to Prepare & Example

Table of contents:

- Key Takeaways

- Statement of Account Meaning

- What Is A Statement Of Account?

- Importance Of The Statement Of Account In Accounting

- What Should A Statement Of Account Include?

- How To Prepare A Statement Of Account?

- When Should You Send a Statement of Account?

- Statement Of Account Example

- Statement of Account Example — International Company to Retail Mart

- How To Read And Understand An Account Statement?

- Common Errors On A Statement Of Account

- How A Small Business Owner Uses A Statement Of Account?

- Statement Of Account Vs Invoice

- Statement of Account vs. Invoice vs. Receipt

- Statement Of Account Vs Balance Sheet

- Account Statement Vs Transaction History

- Streamline Statement Of Account With Enerpize

- FAQs

A statement of account — also referred to as a statement of accounts — is a financial document that provides a detailed summary of all transactions between a business and its customer over a specific period — typically one month. It shows every invoice issued, every payment received, any credits applied, and the resulting outstanding balance.

Unlike an invoice, which covers a single transaction, a statement of account covers the entire relationship for a period. It's used to prompt overdue payments, support reconciliation, and give both parties a clear, shared record of where the account stands. For a ready-to-use format, download our free statement of account template in Excel, Word, Google Sheets, and PDF.

Key Takeaways

- A statement of account is not the same as an invoice — it covers an entire period, not a single transaction

- It should include opening balance, itemized transactions, payments received, credits, and closing balance

- Most businesses send statements monthly — but high-volume suppliers may send bi-weekly

- A well-maintained statement of account can serve as supporting evidence in a payment dispute

- Accounting software like Enerpize generates statements automatically from invoice and payment records — no manual assembly required

Statement of Account Meaning

A statement of account is a formal summary document issued by a business to a client that records all financial activity between them over a defined period — typically one month. In accounting terms, it serves as a reconciliation tool, a payment reminder, and a dispute resolution reference all in one document.

What Is A Statement Of Account?

A statement of account definition is a financial document that provides a detailed summary of all transactions between a business and its customer over a specific period. It typically lists all invoices issued, payments received, credits, and any outstanding balances.

This statement helps both the business and the customer keep track of what has been billed and what remains unpaid, ensuring transparency and accurate account reconciliation. It’s commonly used as a reminder or reference for pending payments and serves as a reliable record for financial reviews or audits.

Need the document itself, not just the definition? Download our free statement of account template — Excel, Word, Google Sheets, and PDF, ready in 60 seconds. Download Free Template.

Importance Of The Statement Of Account In Accounting

The purpose of a statement of account in accounting is to maintain transparency and accuracy in financial records. It serves as an essential communication tool between a business and its customers or suppliers, ensuring both parties agree on the recorded transactions. In financial accounting, statements of account serve as primary source documents for reconciling accounts receivable and confirming period-end balances.

- Ensures accuracy in records: The statement of account helps verify that all invoices, payments, and credits are correctly recorded and balanced.

- Facilitates payment tracking: Businesses can easily identify overdue accounts and follow up on pending payments.

- Supports reconciliation: It simplifies the process of matching internal records with customer or supplier ledgers.

- Enhances transparency: By providing a clear breakdown of all transactions, it builds trust and reduces disputes.

- Aids financial reporting: Statements of account help accountants confirm balances and ensure reliable financial statements.

Enerpize Accounting Software helps ensure accuracy, transparency, and reconciliation by automatically updating customer balances and transaction records in real time.

What Should A Statement Of Account Include?

A statement of account should include all the key terminology on an account statement and key details that clearly summarize the financial relationship between a business and its customer or supplier. It provides a complete view of all transactions within a specific period.

A statement of account should include the following:

- Business and customer details: Names, addresses, and contact information of both parties.

- Statement period and date: The start and end dates of the transactions covered, along with the issue date of the statement.

- Invoice details: A list of all issued invoices, including invoice numbers, dates, and amounts.

- Payments received: Records of payments made by the customer and the dates they were received.

- Credits and adjustments: Any credit notes, discounts, or refunds applied to the account.

- Outstanding balance: The total amount due at the end of the statement period.

- Reference or statement number: For easy tracking and recordkeeping.

