Author : Enerpize Team

Contribution Income Statement: A Comprehensive Guide

Table of contents:

- Key Takeaways

- What is the Contribution Margin Income Statement?

- Importance of Contribution Income Statement

- Contribution Margin Income Statement Formula

- Contribution Margin Income Statement Components

- Contribution Income Statement Example

- How To Prepare A Contribution Margin Income Statement?

- Contribution Margin Ratio Formula

- How to Improve Contribution Margin?

- Differences Between Contribution Income Statement and Traditional Income Statement

- How Can You Use Enerpize in the Contribution Income Statement?

- Final Thoughts

- FAQs

Outstanding companies know how to manage their profit and loss statements, so they grow. Fewer calculating companies do not, and so they go bust. That is why managing profits and losses goes beyond crunching numbers or settling accounts.

Instead, managing revenue and expenses is about diving deeper to categorize expenses as fixed or variable. Here is where a contribution income statement (aka contribution margin income statement) comes in. The contribution statement controls a company's expenses by separating costs by variability, enabling managers to decide which products perform well.

Contribution statements differ from and share basic similarities with traditional income statements. Traditional income statements mix and account for fixed and variable costs based on their relationship to production, whereas contribution statements separate costs based on variability alone. Both conclude with only one bottom line: operating income.

To understand what contribution income statements are, why they are super important to savvy managers, and how contribution and traditional income statements compare, read on.

This post is every calculating manager’s go-to guide on contribution income statements.

Key Takeaways

- Contribution margin income statements separate costs by variability (fixed vs. variable), giving managers clearer insight into profitability drivers.

- Unlike traditional income statements, contribution statements focus on contribution margin rather than gross profit, making them ideal for internal decision-making.

- Contribution margin is calculated by subtracting variable costs from sales revenue and shows how much is available to cover fixed costs and generate profit.

- These statements are especially useful for cost control, pricing decisions, product mix optimization, and break-even analysis.

- Contribution income statements provide more granular, actionable data than traditional income statements, helping managers respond quickly to operational changes.

- Traditional income statements are designed for external reporting, while contribution statements are used internally for planning and performance analysis.

- Improving contribution margin requires increasing revenue, reducing variable costs, or a combination of both.

- Key strategies to improve contribution margin include pricing optimization, cost reduction, product mix optimization, operational efficiency, and targeted marketing.

- Automating accounting and operational processes with ERP software like Enerpize enhances accuracy, efficiency, and real-time visibility into costs and margins.

- Using automated systems simplifies the preparation of contribution income statements and supports scalable, data-driven financial management.

What is the Contribution Margin Income Statement?

As noted, the contribution margin income statement is a statement of a company’s costs or expenses, regardless of whether they are used to produce goods or provide services. Fixed expenses include lease, payroll, insurance, etc. Meanwhile, variable expenses include raw materials, commissions, and loan interest.

The contribution margin income statement is also called a contribution income statement or a variable cost income statement. This is because contribution statements, unlike traditional income statements, are used to calculate a company’s contribution margin by subtracting variable costs from revenue. (More about traditional vs contribution income statement in a bit).

That said, you may wonder why managers would produce another statement, such as a contribution statement, and incur an additional accounting burden by creating a new revenue vs. expense statement when the income statement is standard and, unlike contribution statements, is reportable to regulatory authorities. Here is why.

Importance of Contribution Income Statement

As noted, contribution statements serve a different purpose than more traditional income statements. Here is why contribution statements are important (and loved by savvy managers).

Control Costs

Contribution income statements help managers keep track of expenses. By separating variable costs from fixed costs, financial planners, controllers, and accountants can identify specific operating patterns where revenue or expenses show unusual performance, up or down.

For example, mill line managers can decide whether to invest in capital equipment to maximize production of one or more products, reduce or eliminate production in other lines altogether, or switch to a whole new product line.

This is a decision at scale and of substantial consequences, where cost control is directly related to production, which in turn is directly related to entries in income statements, although not stated in contribution statements.

A practical example of this is a software company that used contribution income statements to uncover high variable support costs hidden under traditional reporting, leading to revised pricing tiers and improved overall contribution margins.

Read Also: Prepaid Expense Journal Entries: Importance, Examples & How to Record?

