Author : Haya Assem

Reviewed By : Enerpize Team

Chart Of Accounts: Definition, Structure, Importance

Table of contents:

- What is a Chart of Accounts?

- How a Chart of Accounts Works

- Chart of Accounts Structure

- COA Vs. General Ledger

- Why is a Chart of Accounts Important?

- Chart of Accounts Purpose

- How to Set Up a Chart of Accounts for Small Businesses

- How will Enerpize help you set up your chart of accounts?

- Final Thoughts

Accounting systems were less standardized before the economic and technological development. Businesses relied on basic ledgers and single-entry systems, often resulting in inconsistencies due to trial and error and informal categorization.

Parallel to economic development, there has been a need to reconsider businesses' and organizations' accounting and administrative systems by implementing comprehensive development programs and plans that employ current methods and executive tools.

The chart of accounts was created to offer an organized and uniform framework for categorizing and documenting financial transactions, ensuring accuracy and comparability in financial reporting.

What is a Chart of Accounts?

A chart of accounts is a listing of all financial accounts in a company’s general ledger whether it is commercial, industrial, or economic. This is achieved by allocating a unique number to each account or transaction. It is used to categorize transactions into groups, allowing you to track how transactions move in and out of a company.

The chart of accounts is also known as the accounting tree, as it is like a tree structure. It starts with main accounts, then branches into sub-accounts, and even more specialized ones.

For instance, take the Assets account – a main account. It has branches like current assets and non-current assets. Current assets, in turn, have more specific branches like inventory and cash.

Cash, for example, can be broken down into sub-branches such as cash in a national bank and cash in a foreign bank. It's like a detailed map of a company's financial transactions.

Read Also: Journal Entries for Bank Reconciliation: A Comprehensive Guide

How a Chart of Accounts Works

A Chart of Accounts (COA) is a structured framework that categorizes and organizes an organization's financial transactions. It organizes accounts into categories and subcategories, follows a hierarchical structure, and assigns unique identifiers.

The COA guarantees that the accounting equation is balanced, makes it easier to record transactions accurately, and acts as a basis for generating financial statements. It is adaptable to a company's specific needs, aids in financial analysis, and provides a standardized language for communicating financial information.

There's no one-size-fits-all format for a COA. Its structure depends on the unique needs and size of the business. The goal is to create a systematic and organized approach to financial management, ensuring accurate recording of transactions and facilitating the generation of meaningful financial reports.

Read Also: What is POS Transaction: Types, Benefits, & How They Work?

Chart of Accounts Structure

To ensure the company's accuracy and success in meeting its financial goals, it is essential to focus on precision when creating the chart of accounts from the beginning and ensuring the availability of all its aspects and components. This is particularly crucial as the chart of accounts is only prepared once, and any inaccuracies can have a severe influence on the company's financial position.

The Chart of Accounts is typically organized to display information in the order that it appears in financial statements, with balance sheet accounts listed first, followed by income statement accounts. This structural pattern ensures a systematic representation of financial data.

Read Also: Main Differences Between Income Statement and Balance Sheet

Subaccounts play a significant role in providing more detailed information about each main category, facilitating a more granular analysis of a company's financial transactions. The specific subaccounts utilized may vary depending on the nature of the business and its reporting needs.

To illustrate, here are examples of subaccounts for each of the main account categories:

