Author : Madonna Adel

What Is Accounts Receivable (AR)? And How To Improve?

Table of contents:

- Key Takeaways

- What Is Accounts Receivable (AR)?

- How Accounts Receivable Works

- Accounts Receivable Example

- Is Accounts Receivable an Asset?

- Accounts Receivable vs. Accounts Payable

- Where Accounts Receivable Appears on the Balance Sheet

- Net Receivables and Allowance for Doubtful Accounts

- How to Record Accounts Receivable

- How to Calculate Accounts Receivable

- Key Accounts Receivable Metrics and KPIs

- The Accounts Receivable Process

- How to Reconcile Accounts Receivable

- Common Accounts Receivable Challenges

- How to Manage Accounts Receivable Effectively

- What Is Accounts Receivable Financing?

- How Enerpize Streamlines Accounts Receivable Management?

- FAQs

Customers owe you. Managing invoices, monitoring incoming payments, and tracking outstanding balances are all part of handling accounts receivable. But accounts receivable is more than just tracking money; it plays a key role in cash flow, financial planning, and the overall health of your business.

In this article, you will learn what accounts receivable are, why they are considered assets, and how businesses can manage them effectively. We will also explore the accounts receivable process, common challenges, and practical tips for improving collection and maintaining a healthy cash flow.

Key Takeaways

- Accounts receivable (AR) represents money owed by customers for goods or services already delivered on credit, and it is recorded as a current asset on the balance sheet.

- AR directly impacts cash flow and working capital, making it a critical area for maintaining day-to-day operations and financial stability.

- The AR process follows a clear cycle, issuing invoices, tracking payments, applying cash receipts, and managing overdue or uncollectible balances.

- Journal entries drive AR accounting, from recognizing revenue at the time of sale to recording collections and writing off bad debts when necessary.

- Net receivables provide a more accurate view of expected cash, adjusting total receivables for the allowance for doubtful accounts.

- Key metrics like DSO, turnover ratio, and CEI help measure how efficiently a business collects payments and manages credit risk.

- Common challenges, such as late payments, invoice errors, and weak processes—can disrupt cash flow and require structured solutions to manage effectively.

- Strong AR management improves financial performance by reducing overdue invoices, accelerating collections, and minimizing bad debt.

- Practical improvements, like automation, clear policies, and better communication—lead to faster collections and fewer disputes.

- Accounts receivable financing provides short-term liquidity, allowing businesses to access cash tied up in unpaid invoices when needed.

- Using accounting software enhances visibility and control, helping businesses track receivables, reduce errors, and make better financial decisions.

What Is Accounts Receivable (AR)?

Accounts Receivable (AR) is the money a business is owed by its customers for goods or services that have been delivered but not yet paid for (credit sales). Essentially, it reflects the company’s earned revenue that is still pending collection, indicating that the business has fulfilled the transaction while the customer’s payment is pending.

These accounts are recorded as a current asset on the balance sheet and are a key driver of liquidity and working capital, since it represents cash the business expects to collect in the short term.

How Accounts Receivable Works

When a business makes a credit sale, it delivers goods or services without receiving cash upfront and records the amount owed as accounts receivable. An invoice is then issued to the customer, outlining the amount due and payment terms, often 30, 60, or 90 days.

During this period, the receivable remains on the balance sheet as a current asset while the company waits for payment. Once the customer pays, the receivable is cleared and converted into cash. If payment is delayed or unlikely, the company may adjust its records by recognizing an allowance for doubtful accounts to reflect the expected loss.

Here’s a simple table showing how the accounts move when a customer pays for goods purchased on credit:

| Transaction Stage | Account Debited | Account Credited | What It Means |

| Credit sale (invoice) | Accounts Receivable | Sales Revenue | The business records revenue and recognizes that the customer owes money |

| Payment received | Cash | Accounts Receivable | The customer pays, so cash increases, and the receivable is cleared |

Accounts Receivable Example

Imagine you run a business that supplies parts to a computer manufacturer. A customer orders components worth $5,000, and you deliver them as agreed. You then send an invoice giving the customer 30 days to pay.

Even though you haven’t received the cash yet, the sale is already counted as income. The $5,000 is recorded as a customer balance owed to your business and is listed under accounts receivable until payment is received.