Perform Break-Even Analysis

Importantly, contribution statements can be used to perform break-even analysis. Companies—particularly startups—need to know at what point a given product, segment, subsidiary, or even the company as a whole would profit after investing in business activities for short or long periods.

For startups, a break-even analysis is a make-or-break situation. Generating profits faster at lower operating and non-operating costs distinguishes wise, fast-growth companies from comparable companies that burn cash without much regard for the bottom line.

Download Now: Free Break-Even Analysis Template

The bottom line is, having a contribution income statement pays.

Contribution Margin Income Statement Formula

A contribution margin income statement focuses on how sales revenue is used to cover variable costs and contribute toward fixed costs and profit. It is important to first understand how contribution margin is determined.

The contribution margin is calculated using the formula:

Contribution Margin = Sales Revenue − Variable Costs

This calculation highlights the relationship between revenue and costs that change with production or sales volume.

Contribution Margin Income Statement Components

The contribution margin income statement consists of several key elements, as follows:

1- Sales Revenue

Sales revenue is the total income generated from the sale of goods or services over a specific period. It reflects the gross inflow of economic benefits before any costs are deducted.

2- Variable Costs

Variable costs are expenses that change directly with the level of production or sales. As output increases, these costs rise; as output decreases, they fall. Common examples include raw materials, packaging, direct labor involved in production, sales commissions, and referral fees. Although some of these costs may be indirect, they are still incurred to make a sale and are therefore included.

3- Contribution Margin

The contribution margin is the amount remaining after subtracting variable costs from sales revenue. This figure shows how much revenue is available to cover fixed costs and eventually generate profit. It can be analyzed as a whole, per unit, or as a ratio.

4- Fixed Costs (Presented Below the Contribution Margin)

While fixed costs are not part of the contribution margin calculation itself, they are an essential element of the income statement. Fixed costs do not change with production or sales volume and include expenses such as rent, equipment, machinery, and administrative salaries. These costs must be covered by the contribution margin.

5- Operating Profit (or Loss)

After fixed costs are deducted from the contribution margin, the result is operating profit or loss. This shows whether the business is generating sufficient contribution to sustain operations and earn profit.

Recommended for you: Profit And Loss Statement: What It Is & How To Analyze?

In summary, the contribution margin income statement is built around sales revenue, variable costs, and contribution margin, with fixed costs deducted afterward. This structure makes it especially useful for profitability analysis, pricing decisions, and break-even analysis.

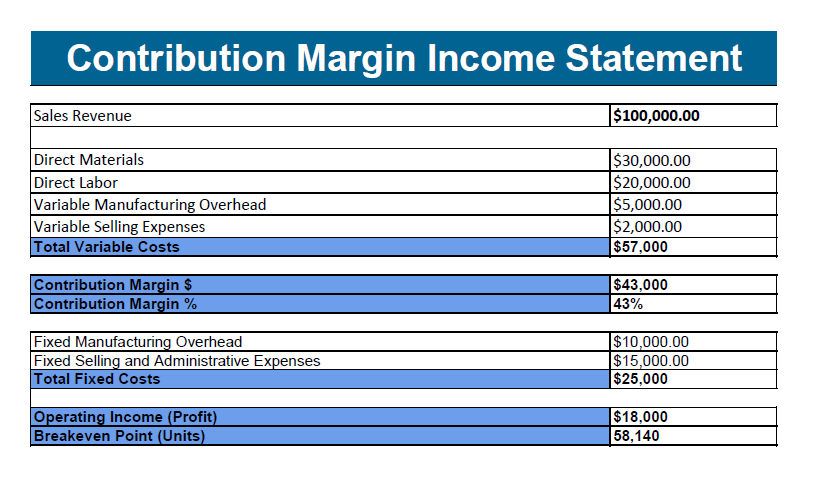

Contribution Income Statement Example

The above example shows, in bold, “Sales Revenue,” “Total Variable Costs,” “Contribution Margin,” “Total Fixed Costs,” and “Operating Income (Profit).” The operating income is calculated by:

- Identifying overall Sales Revenue ($100,000).

- Adding up Variable Costs ($57,000).

- Subtracting Variable Costs ($57,000) from Sales Revenue ($100,000) to get Contribution Margin ($43,000).

- Adding up Fixed Costs ($25,000).

- Subtracting Total Fixed Costs ($25,000) from Contribution Margin ($43,000) to get Operating Income ($18,000).

