Posted on 26 May 2026

Free Australian Invoice Template Download (No GST): Word, Excel, PDF & Google Sheets

- ATO-compliant for businesses not registered for GST — includes the ABN field, correct invoice title, and the legally required 'not a tax invoice' declaration.

- Covers sole traders, freelancers, subcontractors, and new businesses — the four groups who need a non-GST invoice most often and get the least specific guidance online.

- Pre-built payment terms — 14-day due date, 2% monthly late fee clause, and minimum order value field explained in plain language.

- Available in Word, Excel, PDF, Google Sheets, and Google Docs — download the format you already use, today, for free.

An Australian invoice template (no GST) is a ready-to-use billing document for businesses not registered for GST in Australia that displays the seller's ABN with a non-registration qualifier, the correct 'Invoice' title, and all fields the ATO requires so clients receive a compliant, dispute-proof record without any GST component.

What Is an Australian Non-GST Invoice?

An Australian non-GST invoice is a standard invoice issued by a business that is not registered for Goods and Services Tax. It documents a sale, requests payment, and satisfies the ATO's record-keeping requirements — but it does not charge, collect, or remit any GST, because the issuing business is not legally authorised to do so.

The distinction matters more than most template pages acknowledge. The words you put at the top of your invoice are not stylistic. If your business is GST-registered, your invoice must say 'Tax Invoice.' If it is not, your invoice must say 'Invoice' and nothing else. Placing the words 'Tax Invoice' on a document when you are not registered for GST is a breach of the A New Tax System (Goods and Services Tax) Act 1999, and it creates a false document that a client's accountant may attempt to use to claim an input tax credit that is not valid.

The ATO's guidance on setting up business invoices is explicit: if you are not registered for GST, your invoices should not include the words 'tax invoice.' That is the legal baseline. This template is built around it.

How It Differs from a Tax Invoice

| Feature | Non-GST Invoice (This Template) | Tax Invoice (GST Article) |

|---|---|---|

| Document title | Invoice | Tax Invoice |

| GST displayed | None — $0.00 or omitted | 10% per taxable line item |

| ABN required | Yes — mandatory for all invoices | Yes — mandatory for all tax invoices |

| Declaration needed | Yes — 'not a tax invoice' statement | No — title 'Tax Invoice' is sufficient |

| Who issues it | Businesses with GST turnover below $75K or voluntarily unregistered | GST-registered businesses only |

| BAS implications | None — no GST collected, no BAS lodgement for GST | GST collected feeds into quarterly BAS |

Related: If your business is GST-registered and you need a template that calculates the 10% GST rate, handles mixed taxable and GST-free line items, and feeds into your BAS, see our Australian GST invoice template guide — a separate resource built specifically for that use case.

Generate a compliant Australian non-GST invoice in seconds. ABN field, payment terms, and declaration pre-built. Start for free, no credit card required.

Who Should Use This Template?

The requirement to issue a non-GST invoice rather than a tax invoice is tied entirely to GST registration status, not business size or legal structure. If you are not registered for GST, you use this template. Four groups need it most, and each has a specific wrinkle the generic template pages never address.

Sole Traders and Freelancers Under $75,000

A sole trader operating a lawn care business in Queensland, a freelance copywriter billing clients in Melbourne, or a consultant doing 15 hours a week of advisory work — if their combined annual GST turnover sits below $75,000, GST registration is voluntary. Most choose not to register, either because the administrative overhead is not worth it or because they are still building toward the threshold.

For this group, the invoice template is clean and simple. Business name. ABN. Date. Invoice number. Description of services. Total. Payment terms. The one field that confuses sole traders most often is the ABN qualifier: the template includes '(Not registered for GST)' as a bracketed note next to the ABN field. That bracket is not decorative. It signals to the client's accountant that no input tax credit exists on this invoice, which saves a phone call during BAS time.

For the complete picture on how GST registration works and when it becomes mandatory, the ATO's GST registration page is the authoritative source.

Subcontractors and Tradies

Subcontractors often work within a principal contractor's supply chain and invoice upward for labour or materials. A subcontractor who has not yet crossed the GST threshold will send non-GST invoices to the head contractor. The head contractor's accounts team needs the invoice to clearly state that no GST has been charged, so they do not accidentally claim a GST credit they are not entitled to.

For tradies specifically, the delivery address field on this template becomes more relevant. A plumber subcontracting at a job site invoices for work performed at an address that is different from both their own business address and the head contractor's registered office. The template includes a dedicated delivery address field precisely for this scenario.