Once the customer pays the invoice, the receivable is cleared. The accounts receivable balance decreases by $5,000, and your cash balance increases by the same amount.

Now consider a different situation: the customer pays long after the invoice was due, and the amount had previously been written off as uncollectible. In this case, the transaction must be reinstated. You do this by restoring the $5,000 to accounts receivable and recognizing the income again by crediting revenue for the same amount.

| Scenario | Account Debited | Account Credited | Amount | What It Means |

| Credit sale (invoice issued) | Accounts Receivable | Sales Revenue | $5,000 | Revenue is recognized, and the customer balance is recorded |

| Customer pays on time | Cash | Accounts Receivable | $5,000 | Cash is received, and the receivable is cleared |

| Write-off (if unpaid) | Bad Debt Expense | Accounts Receivable | $5,000 | The amount is removed as it’s considered uncollectible |

| Recovery (payment after write-off) | Accounts Receivable | Sales Revenue | $5,000 | The receivable is reinstated, and income is recognized again |

| Cash collected after recovery | Cash | Accounts Receivable | $5,000 | Cash is received, and the reinstated receivable is cleared |

Is Accounts Receivable an Asset?

Yes, accounts receivable is a current asset because it represents cash a business expects to collect from customers, usually within a year. It arises from credit sales, where the company has already delivered value and now holds a legal claim to payment.

AR is considered a current asset because of its short conversion cycle. Most receivables are tied to payment terms of 30, 60, or 90 days, meaning they are expected to be collected in the near term. This places AR alongside other working assets used to run day-to-day operations.

AR is also considered liquid, but not as liquid as cash. Its liquidity depends on how quickly customers pay and how reliable those payments are. High-quality receivables, those collected on time with minimal defaults, are closer to cash in practical terms. Slower collections or doubtful accounts reduce that liquidity.

From an analysis standpoint, AR plays a direct role in short-term financial health. It is a key component of working capital and is used in metrics like the current ratio and days sales outstanding (DSO). These measures help assess whether a business can meet its short-term obligations and how efficiently it converts sales into cash.

May help you: What Is Financial Accounting? A Plain Guide

Accounts Receivable vs. Accounts Payable

The comparison between accounts receivable and accounts payable highlights how a business manages incoming funds from customers versus outgoing obligations to suppliers, both of which are essential for maintaining cash flow and financial stability:

| Aspect | Accounts Receivable (AR) | Accounts Payable (AP) |

| Definition | Money customers and other debtors need to pay for the delivered products and services | Money that a business must pay to suppliers for goods and services already received |

| Business position | Represents amounts owed to the business | Represents amounts owed by the business |

| Balance sheet classification | Current asset because it represents future cash flow | Liability because it reflects outstanding payment responsibilities |

| Control in a relationship | Maintained by the supplier side of the transaction | Maintained by the buyer side of the transaction |

| Accounting treatment | Recognized as income unless written off; adjusted by allowance for doubtful accounts if not fully collectible | Recognized as a liability until paid, then cleared once payment is made |

| Financial importance | Helps forecast cash inflows, manage liquidity, and assess customer payment behavior | Helps manage cash outflows, supplier relationships, and short-term obligations |

| Example | The company records AR when it sends an invoice to a customer expecting payment (net 30–90 terms) | The company records AP when it receives an invoice from suppliers like Frames Inc. or lumber wholesalers |

Enerpize Accounting Software simplifies the management of both accounts receivable and accounts payable and is suitable for small and medium-sized businesses as well as large enterprises.

