Posted on 25 May 2026

Free Australian GST Invoice Template Download: Excel, Word, PDF & Google Sheets

- Includes all 7 ATO-required fields for GST-registered businesses, covering both sales under $1,000 and sales of $1,000 or more.

- Pre-built GST line-item breakdown calculates the 10% rate automatically so your Business Activity Statement figures are always accurate.

- ABN field, tax invoice title, and buyer identity section are built in, covering every mandatory requirement the Australian Taxation Office specifies.

- Download the Australian GST invoice template in Word, Excel, PDF, Google Sheets, or Google Docs.

An Australian GST invoice template is a ready-to-use billing document for GST-registered businesses in Australia that displays the seller's ABN, a line-by-line GST breakdown, and all fields the ATO requires so customers can claim their input tax credits without a compliance issue.

What Is an Australian GST Invoice Template?

An Australian GST invoice template is a pre-structured billing document that contains every field required by the Australian Taxation Office for taxable sales. It differs from a plain invoice in one decisive way: it explicitly separates the 10% Goods and Services Tax from the base price, either as a line item against each product or service, or as a total-price-inclusive statement where GST equals exactly one-eleventh of the invoice total.

Every GST-registered business in Australia must issue a tax invoice, not a standard invoice, for any taxable sale over $82.50 (including GST). Failing to provide one within 28 days of a customer request is a compliance breach under the GST Act. The template removes any ambiguity: if the required fields are present, the invoice is valid; if any are missing, the buyer cannot claim an input tax credit and will come back to you.

The practical difference between a generic invoice template and an Australian GST invoice template is not cosmetic. The words "Tax Invoice" must appear on the document. The seller's ABN must be visible. For sales of $1,000 or more, the buyer's identity or ABN must be included. A template that skips any of these is not ATO-compliant, regardless of how professional it looks.

Generate a compliant Australian GST invoice in seconds inside Enerpize. Start for free, no credit card required.

Who Needs a GST Invoice Template in Australia?

The requirement is tied to GST registration, not business size. If your annual GST turnover reaches $75,000 (or $150,000 for non-profit organisations), you must register for GST and issue tax invoices. Below that threshold, registration is voluntary, but once you are registered, the obligation to provide compliant tax invoices applies to every taxable sale above the $82.50 threshold.

Sole Traders

A sole trader's ABN sits where a company's ACN would appear on a corporate invoice. The document structure is identical: the title must read "Tax Invoice," the ABN must be displayed, and GST must be shown explicitly. There is no simplified format for sole traders under ATO rules. The same 7-field requirement applies regardless of whether you are a one-person trade business or a 50-person consultancy.

One common sole trader mistake is issuing invoices without the words "Tax Invoice" because the template they downloaded said "Invoice" at the top. That document cannot be used by a GST-registered client to claim an input tax credit. If the client's accountant catches it at BAS time, they will ask you to reissue.

Small Businesses and Startups

Australian small businesses issuing invoices across multiple clients and projects benefit most from a template with automatic GST calculation. A manual rounding error on a multi-line invoice creates a discrepancy between what the buyer claims as an input tax credit and what you remit to the ATO at BAS time. The ATO's total invoice rule and taxable supply rule both exist specifically to handle rounding across line items, so the template's formula needs to match one of those two methods.

Freelancers and Contractors

Freelancers who cross the $75,000 turnover threshold mid-year face a registration trigger that catches many off guard. From the day registration is effective, all invoices for taxable services must comply. A freelancer invoicing a GST-registered client without a valid tax invoice is not just inconveniencing the client; they are creating a documented compliance gap that becomes visible at the client's next BAS lodgement.

Businesses with International Clients

Not all sales by Australian businesses are subject to GST. Exported services and goods are generally GST-free under Division 38 of the GST Act, meaning the invoice still needs to exist and display the ABN, but the GST amount is zero. An Australian GST invoice template that supports a 0% GST toggle per line item handles this correctly. Billing an overseas client at 10% GST when the sale is actually GST-free creates an overcollection problem and a refund obligation with the ATO.

