Author : Ghofran Adel

What are Liabilities in Accounting? A Complete Guide to Types & Examples

Table of contents:

- Key Points

- What Are Liabilities?

- Why Liabilities Matter in Business Accounting?

- How Liabilities Fit Into the Accounting Equation?

- Where Liabilities Appear on the Balance Sheet?

- Types of Liabilities

- Common Examples of Liabilities

- Liabilities vs Assets

- Liabilities vs Expenses

- How to Calculate Total Liabilities

- How to Analyze Liabilities?

- Common Mistakes When Classifying Liabilities

- How Enerpize Helps You Manage Liabilities

- FAQs About Liabilities

- Conclusion

One of the most important concepts in accounting is liabilities, which represent all the financial commitments and debts a company owes to external parties such as suppliers, banks, employees, and, of course, government entities. Liabilities play a pivotal and crucial role in determining the true financial position of any company or institution, as it is impossible to understand a company's true strength or the extent of the financial risks it may face without a thorough analysis of its liabilities.

This article serves as your comprehensive guide to understanding liabilities and their fundamentals, helping business owners make informed financial decisions. We will discuss how liabilities appear on the balance sheet and within the financial statements.

Key Points:

- Liabilities are debts or financial obligations that a company has and must repay in the future.

- There are three types of liabilities: current (short-term), long-term, and contingent. They differ in their repayment period and nature.

- Financial liabilities appear on the balance sheet under liabilities.

- Classifying liabilities helps assess a company's liquidity, ability to pay, and financial stability.

- Analyzing liabilities helps in making more informed financial decisions.

- Effective liabilities management contributes to improving the accuracy of financial reports and enhancing the company's stability.

What Are Liabilities?

Liabilities are the sum of debts and financial obligations that companies or institutions owe to external parties, including banks, suppliers, government entities, and others. These liabilities represent amounts the company must pay to the relevant parties in cash, goods, or services.

The liabilities are directly related to the basic accounting equation, which states:

Assets = Liabilities + Equity

Why Liabilities Matter in Business Accounting?

We cannot consider liabilities as mere numbers on financial statements. Rather, they are a fundamental and crucial element in understanding a company's or organization's financial health and its ability to continue, grow, and expand. Liabilities directly impact liquidity.

The importance of liabilities stems from the following:

- Liabilities help provide a clear picture of the size of the debt.

- Liabilities directly affect cash flow.

- Liabilities determine a company's ability to repay its debts on schedule.

- Liabilities assist in making informed decisions regarding the company's or organization's expansion or growth.

How Liabilities Fit Into the Accounting Equation?

Financial liabilities are included in the basic accounting equation for preparing financial statements:

Assets = Financial Liabilities + Equity

Upon closer examination of this equation, we see that it reflects how all of a company's assets are financed through liabilities to external parties or through equity in its assets.

Liabilities naturally appear in the equation when a company borrows from a bank, as this leads to an increase in assets and a corresponding increase in liabilities. Similarly, purchasing goods results in recording a liability to suppliers without directly impacting liquidity. Liabilities also include expenses such as salaries and outstanding invoices, which are considered liabilities until paid.

Thus, the equation always remains balanced, helping to understand how a company finances its assets. The true impact of liabilities is reflected on the balance sheet.