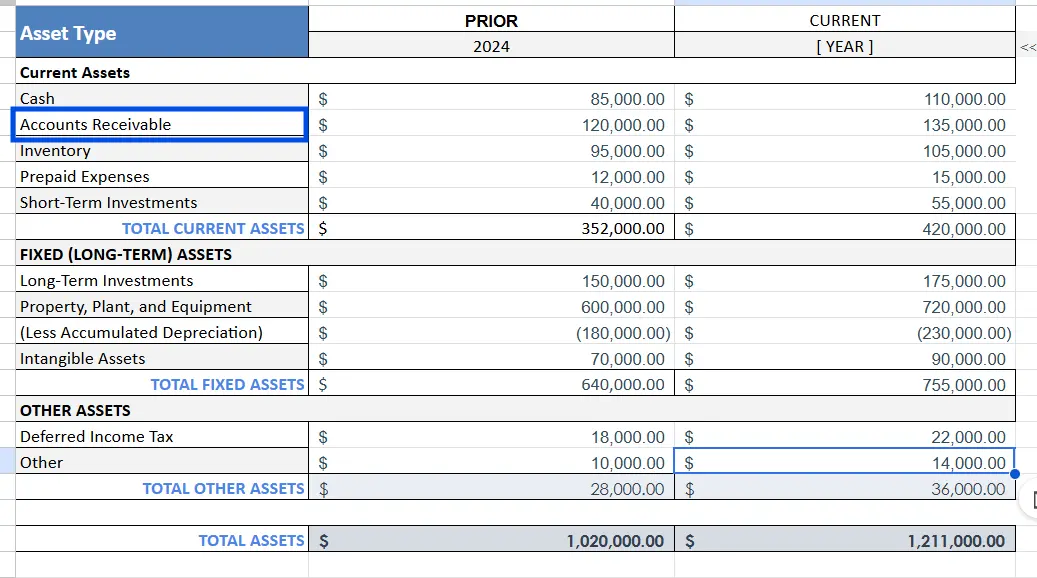

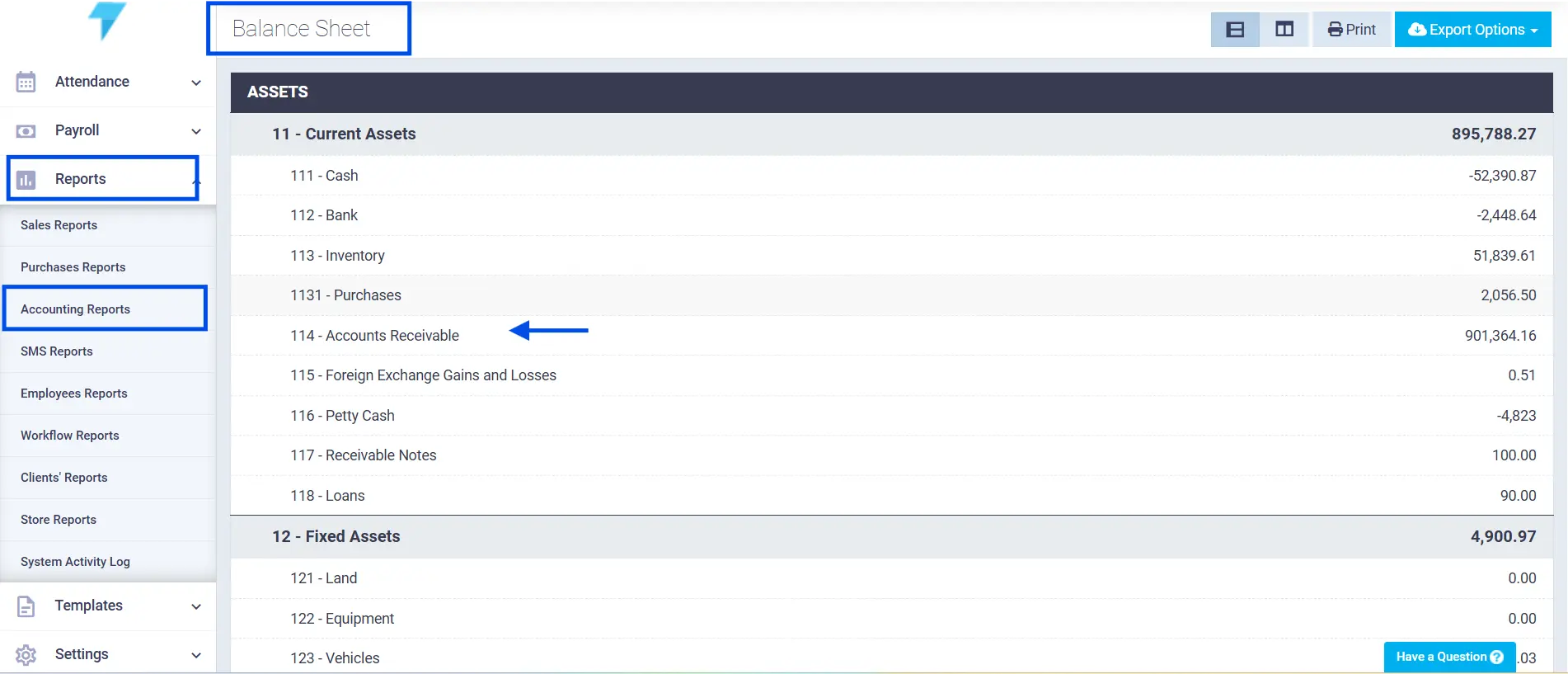

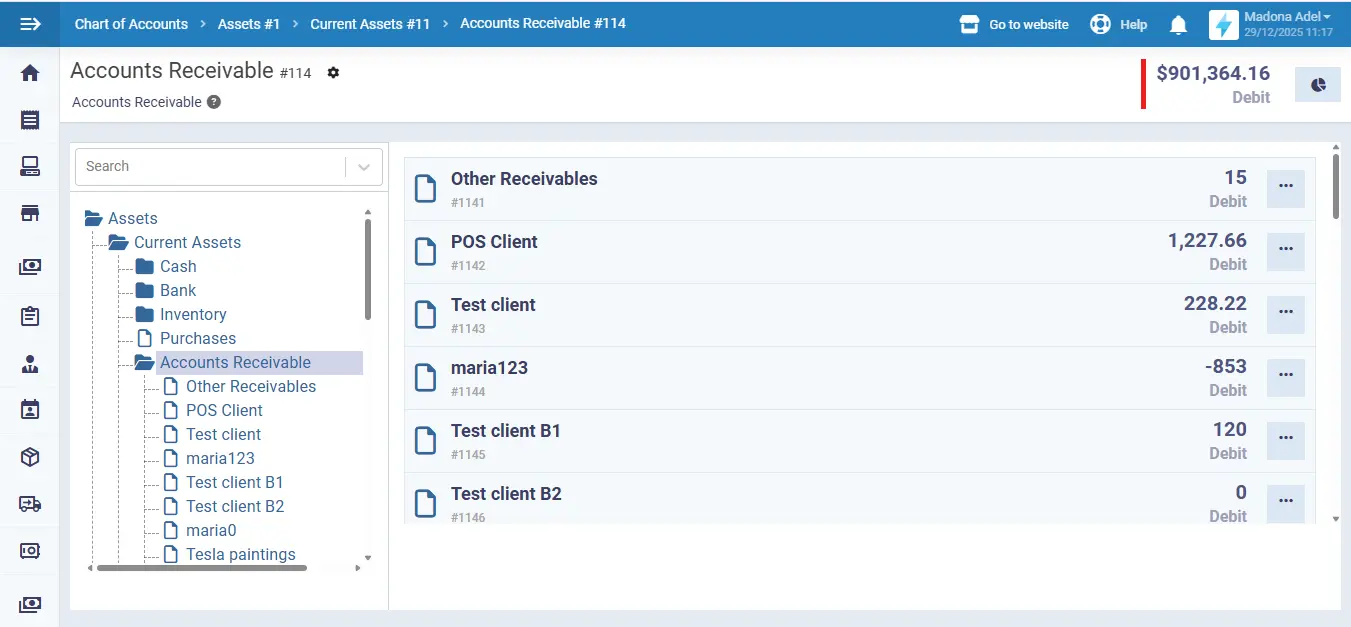

Where Accounts Receivable Appears on the Balance Sheet

Accounts receivable is recorded as a current asset on the balance sheet and represents amounts a company expects to receive from customers for goods or services already delivered. These balances usually arise from agreed credit terms, commonly ranging from 30 to 90 days, before payment is collected.

The following screenshot from the Enerpize system illustrates where AR appears on the balance sheet, showing its classification as a current asset and how it is presented within the system’s financial reporting structure.