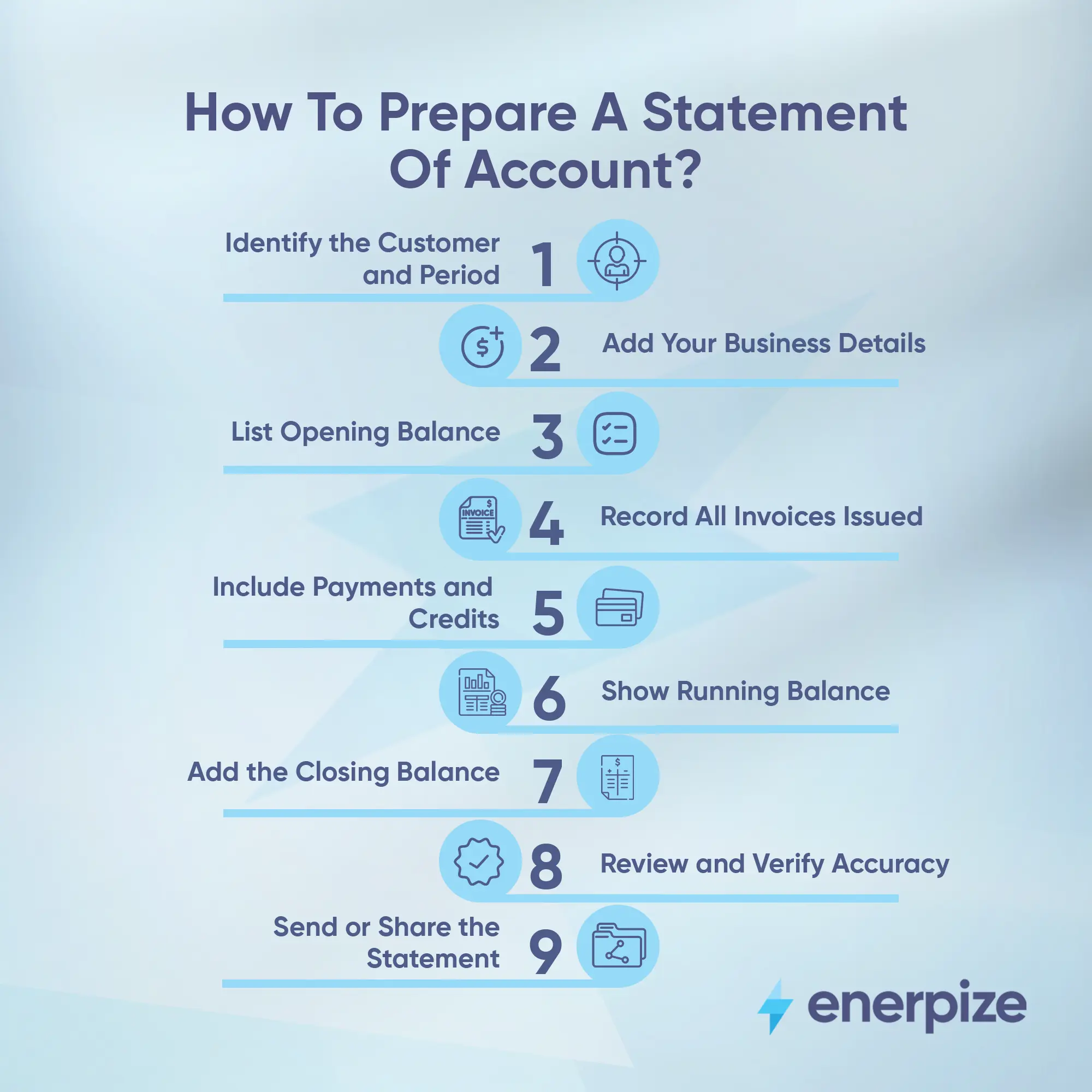

How To Prepare A Statement Of Account?

A statement of account summarizes all invoices, payments, and outstanding balances within a specific period, and helps resolve disputes and improve cash flow tracking.

The following steps will help you prepare a professional statement of account.

1- Identify the Customer and Period

Start by entering the customer’s name, contact details, and account number. Define the statement period, for example, to clearly specify which transactions are included.

2- Add Your Business Details

Include your company name, logo, address, and contact information at the top of the statement. This gives it a professional look and ensures your customer knows who the document is from.

3- List Opening Balance

If the customer has an outstanding balance from previous periods, record it as the opening balance. This helps track the total due amount from the start of the statement period.

4- Record All Invoices Issued

List every sales invoice issued to the customer within the statement period. Include the invoice number, date, description, and total amount. This section forms the core of the statement, showing all goods or services sold.

5- Include Payments and Credits

Record all payments received from the customer during the same period. Also include any credit notes, discounts, or returns to reflect accurate net balances.

6- Show Running Balance

After each transaction (invoice or payment), update the running balance. This makes it easy to see how each transaction affects the amount owed.