The 'minimum order value applies' clause pre-built into the payment terms section is also more commonly relevant for tradies and subcontractors than for freelancers — if you have set a minimum callout fee or minimum job value, this is where it is documented on the invoice.

New Businesses in Their First Year

A new business does not know in advance whether its first-year turnover will reach $75,000. The ATO's rule for new businesses is that you must register for GST if you expect to reach the threshold in your first year of operation. If you genuinely do not expect to, you start issuing non-GST invoices from day one.

The risk period is the growth phase — when monthly revenue is accelerating and the $75,000 annual figure starts to look achievable. The rolling 12-month calculation (covered in full below) is where new businesses get caught, because the threshold is not a calendar-year total. It is the previous 12 months at any point in time. A business that hits $74,000 in its first eleven months and then invoices $2,000 in month twelve has crossed the threshold and must register within 21 days.

Until that registration is effective, the non-GST invoice template is the correct document. On the day registration is confirmed, you switch to a tax invoice format and update all future invoices accordingly.

What Must a Non-GST Invoice Include? (ATO Requirements)

Unlike tax invoices, which have seven mandatory fields set out in GSTR 2013/1, non-GST invoices do not have a statutory field list. The Australian government's invoicing guidance states that 'there is no law that sets out what to put in a regular invoice,' but immediately follows with a list of what common practice — and ATO compliance expectations — require. For any practical purpose, the following fields are mandatory.

| Field | What It Must Show | Risk If Missing |

|---|---|---|

| Invoice title | The word 'Invoice' — never 'Tax Invoice' | Legal breach; creates a false document if not GST-registered |

| Business name | Your legal name or trading name | Client cannot identify the payee |

| ABN | Full 11-digit number with '(Not registered for GST)' qualifier | 47% withholding obligation triggered for the payer — see below |

| Date of issue | Date invoice was issued, not the date work was completed | Record-keeping gap; ATO requires 5-year retention |

| Invoice number | Unique sequential reference | No tracking, no reconciliation, no audit trail |

| Description of goods/services | Brief description with quantity and unit price | Disputes arise; client can legitimately delay payment |

| Total amount payable | Net total with currency | Payment cannot be processed without this |

| Payment terms | Due date and accepted payment methods | Late payment is harder to enforce without documented terms |

| 'Not a tax invoice' declaration | Explicit statement that this document is not a tax invoice | Protects you legally; signals to client's accountant |

The ABN Field: What If You Do Not Have One Yet?

Every Australian business should have an ABN. Applying is free and takes minutes through the Australian Business Register. However, new businesses often send their first invoices before the ABN application has been processed, which typically takes 24 to 48 hours but can take up to 28 days for some business structures.

If you issue an invoice without an ABN, the recipient of that invoice is legally required by the ATO to withhold 47% of the gross amount before paying you. This is the Pay As You Go (PAYG) withholding rule for no-ABN situations. The withheld amount is paid to the ATO, not to you. You can claim it back at tax time, but the cash flow impact in the short term is severe.

The correct approach when waiting for an ABN is to contact the client, explain that your ABN application is in progress, and ask them to hold payment until you can provide the number. Issue the invoice when your ABN is confirmed. Most clients will accommodate a 48-hour delay without issue.

Trading Name vs. Business Name: Which Goes on the Invoice?

Sole traders and small businesses often operate under a trading name that is different from their legal name. A person named Michael Chen who operates a business called 'Blue Ridge Carpentry' has two names in play. The invoice should show both: the trading name for the client's recognition and record-keeping, and the legal name with ABN for ATO compliance.

The format that works cleanly is: 'Blue Ridge Carpentry, trading as Michael Chen' followed by the ABN. If the business is registered as a sole trader under the personal name, the ABN is attached to Michael Chen, not to Blue Ridge Carpentry, so the legal name must appear.

If the trading name is registered as a business name with ASIC, it can appear as the primary name on the invoice, but the ABN must still accompany it, because the ABN is linked to the legal entity — not the trading name.

The 'This Is Not a Tax Invoice' Declaration: Why It Is Not Optional

The declaration printed at the bottom of this template — 'This is not a tax invoice as seller is not registered for GST' — looks like boilerplate. It is not. It exists because the consequences of ambiguity flow in one direction only, and they flow to the seller.

If a GST-registered client receives your invoice and their accounts team mistakenly treats it as a tax invoice, they may attempt to claim an input tax credit on their next BAS. The ATO will reject that claim and may audit the client's credit history. The client will then trace the error back to your invoice and ask you to reissue. That sequence costs time, damages the relationship, and creates a documentation trail that the ATO can follow.