Net Receivables and Allowance for Doubtful Accounts

Net receivables provide a more realistic view of expected cash collections by adjusting gross accounts receivable for amounts that may not be collected due to credit risk.

| Aspect | Accounts Receivable (Gross) | Allowance for Doubtful Accounts | Net Receivables |

| Definition | Total amount customers owe from credit sales | Estimated portion of receivables expected to be uncollectible | Amount expected to be actually collected |

| Balance sheet role | Current asset | Contra asset (reduces accounts receivable) | Net figure reported as collectible receivables |

| Purpose | Shows total credit granted to customers | Accounts for risk of non-payment or default | Reflects realistic cash inflow expectation |

| Basis of recognition | Recorded when sales are made on credit | Based on management estimates and past collection experience | Calculated as Gross AR minus Allowance |

| Financial impact | Can overstate expected cash if shown alone | Reduces reported asset value to reflect risk | Improves the accuracy of liquidity and cash forecasting |

| Adjustment behavior | Increases with credit sales | Adjusted when actual collection experience differs | Changes indirectly as AR or allowance changes |

Net receivables = Accounts Receivable − Allowance for Doubtful Accounts, giving a clearer picture of what the business is realistically expected to collect.

How to Record Accounts Receivable

Accounts receivable are recorded when a business provides goods or services on credit and issues an invoice, creating a claim for future payment. These balances are managed through customer accounts and adjusted as transactions occur, ensuring the receivables ledger reflects what is still owed at any point in time.

The process is driven by a small set of core journal entries that capture the movement from invoicing to collection and, when necessary, write-off.

Journal Entries for Accounts Receivable:

| Stage | Description | Journal Entry | Accounts Receivable Balance | Cash/Bank Balance |

| Invoice issued | Service is provided on credit, and an invoice is sent to the customer | Debit Accounts Receivable 5,000 Credit Revenue 5,000 | 5,000 | 0 |

| Partial payment received | The customer pays part of the invoice | Debit Cash (Bank) 3,000 Credit Accounts Receivable 3,000 | 2,000 | 3,000 |

| Bad debt write-off | The remaining amount is deemed uncollectible | Debit Bad Debt Expense 2,000 Credit Accounts Receivable 2,000 | 0 | 3,000 |

How to Calculate Accounts Receivable

The accounts receivable balance represents the total amount customers owe for goods and services already delivered. At its simplest, it is calculated by adding all outstanding customer invoices at a given point in time and subtracting any payments that have been received.

To estimate future receivables, businesses often rely on Days Sales Outstanding (DSO) because it links receivables directly to revenue. This approach helps predict how much of current sales will remain uncollected at a given time.

Formula:

Accounts Receivable = (DSO ÷ 365) × Revenue

This method reflects how long, on average, it takes to collect payments and allows companies to project receivable levels based on expected sales performance.

Using Enerpize simplifies accounts receivable management by automating invoice tracking, calculations, and key metrics like DSO, turnover ratio, and CCC. This helps businesses monitor cash flow easily, reduce errors, and improve collection efficiency.

Download our free accounts receivable template

Key Accounts Receivable Metrics and KPIs

Accounts receivable KPIs are used to track how efficiently a business extends credit, collects payments, and maintains steady cash flow. Looking at a single metric in isolation rarely tells the full story; strong AR performance comes from balancing collection speed, risk control, and customer experience.

Below are the most important metrics used to evaluate accounts receivable performance:

1- Accounts Receivable Turnover Ratio

Shows how often receivables are converted into cash over a period. A higher ratio means collections are happening more frequently and efficiently.

Formula:

Accounts Receivable Turnover = Net Credit Sales ÷ Average Accounts Receivable

Explore more on this topic: Accounts Receivable Turnover: A Comprehensive Guide

2- Days Sales Outstanding (DSO)

Measures the average number of days it takes to collect payment after a sale. Lower values indicate faster collections and stronger cash flow visibility.

Formula:

DSO = (Accounts Receivable ÷ Net Credit Sales) × Number of Days

3- Cash Conversion Cycle (CCC)

Measures the total time required to convert cash into inventory and back into cash through sales and collections. A shorter cycle indicates better operational efficiency.

Formula:

CCC = DSO + Days Inventory Outstanding (DIO) − Days Payable Outstanding (DPO)

Where:

- DIO = (Average Inventory ÷ Cost of Goods Sold) × Number of Days

- DPO = (Average Accounts Payable ÷ Cost of Goods Sold) × Number of Days

4- Average Collection Period

Another way to express how long it takes to collect receivables. It provides a quick view of whether payments are arriving within expected timelines.