7- Add the Closing Balance

At the end of the statement, calculate the closing balance, the total amount the customer still owes (or the amount in credit, if applicable).

8- Review and Verify Accuracy

Double-check all entries to ensure no transaction is missing or duplicated. Accuracy is critical for maintaining customer trust and preventing disputes.

9- Send or Share the Statement

Once finalized, send the statement of account to the customer via email or through your accounting system.

To get started instantly, you can download the Enerpize-ready statement of account sample.

Still assembling statements manually every month? Enerpize generates client statements automatically from your invoice and payment records — no copy-paste, no reconstruction. Try Enerpize Free.

When Should You Send a Statement of Account?

Timing matters as much as content. Statements of account are a core tool in accounts receivable management — they consolidate outstanding invoices into a single client-facing document that accelerates collection.

Monthly — the standard

Most businesses issue statements at the end of the calendar month or the first business day of the following month. This aligns with typical billing cycles and gives clients a predictable schedule. Clients who know when to expect statements are more likely to have payments ready.

Before chasing overdue invoices

A statement of account is a professional, non-confrontational way to remind a client of outstanding balances before escalating to a formal follow-up. It shows the full picture — what was invoiced, what was paid, what remains — without the adversarial tone of a direct payment demand.

When a client requests a reconciliation

If a client queries a balance or disputes a charge, a current statement is the fastest way to resolve it. Both parties can see the same transaction record and identify where the discrepancy occurred.

At the start of a new credit relationship

When you first extend credit to a new client, issuing a statement after the first month establishes the format and cadence early — before there's any outstanding balance to chase.

When you have multiple outstanding invoices

If a client has three or more unpaid invoices at different stages of overdue, a consolidated statement is cleaner and more actionable than forwarding each invoice individually.

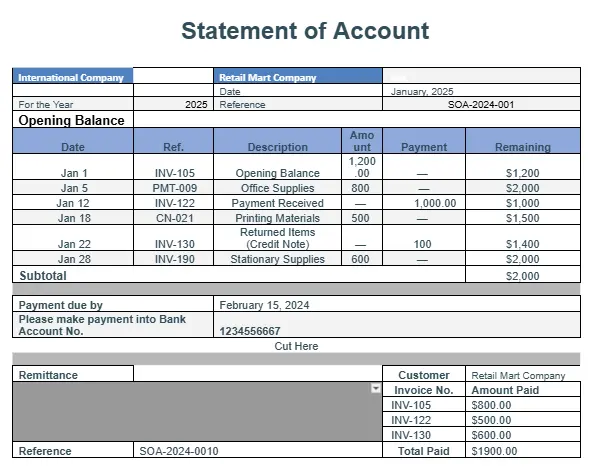

Statement Of Account Example

To better understand how a statement of account works, here’s a sample showing how transactions, payments, and outstanding balances appear over a specific period.

This example illustrates a business (International Company) issuing a statement to a customer (Retail Mart Company) summarizing all invoices, payments, and returns for January 2025.

Statement of Account Example — International Company to Retail Mart

Period: January 1, 2025 to January 31, 2025

| Date | Reference | Description | Debit (Amount Due) | Credit (Payment Received) | Balance |

|---|---|---|---|---|---|

| Jan 1, 2025 | Opening Balance | $1,200.00 | |||

| Jan 5, 2025 | INV-0041 | Product Delivery — Order #112 | $3,500.00 | $4,700.00 | |

| Jan 10, 2025 | PMT-0089 | Payment Received — Thank You | $1,200.00 | $3,500.00 | |

| Jan 18, 2025 | INV-0045 | Consulting Services — January | $1,800.00 | $5,300.00 | |

| Jan 22, 2025 | CN-0012 | Credit Note — Returned Goods | $300.00 | $5,000.00 | |

| Jan 31, 2025 | Closing Balance | $5,000.00 |

Total Invoiced: $5,300.00 | Total Received: $1,500.00 | Amount Due: $5,000.00

How To Read And Understand An Account Statement?

A statement of account may look detailed, but once you understand its structure, it becomes an invaluable tool for financial clarity.

1- Header Section

Found at the top of the statement, it includes your business name, contact details, and the statement period. This confirms that you’re reviewing the correct account within the right timeframe.

2- Customer or Supplier Information

Displays the customer’s or supplier’s name, account number, and address, ensuring all listed transactions belong to the correct party.

3- Opening Balance

Shows how much was owed or due at the beginning of the statement period. It serves as the starting point for all subsequent financial movements.

4- Transaction Details

This main section lists each transaction during the statement period, including dates, references, descriptions, debit and credit amounts, and a running balance. It allows you to see how invoices, payments, and credit notes affect the overall balance.