This operating income figure shows pre-tax profit, a positive signal for investors interested in the company.

Just like many financial statements and sheets, contribution statements can be created manually (i.e., using conventional paper-based documentation methods) or automatically (i.e., using automated ERP software).

Enerpize Accounting Software helps businesses automatically generate contribution margin statements, track revenues and costs in real time, and produce clear financial reports—without the complexity of traditional ERP systems.

Download Now: Free Contribution Margin Income Statement Excel Template

How To Prepare A Contribution Margin Income Statement?

Steps to Prepare a Contribution Margin Income Statement:

1- Calculate Total Sales Revenue

Determine the total revenue generated during the selected period, such as a month, quarter, or year.

2- Identify All Variable Costs

List all variable costs incurred during the same period that are directly related to production or sales.

3- Compute The Contribution Margin

Calculate the contribution margin by subtracting total variable costs from total sales revenue.

4- Determine Fixed Costs

Identify all fixed costs for the period, including rent, salaries, and administrative expenses.

Recommended for you: 30 Business Expense Categories List

5- Calculate Net Profit or Loss

Subtract total fixed costs from the contribution margin to determine the net profit or loss for the period.

Contribution Margin Ratio Formula

The Contribution Margin Ratio (CMR) expresses the contribution margin as a percentage of total sales revenue. It indicates how much of each dollar of sales contributes to covering fixed costs and generating profit.

The CMR can be calculated in two ways:

1- Total Contribution Margin Ratio

CMR = (Total Contribution Margin / Total Sales Revenue) × 100

2- Per Unit Contribution Margin Ratio

CMR per unit = (Selling Price per Unit – Variable Cost per Unit) / Selling Price per Unit × 100

This ratio is useful for analyzing profitability, pricing decisions, and performing break-even analysis.

If you want to analyze profitability easily, you can download our free Profitability Analysis Template immediately.

How to Improve Contribution Margin?

Improving contribution margin is a critical step toward building a more profitable and scalable business. Since contribution margin reflects the difference between revenue and variable costs, any improvement comes down to two core actions: increasing revenue or reducing variable costs. The most effective strategies integrate both into day-to-day business decisions.

Below are the key ways businesses can sustainably improve their contribution margin.

1- Optimize Pricing Strategies

Pricing is one of the fastest levers for improving contribution margin. Small, well-tested price changes can have a meaningful impact without significantly affecting demand.

Businesses should evaluate market demand, customer willingness to pay, competitor pricing, and cost structures to identify optimal price points. Techniques such as price elasticity analysis help determine how sensitive customers are to price changes. Tiered pricing and premium bundles can also capture more value from different customer segments, while selective price increases—when market conditions allow—can directly widen margins.

2. Reduce Variable and Direct Costs

Lowering variable costs improves contribution margin without relying on higher sales volumes. This starts with a detailed review of cost structures, particularly costs tied directly to production and delivery.

Negotiating better supplier terms, sourcing alternative materials, or switching to more cost-effective logistics providers can significantly reduce costs. Implementing lean practices, automating repetitive tasks, and closely tracking resource consumption help eliminate waste and improve efficiency without compromising product quality.

You might also find this helpful: Direct VS Indirect Costs: A Comprehensive Guide

3- Optimize Product Mix

Not all products contribute equally to profitability. Analysing contribution margins by product, service, channel, or region allows businesses to identify where profits are strongest.

Shifting marketing and sales efforts toward higher-margin products can improve overall margins even if total sales volume remains unchanged. Reducing excessive discounts, promotions, or low-margin bundles also helps preserve margin integrity and maintain the perceived value of products.

4- Improve Operational Efficiency

Operational efficiency directly affects variable labour and production costs. Streamlining workflows, minimising downtime, and improving inventory management all reduce unnecessary expenses.

Investing in the right tools—such as automation software, inventory systems, or production management solutions—can boost productivity and lower labour costs. Energy efficiency initiatives and better production planning further reduce operating costs while supporting long-term sustainability.

Enerpize ERP Software enhances operational efficiency by integrating core business functions into one system. Automating workflows across inventory, production, accounting, and HR, it reduces manual work, improves data accuracy, and supports better cost control and scalable growth.

5- Strengthen Marketing and Sales Effectiveness

Targeted marketing can improve contribution margin by attracting customers who are more likely to buy at full price or choose premium options.