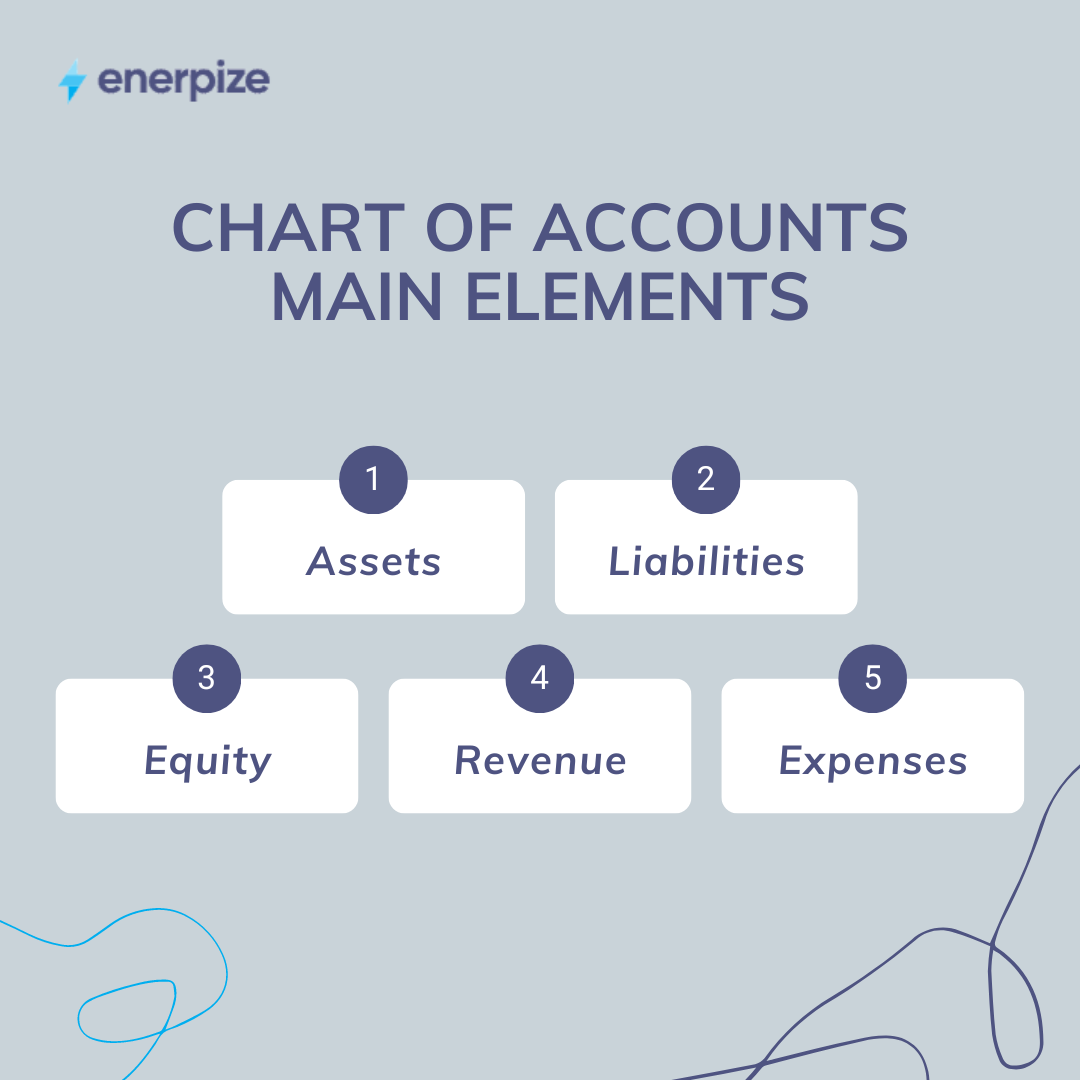

Assets

Current Assets:

Cash on Hand

Accounts Receivable

Fixed Assets:

Buildings

Lands

Vehicles

Machinery and Equipment

Read Also: What is the Difference Between Liquid and Illiquid Assets?

Liabilities

Current Liabilities:

Accounts Payable

Short-Term Loans

Long-Term Liabilities

Bank Loans

Mortgage Payable

Read Also: Tow to Calculate Total Liabilities

Equity

Common Stock

Capital

Retained Earnings

Revenue

Product Sales

Service Sales

Subscription Revenue

Expenses

Salaries and Wages

Depreciation Expenses

Utilities

Rent

COA Vs. General Ledger

The Chart of Accounts (COA) and the General Ledger (GL) are both essential components of accounting systems, although they serve different purposes. To make things clearer, here's a comparison of both components:

Points of Comparison | Chart Of Accounts | General Ledger |

Definition | A systematic list of all accounts an organization uses, organized according to financial statements and accounting principles. | A complete record of a company's financial transactions, organized by accounts specified in the Chart of Accounts. |

Structure | A hierarchical structure that includes main accounts, and subaccounts. Each account is assigned a unique identifier for easy identification. | Consists of individual ledger accounts, each corresponding to an account in the Chart of Accounts. |

Content | Lists all of the organization's accounts, including assets, liabilities, equity, revenue, and expenses. | Contains detailed transaction records, including date, description, debit/credit amounts, and the account affected. |

Example | Cash, Accounts Receivable, Revenue, Expenses, etc. | Specific transactions like a sale, purchase, payment, or receipt with corresponding amounts and dates. |

Read Also: General Ledger VS Subledger: A Comprehensive Guide

Why is a Chart of Accounts Important?

A chart of accounts is important because it helps keep track of a business's money in a clear and organized way. It provides a detailed picture of how the business is doing financially, making it easier for the owner to share accurate information with investors and shareholders.

Additionally, it helps the business follow the rules for financial reporting, ensuring that everything is in order and meets the standards. A well-prepared chart of accounts is like a map that helps everyone understand how the business is doing with its money.

Chart of Accounts Purpose

The chart of accounts is the cornerstone of the accounting system, serving as the primary factor in achieving the company's objectives. As a result, all businesses, whether startups, medium-sized, or large, strive to create it precisely, either manually or using the latest programs and systems. Here are the chart of accounts' key objectives:

Organization: A chart of accounts organizes financial transactions into separate accounts based on their nature (e.g., assets, liabilities, revenue, costs). This structure simplifies the tracking and evaluation of financial data.

Clarity: It provides a clear and uniform method for recording financial information, providing consistency throughout the business, and making communication and understanding easier among stakeholders.

Accuracy: By classifying transactions into specific accounts, a chart of accounts helps ensure accuracy in financial reporting. It reduces the risk of errors and discrepancies in the recording and analysis of financial data.

Decision-Making: The insights and information that the chart of accounts provides may help businesses make informed budgeting and strategic planning decisions.