Formula:

Average Collection Period = 365 ÷ AR Turnover Ratio

5- Collection Effectiveness Index (CEI)

Focuses on how much of the receivables a company actually collects, rather than how fast. It highlights the quality of the collection process.

Formula:

CEI = [(Beginning AR + Credit Sales − Ending AR) ÷ (Beginning AR + Credit Sales − Ending Current AR)] × 100

6- Average Days Delinquent (ADD)

Tracks how late payments are beyond agreed terms. It helps separate normal collection time from overdue delays.

Formula:

ADD = DSO − Best Possible DSO

7- Expected Cash Collections

Estimates how much cash the business is likely to receive, combining cash sales and projected collections from receivables. This is useful for short-term cash planning.

Formula:

Expected Cash Collections = Cash Sales + Projected AR Collections

8- Bad Debt and Allowance Measures

Bad debt reflects receivables that will not be collected, while the allowance method estimates these losses in advance. Monitoring this helps manage credit risk and avoid overstating assets.

Example formula:

Bad Debt to Sales Ratio = (Uncollectible Debts ÷ Total Sales) × 100

9- Percentage of High-Risk Accounts

Looks at the share of customers likely to default based on payment behavior. It helps balance growth with credit risk.

Formula:

(Number of High-Risk Accounts ÷ Total Accounts) × 100

10- Number of Revised Invoices

Tracks how often invoices are corrected due to errors or disputes. Frequent revisions can delay payments and signal process issues.

11- Staff Productivity (AR Team)

Measures how efficiently the receivables team converts effort into results, such as invoices processed or payments collected.

Formula:

Productivity = Output ÷ Input

12- Customer Satisfaction (Billing Experience)

Reflects how easy and transparent it is for customers to receive invoices and make payments. Poor experiences often lead to delays or nonpayment.

Why these KPIs matter

Together, these metrics give a complete picture of accounts receivable performance. Some focus on speed (DSO), others on quality (CEI), risk (bad debt, high-risk accounts), or operational efficiency (productivity, invoice accuracy).

Tracking them consistently helps businesses spot issues early, improve collections, and maintain healthy cash flow without damaging customer relationships.

The Accounts Receivable Process

The AR process covers all steps a business takes to manage customer payments, from delivery of a product or service through receipt of payment to account closure. It helps companies to track customer balances, follow up on unpaid balances, and maintain healthy cash flow and financial stability.

Accounts Receivable Process Steps:

- Providing goods or services on credit: The process begins when a business provides goods or services on credit and issues an invoice to the customer with agreed-upon payment terms.

- Issuing the invoice: The invoice is generated and sent to the customer, detailing the amount due and payment terms.

- Recording in the ledger: The invoice amount is recorded in the accounts receivable ledger under that customer’s account.

- Monitoring due dates and incoming payments: The company monitors due dates and incoming payments to ensure collections stay on track.

- Applying received payments: When a payment is received, it’s applied to the correct invoice, reducing the outstanding balance.

- Handling unmatched payments: If a payment can’t be matched immediately, it’s temporarily placed in a clearing account until it can be assigned appropriately.

- Follow-up on missed payments: If a customer misses a payment deadline, the company begins follow-up actions, such as reminders or collection efforts, to encourage payment.

- Assessing debtor risk: Companies assess debtor risk by reviewing customers’ payment history and creditworthiness to minimize the risk of bad debts.

- Analyzing and reporting information: Relevant information on receivables and payment behavior is analyzed and reported to management or controlling, enabling informed operational and strategic decisions.

Overall, the accounts receivable process goes beyond simple bookkeeping and plays a key role in effective cash flow management and financial planning.

How to Reconcile Accounts Receivable

Accounts receivable reconciliation is the process of verifying that the total amount recorded in the general ledger matches the sum of the balances of all customer accounts and related records. It helps ensure everything adds up and that the numbers accurately reflect what customers owe.

This process typically involves the following steps:

1- Review the accounts receivable ledger

Start by obtaining the accounts receivable balance from the general ledger for the reconciliation period.

2- Compare with the customer subledger

Add up all outstanding balances from individual customer accounts and verify that the total matches the general ledger balance.