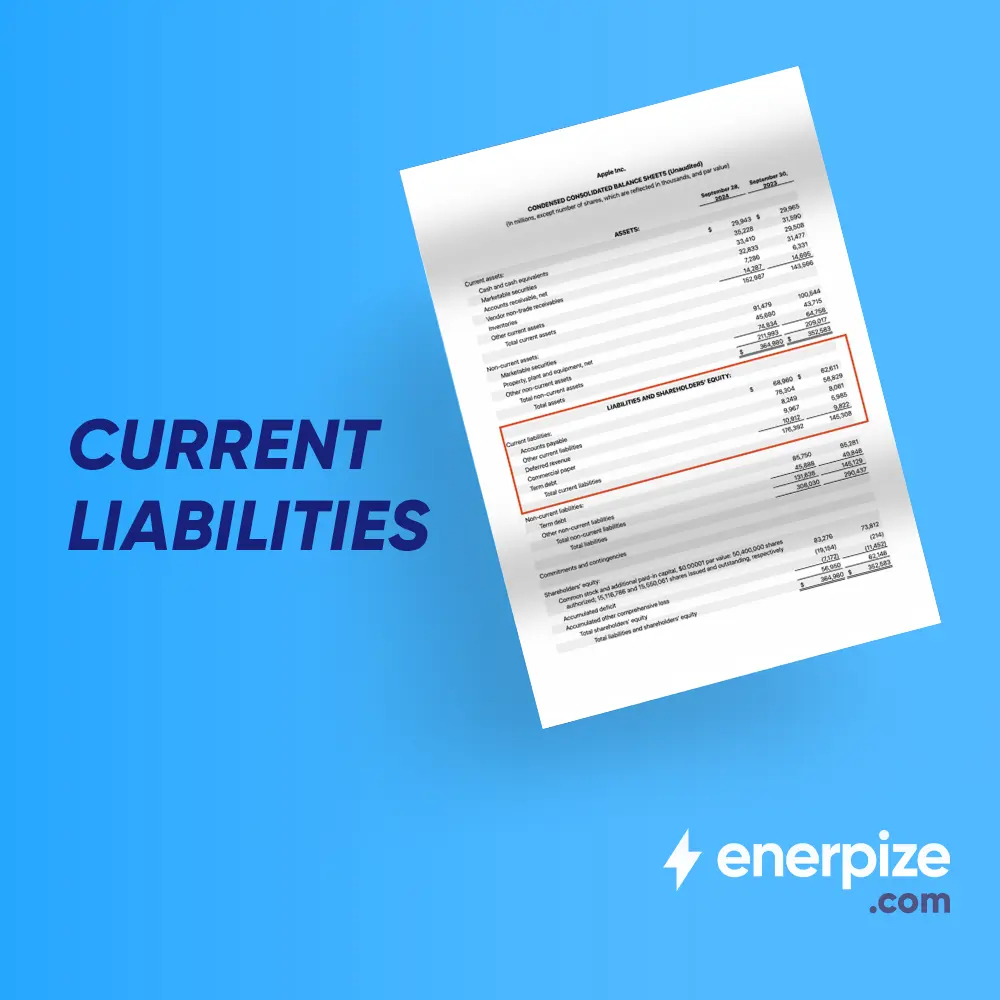

Where Liabilities Appear on the Balance Sheet?

Financial obligations appear on the balance sheet under the liabilities side. They are listed separately from assets and equity to clarify the source of funding. Liabilities are generally divided into two main categories:

- Short-term liabilities: Debts and amounts due that must be paid within one year, such as salaries and short-term loans.

- Long-term liabilities: Obligations that extend for periods longer than one year, such as loans and bonds.

This categorization of liabilities aims to help business owners and investors assess a company's financial performance, understand its long-term obligations, and evaluate their impact on the company's stability and financial position.

If you want a ready template to list your business liabilities, download our free balance sheet template.

Types of Liabilities

Financial liabilities are classified into three types:

Current liabilities

These are liabilities that arise during the company's normal operating cycle or are expected to be repaid within one year.

For more: What are Current Liabilities: Definition, Examples

Non-current liabilities

These are liabilities whose repayment period extends beyond one year and usually arise from long-term financing such as loans and long-term leases.

Explore more: Long Term Liabilities In Accounting: Examples And How To Calculate

Contingent liabilities

These are defined as liabilities that could potentially occur, such as lawsuits or obligations to customers.

Recommended for you: Contingent Liabilities: Meaning, Examples, and How to Record

| Type | Duration | Examples |

| Current | One year | Salaries and taxes |

| Non-current | More than one year | Loans and long-term leases |

| Contingent | Unspecified | Liabilities and guarantees |

Common Examples of Liabilities

A table showing some examples of liabilities and the type to which these obligations belong:

| Liability | Description | Classification |

| Debts to suppliers | Payments owed for goods or services | Current |

| Salaries | Employee salaries | Current |

| Taxes | Unpaid taxes | Current |

| Loan interest | Loan interest | Current |

| Loans | Bank financing | Nom-Current |

| Mortgages | Asset-secured loans | Nom-Current |

| Rent | Long-term leases | Nom-Current |

| Revenue | Payments received for services not yet rendered | Current |

| Security liabilities | Maintenance obligations on products or warranties | Contingent |

Liabilities vs Assets:

The difference between defining financial liabilities and assets is important, as each represents a different aspect of a company's financial position.

- Assets: Reflect what a company or organization owns.

- Financial Liabilities: Are categorized as liabilities or equity.