Compliance: A chart of accounts ensures that the business's financial records align with these standards, reducing the risk of legal issues.

Analysis: A chart of accounts facilitates financial analysis by providing a detailed breakdown of each account. This analysis can reveal trends, identify areas for improvement, and support performance evaluation.

How to Set Up a Chart of Accounts for Small Businesses

Setting up a chart of accounts is an important step in organizing a small business's financial operations. Here's how to create a chart of accounts for your small business:

Understand your business structure

Different types of businesses may have different needs. Consider whether your business is a sole, partnership, corporation, or another structure, as this can influence your account setup.

Identify key categories

Determine the primary accounts you need. The most common categories are Assets, liabilities, equity, revenue, and expenses These categories will have sub-accounts for more detailed tracking.

List Basic Accounts

Create a list of basic accounts in each category. For example:

Assets include cash, accounts receivable, inventory, and equipment.

Liabilities include accounts payable and loans payable.

Equity: Owner's equity.

Revenue is generated through sales and services.Expenses include rent, utilities, salaries, and marketing.

Numeric System

For ease of reference, assign each account an identification code. For example, assets could start at 1000, liabilities at 2000, equity at 3000, revenue at 4000, and costs at 5000. This can help keep things in logical order.

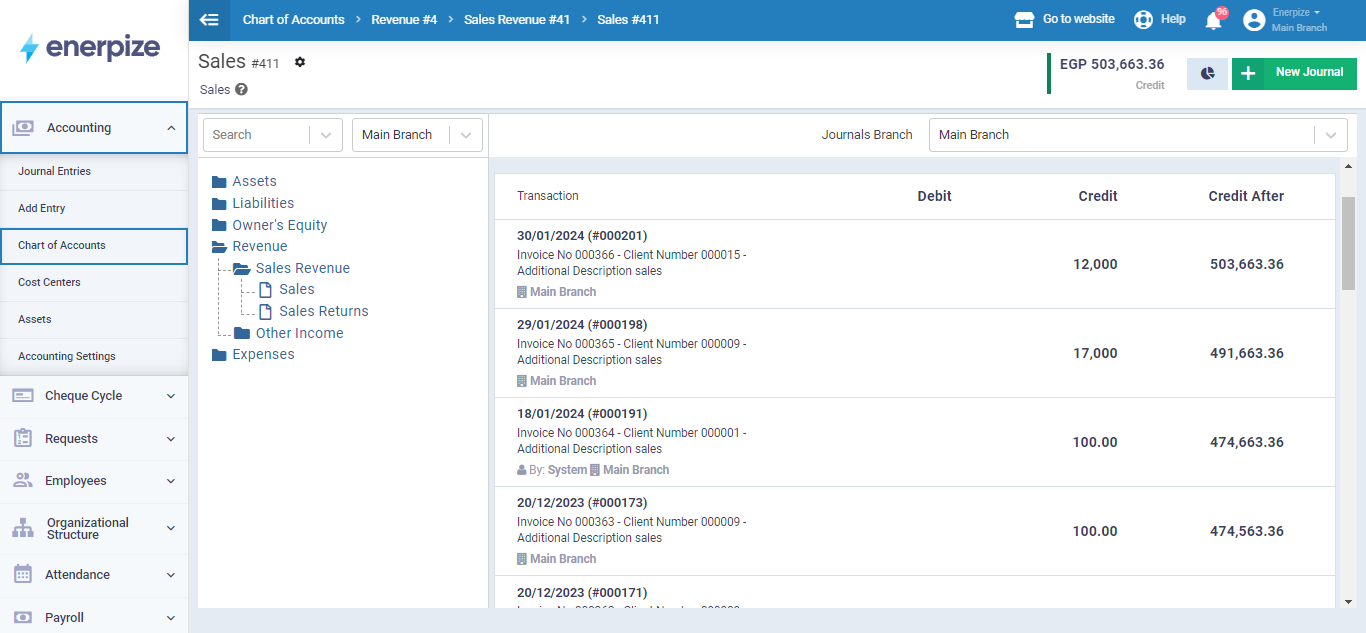

How will Enerpize help you set up your chart of accounts?

The online accounting software from Enerpize provides a pre-prepared chart of accounts that you can easily use or modify to suit the specific needs of your business. Entries are automatically recorded in the chart of accounts within the account to which the entry belongs, making your accounting work faster and more accurate than ever before.

You can sign up for Enerpize for free for a 14-day trial, during which you can explore the chart of accounts and all the features of the system.

Final Thoughts

The chart of accounts is a crucial tool in modern accounting, originating from the need for standardized financial systems. It organizes financial transactions into categories and subcategories, creating a hierarchical structure for accurate and consistent reporting.

This systematic approach ensures the balance of the accounting equation, aids in decision-making and facilitates compliance with financial standards. Precision in its setup is essential for its accuracy. Small businesses can benefit from tools like Enerpize, offering a pre-prepared chart of accounts for efficient financial management.

Accounting is easy with Enerpize.

Try our accounting module to manage your accountings

Accounting is easy with Enerpize.

Try our accounting module to manage your accountings