5- Closing Balance

Summarizes the total amount still owed or due at the end of the statement period, reflecting all payments and adjustments made.

6- Payment Instructions

Bank details, accepted payment methods, and the payment due date. Every statement should include these even for long-standing clients — making payment frictionless is the single most effective way to accelerate settlement.

7- Remittance Section

A detachable slip at the bottom the client can return with their payment, confirming which invoices they're paying and the total amount. It speeds up reconciliation on both sides — the client knows exactly what they're paying for, and you know exactly which invoices to mark as settled.

Related Post: What Is a Profit and Loss Statement? & How to Make?

Common Errors On A Statement Of Account

Misallocated payments and duplicate entries are among the most common accounting errors in statement preparation — and the hardest to trace once a period has closed. Mistakes can occur when preparing a statement of account, even with careful bookkeeping. These errors can lead to inaccurate balances, customer disputes, or even payment collection delays. Understanding the most common mistakes and knowing how to prevent them helps maintain accuracy, trust, and smooth financial operations.

Below are the most common errors that might occur while preparing a statement of account and how to avoid each:

1- Incorrect Opening or Closing Balances

One of the most frequent mistakes is starting with an inaccurate opening balance or ending with an incorrect closing figure.

How to avoid: Always reconcile your records with the previous statement before issuing a new one to ensure continuity and accuracy.

2- Missing or Duplicate Transactions

Omitting invoices or recording the same payment twice can distort the true balance.

How to avoid: Cross-check each transaction against your accounting system or bank records before finalizing the statement.

3- Wrong Customer or Account Details

Sending a statement with the wrong name or account number can create confusion and delay payments.

How to avoid: Verify customer information before generating or sending the statement.

4- Missapplied payments or credit notes

Sometimes, payments are recorded against the wrong invoices, leading to discrepancies in outstanding balances.

How to avoid: Always match payments with the correct invoice reference numbers to maintain accuracy.

5- Unrecorded Sales Returns or Adjustments

Failing to include credit notes for returns or discounts makes the balance appear higher than it should.

How to avoid: Review recent credit notes and ensure all sales returns are reflected before issuing the statement.

6- Date Errors

Posting transactions under the wrong date period affects the running balance and confuses financial tracking.

How to avoid: Double-check transaction dates and ensure all entries fall within the correct statement period.

Read Also: Types of Errors in Accounting with Examples

How A Small Business Owner Uses A Statement Of Account?

For small business owners, a statement of account is more than just a record of transactions; it’s a vital financial management tool. It provides an at-a-glance summary of all dealings with a customer or supplier, helping the owner stay organized and make informed decisions.

Small business owners typically use the statement of account to track outstanding payments, ensuring they follow up with customers who have overdue balances. It also serves as proof of transactions during payment disputes, offering a clear record of issued invoices, received payments, and any pending amounts.

Additionally, it helps in reconciling accounts at the end of each period, confirming that what’s recorded in the books matches the actual financial activity. For growing businesses, regularly reviewing statements of account supports better cash flow management, helping owners plan expenses, monitor credit sales, and maintain healthy business relationships.

Statement Of Account Vs Invoice

A statement of account and an invoice are essential accounting documents, but they serve different purposes in the sales and payment process.

An invoice is a billing document issued by a seller to a buyer for a specific transaction. It lists the goods or services provided, the total amount due, payment terms, and any applicable taxes. Each invoice represents a single sale or service and acts as a request for payment.

A statement of account is a summary report that covers multiple invoices, payments, and credits over a defined period. It shows the running balance between a business and its customer, how much has been billed, paid, and what remains outstanding. Rather than requesting payment for a single sale, it helps both parties reconcile accounts and track ongoing transactions. If you need to issue individual transaction requests, start with our free invoice template before consolidating into a monthly statement.

Statement of Account vs. Invoice vs. Receipt

Three documents. Three stages. One transaction cycle.

| Statement of Account | Invoice | Receipt | |

| When issued | End of period (monthly) | Per transaction | After payment |

| Purpose | Summarize the relationship | Request payment | Confirm payment received |

| Shows | All transactions in a period | One sale or service | One completed payment |

| Outstanding balance | Yes | Yes (per invoice) | No |

| Sent by | Seller | Seller | Seller |

| Legal standing | Supporting evidence | Enforceable payment request | Proof of payment |

The statement of account sits between the invoice and the receipt in the payment cycle. Invoices are issued per transaction. Statements are issued periodically to consolidate. Receipts are issued once payment is confirmed. All three serve different functions — and a business managing credit sales needs all three to maintain a complete audit trail.