The two definitions are directly related by the following equation:

Assets = Liabilities + Equity

This equation illustrates that any asset owned by a company is financed through liabilities or owner's funds. On the other hand, an increase in assets may result from an increase in liabilities, and simultaneously, it also reflects an increase in the liabilities themselves.

The table below shows the difference between liabilities and assets:

| Item | Assets | Liabilities |

| Purpose | Used to generate future economic benefits | Must be settled or fulfilled in the future |

| Examples | Cash, inventory, equipment, property | Accounts payable, loans, accrued expenses, taxes payable |

| Balance Sheet Position | Recorded on the assets side | Recorded on the liabilities side (liabilities section) |

Liabilities vs Expenses

Financial liabilities and expenses have different roles within financial statements. Financial liabilities are commitments a company has to fulfill. Expenses, on the other hand, are costs incurred by a company during a specific period and are recorded in the income statement to determine net profit or loss.

The difference between them is as follows:

- Expenses = Costs incurred

- Liabilities = Amount not yet paid

However, there are instances where expenses can become liabilities if they are recorded before payment is made.

You may also like: Accrued Liabilities in Accounting: Meaning and Examples

How to Calculate Total Liabilities:

The primary purpose of calculating total liabilities is to understand the size of a company's or organization's debt.

Total financial liabilities can be calculated using the following formula:

Total Liabilities = Current Liabilities + Long-Term Liabilities

Or, using the formula:

Total Liabilities = Total Assets - Equity

A practical example of calculating total financial liabilities:

| Statement | Value |

| Total Assets | 500,000$ |

| Equity | 300,000$ |

| Total Liabilities | 200,000$ |

Also read How to Calculate Liabilities: A Detailed Guide with Examples

How to Analyze Liabilities?

The financial obligations of companies and institutions are analyzed through several steps:

- Reviewing the due dates of obligations to determine whether they are long-term or short-term.

- Classifying obligations as current or non-current to determine repayment priority and assess the company's financial stability.

- Comparing total liabilities with assets to determine the company's ability to cover its debts.

- Comparing equity with liabilities to measure the company's reliance on debt financing.

- Analyzing the company's or institution's cash flows to determine its ability to meet payment deadlines.

Common Mistakes When Classifying Liabilities

Some of the most common mistakes when classifying liabilities include:

- Considering expenses as liabilities and liabilities as expenses.

- Recording long-term liabilities as current liabilities and vice versa leads to a distorted view of liquidity.

- Ignoring that some long-term loans have a portion due within the current year.

- Incorrectly including contingent liabilities results in an exaggerated debt level.

- Ignoring unpaid salaries and bills creates an inaccurate picture of the financial position.

How Enerpize Helps You Manage Liabilities:

Enerpize accounting software aims to help companies manage their liabilities accurately and easily by consolidating financial obligations within a single accounting system that allows for monitoring and control.

The system helps organize payments and due dates to avoid late payments and reduce financial risks. Enerpize supports the correct and accurate classification of liabilities within the balance sheet.

Furthermore, Enerpize generates robust financial reports that help companies and business owners analyze crises, understand their debts, and track liabilities by type to avoid any surprises or financial pressures.

FAQs About Liabilities

What does liability mean?

In accounting terms, the term "commitment" refers to obligations or debts that must be repaid in the future.

Is a liability something you owe?

Yes, a commitment means a debt or financial obligation on the part of the company towards other parties, such as banks, suppliers, and others. However, not every commitment is a debt; some commitments are in the form of outstanding payments, such as salaries.

What is the most common liability?

The most common type of liability is accounts payable, which are amounts owed by the company for goods or services purchased.

This is followed by unpaid salaries and invoices.

What are the 10 current liabilities?

Common examples of current liabilities that must be paid within one year include:

- Suppliers

- Salaries

- Taxes

- Accrued Interest

- Short-term Loans

- Deferred Revenue

- Accrued Expenses

- Dividends Payable

- Short-term Bank Debts

- Short-term Leases.

Conclusion

In conclusion, liabilities are a fundamental element in understanding the financial position of any company or organization, as they reflect the company's debt.

By analyzing and classifying liabilities, decision-makers can assess the company's ability to repay and understand its financial health.

Including liabilities correctly within the balance sheet and linking them to the accounting equation helps provide an accurate and comprehensive financial picture.

Accurate liability management and proper analysis are essential steps toward better financial decisions and the sustainability of companies.