The declaration eliminates the ambiguity before it starts. It is a one-sentence statement that costs you nothing to include and protects you from a compliance chain reaction that costs you quite a lot to untangle. Every invoice this template generates includes it.

The $75,000 Threshold: When Do You Actually Cross It?

Every competitor page states the $75,000 threshold. Zero of them explain how it is calculated in practice. This matters because the ATO does not measure your GST turnover against a fixed financial year. It measures it on a rolling 12-month basis. That changes everything for a growing business.

The $75,000 figure refers to your GST turnover — which is your gross income from all business activities minus any GST already included in those amounts. Non-commercial activities, salary income, and private sales are excluded. What remains is measured continuously: at any point in time, the ATO looks at the previous 12 calendar months and the current month projected forward.

The Rolling Calculation: A Real Scenario

Scenario: Emma runs a sole trader web design business. In the 12 months from July 2025 to June 2026, her total revenue from client work is $71,000. She is comfortably below the threshold. In July 2026, she lands two major projects and invoices $6,500 for that month alone. Her rolling 12-month turnover — August 2025 through July 2026 — is now $76,500. She has crossed the threshold.

Emma must register for GST within 21 days of the month in which she crossed the threshold. From the date her registration is effective, all future invoices must be tax invoices that include GST. Her invoices issued before the registration date remain valid non-GST invoices — she does not need to reissue them.

The practical implication: if you are approaching $75,000 in rolling 12-month turnover, start monitoring monthly. The threshold is not a once-a-year calculation. It is a continuous obligation.

You Just Crossed $75K: What Happens to Your Existing Invoices?

Nothing happens retroactively. Invoices you issued before your GST registration was effective are non-GST invoices and they remain so. Your clients do not need to reissue payments. You do not need to send amended documents.

What changes is: every invoice you issue from the effective date of your GST registration must be a tax invoice. If you have an invoice already in draft that crosses the registration date, hold it, switch to the GST invoice template, add the 10% GST calculation, and update the document title to 'Tax Invoice' before sending.

The transition is clean if you manage the date carefully. The transition is messy if you send a non-GST invoice after your registration is already effective, because that document is now incorrect and the client cannot claim an input tax credit from it. Enerpize tracks your registration status and automatically prompts you to switch invoice types when the status changes, so the transition happens at the correct point rather than two invoices too late.

The 47% Withholding Rule: Why Your ABN Matters Even Without GST

This is the compliance risk that no invoice template page talks about, and it is the highest-stakes practical concern for Australian businesses issuing non-GST invoices. The rule is simple, the exposure is serious, and it is entirely preventable.

Under the ATO's PAYG withholding rules, if a business receives an invoice that does not include a valid ABN, it is legally required to withhold 47% of the gross invoice amount before making payment. The withheld amount is remitted to the ATO. The ATO's withholding if no ABN is quoted page confirms this obligation applies to payments for goods and services made in the course of business.

Example: You send an invoice for $3,000 for consulting services. You forgot to include your ABN. Your client's bookkeeper notices, flags it as a no-ABN invoice, and is legally required to withhold $1,410 (47%) before paying you. You receive $1,590. You can claim the $1,410 back at tax time, but you are waiting months for money that should have arrived this week.

The rule applies to invoices from both unregistered and GST-registered businesses. It is not a penalty for not being registered for GST. It is a withholding mechanism that exists to ensure income is reported. The ABN on your invoice is the proof that income will be reported by an identifiable entity.

Two scenarios trigger it in practice. First, you accidentally leave the ABN field blank when copying a template. Second, you send an invoice before your ABN application has been processed. The template's ABN field is mandatory and clearly labelled — filling it in takes three seconds and protects $1,410 or more on every invoice.

Enerpize validates your ABN on every invoice before the document is issued and monitors your rolling turnover so you know exactly when you are approaching the $75K threshold. Start for free, no credit card required.

Understanding the Clauses Pre-Built Into This Template

The template includes three pre-built clauses in the payment terms section that most users either edit without understanding or leave in without knowing what they have committed to. Each clause has a legal dimension that is worth understanding before you send your first invoice.

Payment Due Within 14 Days and the 2% Monthly Late Fee

The template states: 'Payment due within 14 days. Late payments incur a 2% monthly fee.' This is a contractual term, not a regulatory one. The ATO does not mandate payment terms on non-GST invoices — you set them yourself, and the terms on this template are defaults that you can change.