By analysing customer data and purchasing patterns, businesses can focus their marketing spend on high-value segments. Upselling and cross-selling higher-margin products increase average order value without significantly increasing costs, improving contribution margin per sale.

6- Use Data to Guide Decisions

Segmenting contribution margins by product, region, or sales channel provides clear insight into where to invest, expand, or scale back. Data-driven decision-making ensures that pricing, cost control, and growth strategies are aligned with profitability goals rather than solely with revenue.

Improving contribution margin is not about a single change—it’s about aligning pricing, cost management, product mix, operations, and marketing around profitability. By consistently analysing performance and applying these strategies, businesses can strengthen margins, improve cash flow, and build a more resilient financial foundation.

Differences Between Contribution Income Statement and Traditional Income Statement

The traditional vs contribution income statement merits your particular attention as a business owner or executive manager. Here are four main differences between contribution and traditional income statements.

1- Cost Accounting

One significant difference between contribution and traditional income statements is how each is calculated, expense-wise, to arrive at the ultimate operating income line.

Contribution statements record all fixed and variable costs separately, e.g., based solely on variability. Meanwhile, traditional statements record all expenses related to production and management, i.e., whether an expense is production- or management-related, regardless of variability.

An additional benefit of using contribution statements may be the ability to use two different approaches to calculate a company’s operating income. Reconciling financial records is essential in cost accounting.

By double-checking accounts to individual entries, controllers and auditors ensure all records and calculations are mathematically correct. Since contribution statements are only used internally, as explained a bit, having such additional statements serves as an early-auditing system, akin to early warning systems that alert responders to potential dangers and prompt preemptive action.

Read Also: Journal Entries for Bank Reconciliation: A Comprehensive Guide

2- Different Margins

The margins calculated for the contribution and income statements differ. Traditional income statements calculate a company’s gross profit margin by subtracting the cost of goods sold COGS from revenue. Meanwhile, contribution margins are calculated by subtracting variable costs from revenue. Variable costs are only a subset of COGS, usually including fixed and variable costs.

This difference in margin calculation is a case in point. Specifically, while gross profit margins provide a general overview of how a given company generates revenue and incurs expenses, contribution margins offer a more granular, dynamic view of how costs are incurred to meet different operational needs over a short period.

Read Also: How to Calculate Cost of Goods Sold: Formula & Examples

3- General vs. Specific

Traditional and contribution statements also differ along a critical criterion: generality. That is, while traditional statements are, by definition, more general, accounting for a given company’s overall profitability over a given reporting period, contribution statements are granular, accounting for a more detailed account of variable and fixed costs.

The level of detail in contribution statements is a holy grail for savvy managers who want to closely examine cost dynamics daily to adjust quickly to any needed changes in sales operations, pricing, or production.

For example, assume a textile mill floor manager wants to dive deeper into how the cost of one or a group of input materials (say, woven cotton) is affecting the mill’s overall cost to decide whether to source woven cotton from a different supplier, rely less on cotton-based products, or switch to more innovative textile solutions. This understanding of cost sets contribution statements apart from traditional income statements, where a manager focuses more on overall profitability rather than per-product cost per se.

4- Internal vs. External Application

As noted, where contribution statements are used only internally, traditional income statements are more formal and reportable to relevant regulatory authorities.

The benefit of each, in terms of use, is substantial. Used internally, contribution statements serve as miniature income statements, from which planners, controllers, and auditors can identify short-term cost patterns. Traditional income statements, however, are geared for external users - such as external auditors, regulatory authorities, and public oversight - where statement format and content are particularly important to be accepted as formal financial statements.

This difference in application is similar to cost accounting in one important way. Specifically, contribution statements—used internally only—act as an early warning system for all involved financial planners, controllers, and auditors. So, like in cost accounting, contribution statements provide invaluable accounting information at a more granular level, allowing internal stakeholders to adjust and reconcile accounts early on before formalizing them in traditional income statements.

How Can You Use Enerpize in the Contribution Income Statement?

Using Enerpize to generate accurate and compliant contribution statements is guaranteed to businesses looking for a leading, cost-effective, and comprehensive accounting operations management solution.

To get a sense of what Enerpize can offer to help with contribution income statement and more, here are only a few features and benefits:

- Track and manage your earnings and spend anytime, anywhere.