3- Check outstanding invoices

Review all open invoices to ensure they are accurate, properly recorded, and reflect the correct amounts and due dates.

4- Verify incoming payments

Match customer payments received (such as bank deposits or receipts) to the corresponding invoices to confirm they have been correctly applied.

5- Investigate discrepancies

Identify and resolve differences caused by timing issues, posting errors, unapplied payments, credit notes, or write-offs.

6- Adjust and document corrections

Make the necessary journal entries to correct errors and document the reconciliation for audit and reporting purposes.

Regular reconciliation of accounts receivable helps ensure accurate financial records, improves cash flow management, and reduces the risk of errors or fraud.

Common Accounts Receivable Challenges

Managing accounts receivable is central to keeping cash flowing, but it rarely runs without friction. Most issues come down to delays in payment, gaps in process, or weak coordination between teams and customers.

These problems can slow collections, increase costs, and limit growth:

1- Invoice errors and disputes

Mistakes in pricing, quantities, or terms often lead to disputes. Even small discrepancies can delay payment while the issue is investigated. Clear, accurate invoices and consistent documentation reduce back-and-forth and help resolve issues faster when they do arise.

2- Late payments and overdue balances

Delayed payments disrupt cash flow and make it harder to plan expenses or invest in the business. Weak payment terms, lack of follow-up, or poor visibility into receivables often contribute to the problem.

3- Credit risk and high-risk customers

Extending credit always carries risk. Without proper assessment, businesses may end up dealing with customers who consistently pay late—or not at all. Monitoring payment history and aging reports helps identify warning signs early.

4- Manual errors and inefficient processes

Heavy reliance on manual data entry, invoice handling, and payment matching increases the risk of mistakes and slows down the entire cycle. These inefficiencies can lead to incorrect records, missed payments, and delays in updating accounts.

5- Disorganized data and limited visibility

When receivables data is scattered or outdated, it becomes difficult to track balances, monitor trends, or make informed decisions. Poor reporting limits a company’s ability to act quickly on overdue accounts or forecast cash flow accurately.

6- Ineffective collection strategies

A one-size-fits-all approach to collections rarely works. Some customers respond to reminders, while others require more structured follow-ups. Without a clear and adaptable strategy, collections become inconsistent and less effective.

7- Weak customer communication

Unclear invoices, missing details, or a lack of follow-up can confuse customers and delay payment. Strong communication—before and after invoicing—helps set expectations and reduces misunderstandings.

8- Unclear payment terms

If due dates, penalties, or payment methods aren’t clearly defined, delays are more likely. Consistent and transparent terms from the start of the relationship help avoid confusion later.

9- Cash flow interruptions

When collections slow down, the impact spreads quickly—affecting payroll, supplier payments, and growth plans. Regular monitoring of receivables and faster invoicing can help reduce these gaps.

10- Inaccurate forecasting

Poor estimates of incoming cash can lead to shortages or missed opportunities. Forecasts that aren’t updated or based on reliable data make it harder to manage working capital effectively.

11- Limited scalability and system constraints

As businesses grow, outdated systems and manual workflows struggle to keep up. This leads to bottlenecks, higher error rates, and reduced efficiency across the receivables process.

These challenges are closely connected. Invoice errors can lead to disputes, disputes delay payments, and delays disrupt cash flow. Strengthening processes, improving data visibility, and maintaining clear communication go a long way in keeping accounts receivable under control.

How to Manage Accounts Receivable Effectively

Efficient accounts receivable management is essential for maintaining healthy cash flow and reducing payment delays. The practices below are not just operational improvements—they directly influence key outcomes such as faster collections, fewer disputes, and stronger financial stability:

1- Move to digital invoicing and online payments

Shifting to electronic billing and payment platforms speeds up the invoicing cycle and reduces manual errors. The result is shorter payment cycles and lower Days Sales Outstanding (DSO), as customers can receive and settle invoices instantly.

2- Track key performance indicators (KPIs)

Monitoring metrics like DSO, Average Days Delinquent (ADD), and accounts receivable turnover helps identify bottlenecks early. This leads to better decision-making and continuous improvement in collection efficiency, ultimately strengthening cash flow predictability.