The 2% monthly late payment fee is legally enforceable in Australia under contract law, subject to one important condition: the client must have been aware of the term before or at the time of contracting, not just when they received the invoice. If you agreed a scope of work verbally and then sent an invoice with a 2% late fee clause the client had never seen, enforcing that clause in a dispute is difficult.

The practical solution is to include your payment terms in your written proposal, quote, or client agreement before work begins, and then restate them on the invoice. When the same term appears in both documents, enforceability is straightforward. If you operate on a handshake agreement with no pre-engagement paperwork, consider whether 2% monthly is the right default — 1.5% is more commonly accepted in practice and less likely to generate friction.

You can change the payment period from 14 days to 7, 21, or 30 days — whichever your client relationship and cash flow requirements dictate. Shorter terms are better for cash flow. Longer terms are sometimes required by larger clients who operate on net-30 or net-45 internal processing cycles.

Minimum Order Value: What It Means and Whether It Is Enforceable

The clause reads: 'For non-GST registered businesses only. Minimum order value applies.' The minimum order value field exists for businesses that have a minimum engagement threshold — a tradie who does not take jobs under $200, for example, or a consultant who does not bill for less than two hours.

A minimum order value clause is enforceable in Australia if it was communicated to the client before they placed the order. If it appears only on the invoice and the client had no prior notice, you cannot refuse payment on a below-minimum invoice or charge a fee for it. The clause works as a forward-looking business policy, not as a retrospective charge.

If you do not have a minimum order value, delete this clause from the template. Leaving it in without filling in the figure creates ambiguity about what your minimum is, which creates a question you do not want a client asking after they have already received a service.

Delivery Address: When Is It Relevant?

The template includes a separate delivery address field below the billing address. For service businesses billing a single client address, this field will usually be left blank. It becomes relevant in three situations: when the service is delivered at a physical location that differs from the client's registered office (a subcontractor invoicing a head contractor for work at a job site), when goods are shipped to an address the buyer nominates, and when the client's accounts payable team is in one location and the service delivery is in another.

For record-keeping purposes, the delivery address on an invoice is useful if there is ever a dispute about whether the service was delivered at the agreed location. Leave it blank when it adds no information. Fill it in when the delivery location is part of the transaction's substance.

How to Fill In This Template: Step-by-Step

The following steps apply to all five formats: Word, Excel, PDF, Google Docs, and Google Sheets. The fields are identical across formats. The only difference is how you edit them.

- Enter your business details. Business name or trading name at the top. ABN in full — 11 digits, formatted as XX XXX XXX XXX — followed by the '(Not registered for GST)' qualifier. Business address, phone, and email. If you operate under a trading name that differs from your legal name, include both as described in the trading name section above.

- Enter client details. Client name and business name. Billing address. If the delivery address differs, add it in the separate field. The client's phone and email are optional but useful for follow-up if the invoice goes unpaid.

- Assign an invoice number. Use a sequential numbering system. Start at 001 or 1001 — whatever suits your business. Never reuse an invoice number. The ATO expects invoice numbers to be unique and sequential for record-keeping purposes.

- Set the date and due date. Date of issue is today's date or the date you are sending the invoice, not the date work was completed. Due date is your payment terms date — 14 days from issue date if you are using the default clause. Change the 'Terms' field to match: 'Net 14,' 'Due on Receipt,' or whatever applies.

- Describe your services. One line per service or product. Description should be specific enough that neither party could dispute what it refers to. Quantity and unit price per line. The Amount column calculates automatically in Excel and Google Sheets — in Word and PDF, enter the line total manually.

- Confirm the total and review the declaration. The total is the sum of all line items. No GST is added. The declaration at the bottom — 'This is not a tax invoice as seller is not registered for GST' — should remain on every invoice. Do not delete it.

- Add payment details. BSB and account number in the payment notes field, or your PayID, PayPal, or other accepted method. Specify the reference the client should use — typically the invoice number — so you can match incoming payments to outstanding invoices.

- Save, send, and archive. Save a copy for your records. The ATO requires you to retain invoice records for five years. Email the invoice as a PDF so the client receives a document they cannot accidentally edit. Archive the source file so you can reissue or amend if needed.