- Show a snapshot view of all revenue, expenses, and net income.

- Choose how to calculate income from invoices within preset date ranges and get accurate net profit calculations.

- Define tax brackets and classes (e.g., GST, VAT, EXP, etc.) based on monthly, quarterly, and annual reporting requirements.

- Use Enerpize’s customizable cost centers to monitor operating expenses, control overall spending, and calculate profitability per product or department.

- Use Enerpize’s comprehensive and automated Chart of Accounts to list identified accounts and record transactions in your general ledger.

- Maintain a record of all transactions over your company’s life and always get accurate and comprehensive financial statements and reports whenever you need them for internal or external use.

- Categorize expenses, vendors, and customers per group, tier, payment range, and more.

- Set your currency and tax requirements as and when needed for internal control and external regulatory purposes.

- Speed up customer payments with Enerpize’s dedicated customer portal.

- Enable various payment options to speed up customer payments, subject to certain payment restrictions in some jurisdictions.

- Dynamically set commission structures to manage commission payments for your sales teams.

- Create customizable offers for your loyal and prospective customers to drive revenue and unlock upsell opportunities.

- Create customizable estimates and quotes to expedite sales and improve customer satisfaction.

These features and benefits will set your company apart from the competition. Invest wisely in Enerpize as your accounting management solution.

Enerpize is primarily an online accounting software for businesses with varying and evolving needs. As such, Enterprise is best positioned to cater to ever-changing business needs, particularly cost structuring in response to market dynamics.

Try us for 14 days free, start reaping the expected and unexpected rewards and benefits, and leave your accounting concerns behind.

Final Thoughts

Contribution income statements are often overlooked as important financial statements for managing costs and planning for business growth. Used by savvy business owners and executive managers, contribution statements provide insights not obtainable elsewhere in accounting management’s repertoire of financial statements, sheets, and reports.

Contribution statements, which include a full record of all variable and fixed costs, help business owners and executive managers control costs and perform break-even analysis, both of which are critical in production operations planning and demand forecasting.

Traditional and contribution statements differ in four important areas:

- Cost Accounting: Both arrive at an ultimate operating income line. However, whereas traditional statements calculate all production and management expenses, contribution statements calculate fixed and variable costs based solely on availability.

- Different Margins: Where traditional statements calculate a company’s gross profit margin (Revenue - COGS), contribution statements calculate contribution margins (Revenue - Variable Costs).

- General vs. Specific: Where traditional statements account for a company’s overall profitability, contribution statements are cost-specific and limited to accounting for fixed and variable costs to calculate a company’s contribution margin.

- Internal vs. External Application: Where contribution statements are intended for internal use only, traditional income statements are, by definition, intended for external auditing and regulatory purposes.

Contribution statements can be created manually or automatically.

Choosing the solution that best suits your business for managing your accounting operations, including creating contribution statements, depends on your needs and market dynamics. Make no mistake, opting for your best-fit accounting software.

FAQs

What is the difference between traditional income statement and contribution income statement?

The main difference lies in how costs are classified and analyzed. A traditional income statement groups expenses by function (such as cost of goods sold, selling, or administrative expenses) and mixes fixed and variable costs. It focuses on calculating gross profit and is primarily used for external reporting and regulatory purposes.

In contrast, a contribution income statement separates costs strictly by behavior—fixed versus variable—regardless of their function. It calculates contribution margin by subtracting variable costs from sales revenue, showing how much revenue is available to cover fixed costs and generate profit. Contribution income statements are used internally to support pricing decisions, cost control, product mix analysis, and break-even analysis.

How to fill out a contribution income statement?

You can prepare a contribution income statement by following these steps:

- Calculate Total Sales Revenue: Determine total income generated from sales during the period.

- Identify Variable Costs: List costs that change with production or sales volume.

- Calculate Total Variable Costs: Add all variable costs together.

- Compute Contribution Margin: Subtract total variable costs from sales revenue.

- Identify Fixed Costs: List expenses that remain constant regardless of activity level.

- Determine Operating Profit or Loss: Subtract fixed costs from the contribution margin.

Following these steps helps clearly show how revenue covers variable costs, contributes to fixed costs, and generates profit.

Contribution income statements are easy with Enerpize.

Try our accounting module to create financial statements easily.

Contribution income statements are easy with Enerpize.

Try our accounting module to create financial statements easily.