Statement Of Account Vs Balance Sheet

A statement of account and a balance sheet may both summarize financial information, but they serve entirely different purposes and audiences.

A statement of account is a customer-focused document that summarizes all transactions between a business and a specific client over a certain period. It includes invoices issued, payments received, credits, and the remaining balance. Its main goal is to help both parties reconcile their records and confirm outstanding amounts.

On the other hand, a balance sheet is a financial statement for the entire business, showing the company’s assets, liabilities, and equity at a specific point in time. It reflects the overall financial position of the business, not just its dealings with a single customer.

Account Statement Vs Transaction History

While both an account statement and a transaction history provide records of financial activity, they differ in purpose, scope, and presentation.

An account statement is a formal summary of all transactions between a business and a customer during a specific period. It highlights opening and closing balances, invoices, payments, credits, and any outstanding amounts, helping both parties reconcile accounts and confirm dues.

A transaction history, however, is a detailed, real-time record of every individual transaction made within an account. It often lacks summaries or balances and is mainly used for tracking recent activities or verifying specific entries.

Streamline Statement Of Account With Enerpize

Enerpize is an all-in-one cloud-based business and accounting management software designed to simplify financial tracking and reporting. When it comes to managing statements of account, Enerpize automates the entire process, from generating detailed statements to sharing them directly with clients.

Easily manage customer accounts through Enerpize, where all related transactions from invoices and payments to credit notes are displayed in one organized report. The system automatically updates balances, records transactions in real time, and generates professional statements ready to send in just a few clicks.

You can also download or customize a statement of account template to match your business needs, ensuring professional and consistent communication with clients. This saves time, effort and helps you maintain accuracy, transparency, and stronger financial control across your operations.

Key benefits include:

- Automated statement generation from recorded invoices and payments.

- Accurate, real-time balances for every customer.

- Ready-to-send statement templates that enhance professionalism.

- Easy export and sharing options for smooth customer communication.

FAQs

What is the purpose of an account statement?

The purpose of a statement of account is to provide a summarized record of all transactions between a business and its customer over a specific period. It helps verify balances, track payments, identify outstanding invoices, and ensure both parties agree on the current amount owed.

What information is included in a statement of account?

A standard statement of account typically includes:

- Business and customer details (name, address, contact information)

- Statement period and issue date

- Invoice numbers and dates

- Payment dates and references

- Credits, refunds, or adjustments

- Opening and closing balances

- Total amount due

How often should a business send a statement of account?

Most businesses send statements of account monthly, especially to customers with ongoing transactions or outstanding balances. However, some may issue them weekly or quarterly, depending on transaction volume and credit terms.

Can a statement of account be used to collect a debt?

A statement of account alone is not sufficient for formal debt collection, but it is an important piece of supporting documentation. It demonstrates that invoices were issued, the client was informed of the outstanding balance, and the business maintained accurate records. Combined with the original invoices and any written communication, a statement of account strengthens your position significantly in a dispute or legal proceeding.

What is the difference between a statement of account and a bank statement?

A bank statement is issued by a financial institution showing all transactions through your bank account. A statement of account is issued by a business to a client showing all transactions between the two parties — invoices, payments, and credits. Both serve as reconciliation tools but in completely different contexts: one tracks your money in the bank, the other tracks what clients owe you.

Is a statement of account a legal document?

A statement of account is not a formal legal instrument on its own, but it can serve as supporting evidence in a payment dispute or legal proceeding. A well-maintained statement — especially one sent to and acknowledged by the client — demonstrates that invoices were raised, the client was notified, and the business kept organized records. For formal debt recovery, consult a legal professional in your jurisdiction.

How long should you keep statements of account?

Most jurisdictions require businesses to retain financial records for 5–7 years. Statements of account fall under this requirement as they form part of your accounts receivable documentation. Store digital copies organized by client and period, with physical copies as backup if your jurisdiction requires original documents.

What information is included in the annual transaction report of a specific account?

An annual transaction report for a specific account — also called a yearly statement of account — includes all invoices issued, payments received, credits applied, and the opening and closing balance for the full year. It follows the same structure as a monthly statement of account but covers a 12-month period, giving both parties a complete record of the financial relationship for the year.

Join 40,000+ businesses that send professional statements of account automatically — without opening a spreadsheet. Create Your Free Account.

Creating statements of account is easy with Enerpize.

Try Enerpize accounting software to generate your statements of account automatically.

Creating statements of account is easy with Enerpize.

Try Enerpize accounting software to generate your statements of account automatically.