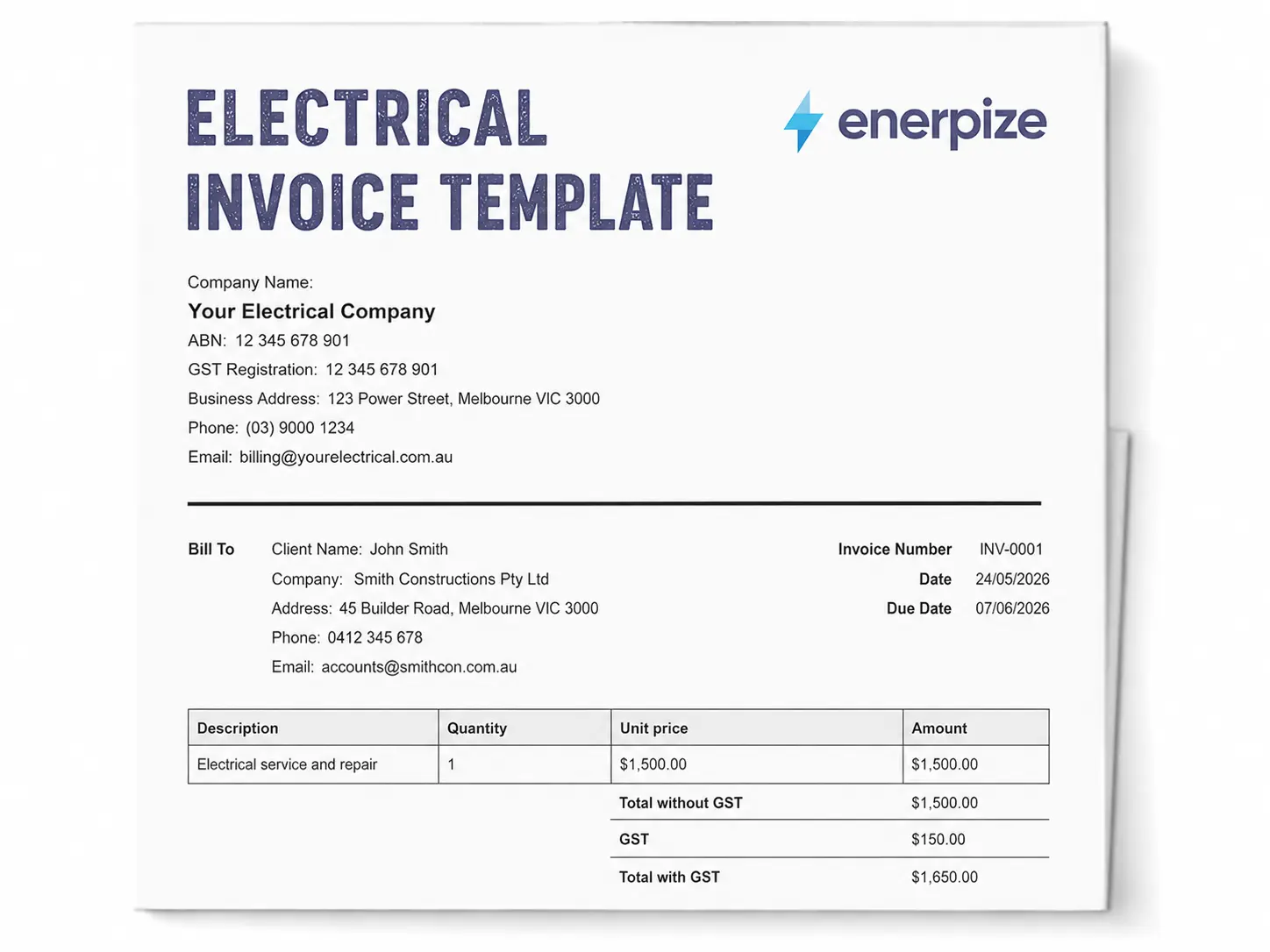

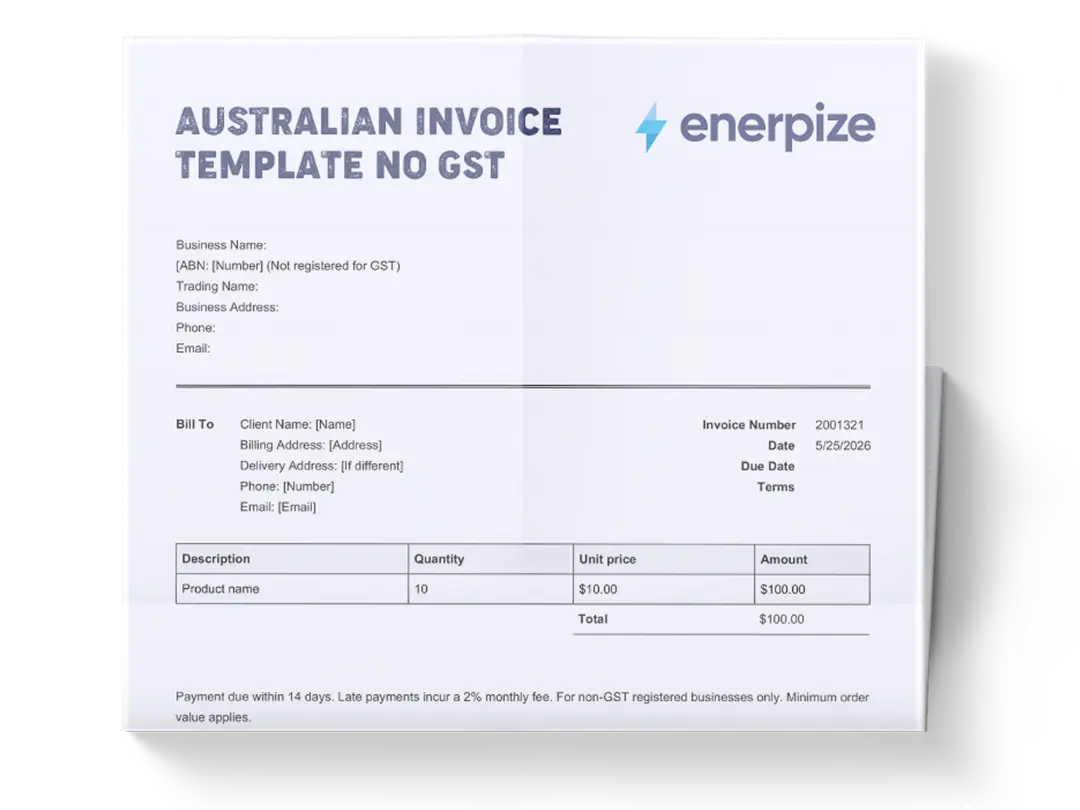

Worked Example: A Sole Trader Non-GST Invoice

Below is a fully populated example of a valid Australian non-GST invoice. The business is a sole trader lawn care operator in New South Wales. All fields reflect real ATO requirements, not placeholders.

INVOICE

Green Edge Lawn Care (trading as Daniel Okafor) ABN: 51 234 567 890 (Not registered for GST) 14 Banksia Street, Penrith NSW 2750 Phone: 0421 555 789 | Email: daniel@greenedgelawn.com.au

| Bill To: | Invoice No: | INV-0042 | |

|---|---|---|---|

| Sunrise Property Group | Date: | 26 May 2026 | |

| ABN: 77 456 123 890 | Due Date: | 9 June 2026 | |

| 8/22 Pioneer Road, Blacktown NSW 2148 | Terms: | Net 14 |

| Description | Qty | Unit Price | Amount |

|---|---|---|---|

| Lawn mowing and edge trim — 4 residential properties | 4 | $85.00 | $340.00 |

| Hedge trimming — 2 properties | 2 | $65.00 | $130.00 |

| Rubbish removal and green waste disposal | 1 | $45.00 | $45.00 |

| TOTAL | $515.00 |

Payment due within 14 days. Late payments incur a 2% monthly fee. Please transfer to: BSB 062-123 | Account 1098 7654 | Ref: INV-0042

DECLARATION: This is not a tax invoice as seller is not registered for GST.

This example meets all ATO requirements for a non-GST invoice: correct title (Invoice, not Tax Invoice), ABN with the (Not registered for GST) qualifier, unique invoice number, date and due date, itemized line items, total without GST, payment details, and the legally protective declaration.

Does Your State Affect Your Non-GST Invoice?

Short answer: no. GST is a federal tax administered by the Australian Taxation Office, and the rules for non-GST invoices apply uniformly across all states and territories. An invoice template for a sole trader in New South Wales is structurally identical to one for a sole trader in Western Australia or Queensland.

Where state and territory rules can intersect with invoicing is in industry-specific licensing requirements. A licensed builder in Victoria must display their Builder Practitioner number on invoices for domestic building work. An electrical contractor in Queensland may be required to display their electrical contractor licence number. These are regulatory additions, not changes to the GST or ATO invoicing framework, and they apply on top of the standard fields, not instead of them. For small businesses operating across multiple states or managing more complex workflows, our guide to the best ERP software for small business in Australia covers how a full business management system handles multi-location compliance and operations.