3- Standardize billing procedures

Establishing consistent invoicing formats, approval workflows, and follow-up steps minimizes errors and confusion. This reduces invoice disputes and rework, helping payments move through the system faster.

4- Set clear credit and collection policies

Defining payment terms, credit limits, and escalation procedures upfront ensures customers know what to expect. Strong policies contribute to fewer overdue invoices and reduced credit risk.

5- Be proactive with collections

Following up early on outstanding balances—supported by automated reminders—keeps payments top of mind for customers. This approach leads to faster collections and improved aging profiles.

6- Automate routine tasks

Using accounts receivable software to handle invoicing, reminders, and reconciliation reduces manual workload and errors. Automation improves team productivity and consistency, allowing staff to focus on higher-value activities like dispute resolution.

7- Simplify the payment experience

Clear invoices and multiple payment options (such as online portals) remove friction for customers. This directly results in quicker payments and fewer delays caused by payment difficulties.

8- Involve multiple teams

Collaboration between finance, sales, and customer-facing teams ensures alignment on customer terms and faster issue resolution. This reduces billing errors and disputes, leading to smoother collections and stronger customer relationships.

What Is Accounts Receivable Financing?

Accounts receivable (AR) financing lets a business access cash tied up in unpaid invoices instead of waiting for customers to pay. It can be used either as collateral for a loan or by selling the receivables to a financing provider.

This approach is most useful for companies that sell on credit and face delays in collecting payments. It helps cover short-term needs like payroll, supplier costs, or day-to-day operations when cash inflows are slow.

The amount of funding depends on how reliable the receivables are—lenders look at factors like how old the invoices are and whether customers are likely to pay. Businesses with larger and more dependable receivables can usually access more funding.

In practical terms, AR financing is used when cash is needed before customer payments are received.

How Enerpize Streamlines Accounts Receivable Management?

Enerpize online accounting software helps businesses manage accounts receivable efficiently and simply. By using the system, companies can issue electronic invoices and keep all customer billing information organized in one place.

This accounts receivable automation makes it easier to track outstanding amounts and know precisely what customers owe and when payments are due.

The software also supports recording and matching incoming payments with the correct invoices. Once a payment is received, it can be registered in the system and automatically reflected in the customer’s balance. This reduces manual work, minimizes errors, and ensures accounts receivable records remain accurate and up to date.

Enerpize allows businesses to manage customer accounts centrally. For each customer, you can view invoice history, outstanding balances, and payment status at any time. This gives a clear overview of receivables and helps finance teams follow up on overdue payments more effectively.

In addition, the system provides detailed financial reports related to sales, collections, and customer balances. These reports help businesses analyze their accounts receivable performance, monitor cash flow, and make better financial decisions. Overall, Enerpize supports better control, visibility, and efficiency in managing accounts receivable.

FAQs

Is accounts receivable a debit or credit?

Accounts receivable is recorded as a debit. When a company issues an invoice for goods or services provided on credit, accounts receivable is debited to reflect the amount owed by the customer. When the customer pays, accounts receivable is credited, reducing the balance.

Is accounts receivable a current asset?

Yes, accounts receivable is classified as a current asset.

It represents amounts that a company expects to collect from customers within a short period, typically within one year, making it part of the company’s short-term assets.

What type of account is accounts receivable?

Accounts receivable is an asset account, specifically a current asset account on the balance sheet.

It reflects the company’s legal claim to receive cash from customers for goods or services already delivered.

What does accounts receivable do?

Accounts receivable refers to the amounts customers still owe for goods or services already provided. It allows businesses to track unpaid invoices, manage incoming payments, plan cash flow, and assess customer reliability. Properly managing accounts receivable helps ensure timely payments and supports overall financial health.

In summary, accounts receivable are a crucial part of any business’s financial management. By effectively tracking customer payments, managing outstanding invoices, and assessing credit risk, companies can maintain healthy cash flow and ensure financial stability.

Using the right processes and tools, like digital invoicing and accounting software, makes managing receivables simpler, more accurate, and more efficient, supporting the overall growth and success of the business.

Managing accounts receivable is easy with Enerpize.

Try Enerpize accountig software to manage accounts receivable automatically.

Managing accounts receivable is easy with Enerpize.

Try Enerpize accountig software to manage accounts receivable automatically.