If you operate in a licensed trade, check your state's licensing authority requirements for what must appear on invoices in your specific industry. The template includes a 'Business Name' header and an extended notes field where licence numbers can be added without disrupting the core invoice structure.

How Enerpize Handles Non-GST Invoicing for Australian Businesses

A downloaded template handles your first twenty invoices. It starts to show its limits around invoice fifty, when you are tracking who has paid, chasing two overdue invoices simultaneously, trying to remember what format your last invoice was saved in, and wondering whether you are approaching the $75K threshold.

Enerpize's invoicing module is built for Australian businesses at exactly this stage — past the point where a template is enough, but not yet at the complexity level that requires an enterprise accounting system. For Australian small businesses evaluating whether a full ERP system is the right next step, see our guide to the best ERP software for small business in Australia.

ABN Validation on Every Invoice

Enerpize stores your ABN and validates that it appears on every invoice before the document is finalised. For non-GST businesses, the ABN field includes the '(Not registered for GST)' qualifier and the invoice title is set to 'Invoice' — not 'Tax Invoice.' You control these fields and update them if your registration status changes.

GST Status Switching

When your GST registration becomes effective, you update your registration status in Enerpize and switch your invoice template to reflect the change. Every new invoice from that date forward becomes a tax invoice with the 10% GST calculation applied per line item. Invoices issued before the switch remain non-GST invoices in your records. The transition creates no version control problem and no retroactive changes. For the full picture on how GST invoice generation works inside Enerpize, see the Australian GST invoice template guide.

Rolling Turnover Monitoring

Enerpize gives you a clear view of your invoiced revenue so you can monitor where you stand relative to the $75,000 threshold. For businesses in the $60K to $74K range, having your invoices and income in the same system removes the need to maintain a separate spreadsheet for turnover tracking. Paired with Enerpize's accounting software for Australia, the invoicing and financial data sit in the same environment, giving you an up-to-date picture at any point in time.

Payment Tracking and Overdue Flags

Every invoice generated in Enerpize carries a status — sent, viewed, paid, or overdue — and the system sends configurable reminders when due dates pass without payment. For a sole trader managing fifteen to twenty active clients, this replaces the mental overhead of remembering which invoices are outstanding, which clients are consistently late, and which accounts need a formal follow-up.

Five-Year Record Retention

The ATO requires invoice records to be retained for five years. Enerpize archives every invoice in your account and makes it searchable by client, date range, invoice number, or amount. If the ATO requests records in a compliance review — a scenario that becomes more likely as your revenue grows toward the $75K threshold — your complete invoice history is accessible in seconds, not buried in a Downloads folder across three laptops. See our plans and pricing page for the full feature set across each tier.

Key Takeaways

- Non-GST invoices must be titled 'Invoice,' never 'Tax Invoice.' Placing 'Tax Invoice' on a document when you are not GST-registered is a breach of the GST Act and creates a false document that disrupts your client's input tax credit records.

- Your ABN must appear on every invoice, even without GST. If an invoice is missing an ABN, the recipient is legally required to withhold 47% of the gross payment before remitting to you — a cash flow hit that is entirely preventable by filling in one field.

- The $75,000 GST threshold is a rolling 12-month calculation, not a calendar-year total. You can cross it mid-year without realising it. Monitor your rolling turnover monthly once you pass $60,000 in annual billings.

- The 'not a tax invoice' declaration is legally protective, not optional. It prevents a client's accountant from mistakenly treating your invoice as a tax invoice, which would trigger a GST credit claim the ATO would reject and trace back to your document.

- Pre-built payment clauses — including the 2% late fee — are enforceable only if communicated before or at the time of contracting. Restate your payment terms in your proposal or agreement before work begins, then repeat them on the invoice.

- State jurisdiction does not change the invoicing rules, but licensed trades may need to add state-specific licence numbers. The GST framework is federal and uniform. Industry licensing requirements are state-specific and sit on top of, not instead of, the standard invoice fields.

More than 40,000 businesses in the Enerpize ecosystem manage their invoicing, income tracking, and compliance in one system. For Australian businesses approaching the GST threshold, the switch from template to software takes minutes. Start for free, no credit card required.

Frequently Asked Questions

What is a non-GST invoice in Australia?

A non-GST invoice is a standard invoice issued by an Australian business that is not registered for Goods and Services Tax. It documents a sale and requests payment without charging, collecting, or remitting any GST. The document must be titled 'Invoice' — not 'Tax Invoice' — and must include the seller's ABN, the date of issue, a description of the goods or services, and the total amount payable. Businesses with annual GST turnover below $75,000 that have not voluntarily registered for GST issue this type of invoice for all their transactions.

Do I need an ABN on my invoice if I am not registered for GST?

Yes. Your ABN must appear on every invoice you issue, regardless of your GST registration status. The ABN is not a GST requirement — it is an ATO identification requirement for all businesses. If you issue an invoice without an ABN, the recipient is legally required to withhold 47% of the gross invoice amount before paying you, under the ATO's PAYG withholding rules for no-ABN situations. That withheld amount goes to the ATO, not to you, and you must claim it back at tax time.

Can I issue an invoice without GST if my turnover is below $75,000?

Yes. If your annual GST turnover — your gross business income excluding any GST already included — is below $75,000, GST registration is voluntary. If you have not registered, you are not authorised to charge GST, and your invoices must not include any GST amounts. You issue standard invoices with the 'not a tax invoice' declaration. Once your turnover crosses $75,000 on a rolling 12-month basis, you must register for GST within 21 days and switch to tax invoices for all subsequent transactions.

What should I write on my invoice instead of 'Tax Invoice'?

Write 'Invoice.' That is the legally correct title for a document issued by a business not registered for GST. You must not write 'Tax Invoice,' 'GST Invoice,' or any variant that implies GST is being charged, because those titles are reserved for documents issued by GST-registered businesses. In addition to the correct title, include the declaration at the bottom of your invoice: 'This is not a tax invoice as seller is not registered for GST.' This one-sentence statement protects you from the risk of a client accidentally treating your invoice as a tax invoice and attempting to claim an input tax credit from it.

If I am not registered for GST, how do I invoice?

Follow these five steps. First, confirm your ABN is current and include it on the invoice with the '(Not registered for GST)' qualifier. Second, title the document 'Invoice' — not 'Tax Invoice.' Third, describe the goods or services clearly with quantity and unit price per line. Fourth, state the total amount due without adding any GST component. Fifth, add your payment terms, bank details, and the 'not a tax invoice' declaration at the bottom. Send the invoice as a PDF, archive a copy for your records, and retain it for five years as required by the ATO.

What happens if I accidentally charge GST when I am not registered?

Charging GST when you are not registered for GST is an offence under the A New Tax System (Goods and Services Tax) Act 1999. The ATO can require you to remit the GST you collected without any offsetting input tax credit entitlement, because unregistered businesses cannot claim input tax credits. Your client's accountant may also flag the invoice as invalid during a BAS review, triggering a compliance inquiry. If you realise you have issued an invoice with GST incorrectly, issue a replacement invoice immediately with the correct zero-GST total and notify the client so they can substitute it in their records.

Can a sole trader in Australia invoice without GST?

Yes. A sole trader with annual GST turnover below $75,000 who has not registered for GST issues standard invoices without any GST component. The invoice must include the sole trader's ABN, the correct 'Invoice' title, a description of the services, the total amount, and the 'not a tax invoice' declaration. There is no simplified format for sole traders — the same ATO record-keeping rules apply. The practical difference from a company invoice is that the ABN is registered to the individual's name, and if the sole trader also operates under a trading name, both names should appear on the document.

How do I invoice without an ABN?

You should not issue invoices without an ABN if you are operating a business. Apply for an ABN through the Australian Business Register before issuing your first invoice — the application is free and takes minutes online, with most applications processed in 24 to 48 hours. If you are waiting for your ABN to be confirmed, contact the client, explain the situation, and ask them to hold payment until you can provide the number. If you send an invoice without an ABN and the client pays it in full anyway, the ATO may assess the payment as withholdable income with no withholding applied, which can create a liability for the payer. Do not put either party in that position — wait for the ABN.

About the Author

Omar El Bahr is a Senior Digital Growth Specialist at Enerpize, where he leads SEO, content strategy, and organic growth across international markets. He is a Forbes Communications Council contributor and has written for Entrepreneur on business communication and digital strategy.

Disclaimer

The information on this page is provided for general informational purposes only and does not constitute legal, tax, or financial advice. While every effort has been made to ensure accuracy at the time of publication, Australian GST laws and ATO requirements can change. Enerpize does not warrant that this content is complete, current, or applicable to your specific circumstances. Businesses should consult a registered tax agent or accountant before making compliance decisions. For the most current requirements, refer directly to the Australian Taxation Office at ato.gov.au.