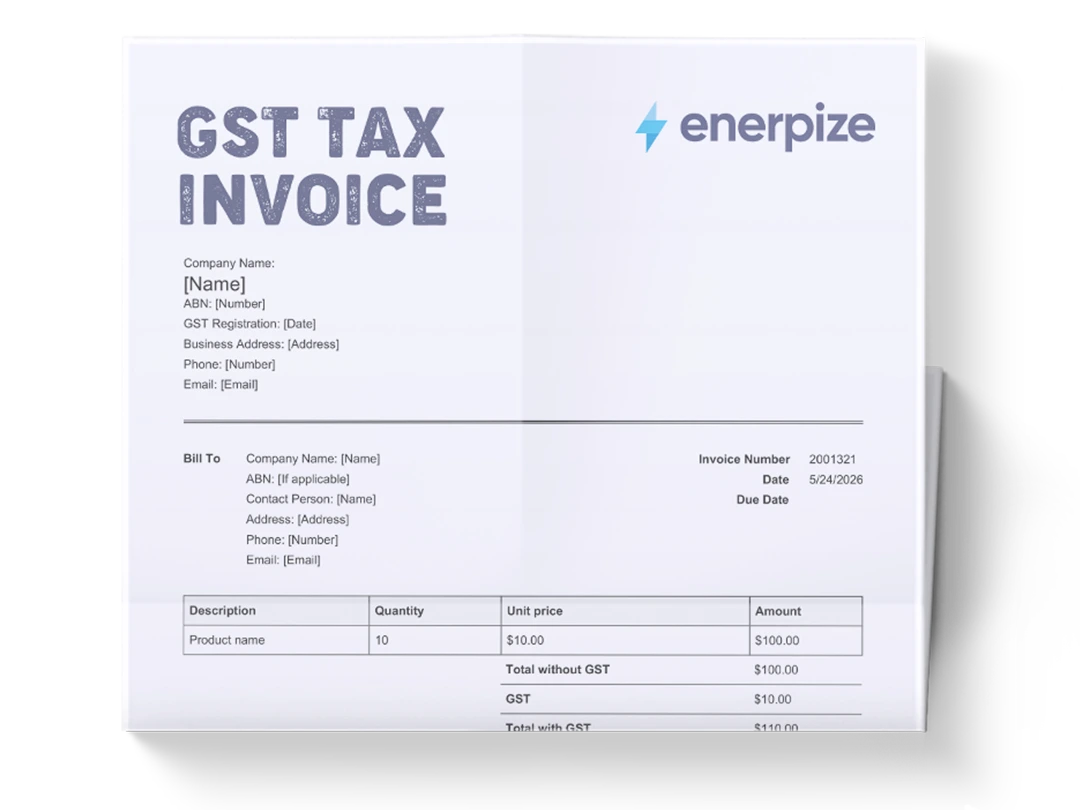

What a Valid Australian GST Invoice Template Must Include

The ATO sets out the requirements in GSTR 2013/1 and the Tax Administration Act. The exact fields differ slightly based on the invoice total. Below are both tiers.

For Sales Under $1,000 (GST-Inclusive): 7 Required Fields

| Required Field | What It Must Show |

| 1. Title | The words "Tax Invoice" or equivalent. Without this, the document is not a tax invoice regardless of its content. |

| 2. Seller's Identity | Your business name or trading name. Contact details are not legally required but are strongly recommended. |

| 3. Seller's ABN | Your Australian Business Number in full. No abbreviations. |

| 4. Date of Issue | The date the invoice was issued, not the date services were delivered. |

| 5. Description of Sale | A brief description including quantity (if applicable) and price for each item or service. |

| 6. GST Amount | Either shown per line item or as a statement that the total price includes GST (only valid when GST equals exactly 1/11 of the total). |

| 7. Extent of Taxable Sale | Clear indication of which items carry GST and which are GST-free or input-taxed. |

For Sales of $1,000 or More (GST-Inclusive): 8th Field Required

Every field listed above applies, plus the buyer's identity or ABN must appear on the invoice. This is a hard ATO requirement, not a best-practice suggestion. A tax invoice for $1,000+ that omits the buyer's details is not valid, and the buyer cannot claim an input tax credit on it.

If your tax invoices consistently meet the $1,000-or-more standard, they also satisfy the requirements for smaller sales. Enerpize automatically includes the buyer's ABN field on every invoice so you never have to remember which threshold you are near.

Worked Example: Multi-Line GST Invoice

This is how a valid Australian GST invoice with both taxable and GST-free items should present the numbers:

| Description | Qty | Unit Price (excl. GST) | GST (10%) | Total (incl. GST) |

| Cloud accounting subscription (taxable) | 1 | $299.00 | $29.90 | $328.90 |

| ATO compliance training (GST-free) | 2 | $150.00 | $0.00 | $300.00 |

| Onsite setup service (taxable) | 1 | $120.00 | $12.00 | $132.00 |

| TOTAL | $719.00 | $41.90 | $760.90 |

Each taxable line shows its GST amount separately, and the GST-free training line is clearly labelled $0.00. The total-price-inclusive statement method is not available here because this invoice contains a mix of taxable and GST-free supplies. Per-line GST breakdown is the only format the ATO accepts for mixed-supply invoices, regardless of the total amount.

The $82.50 Rule, the 28-Day Window, and What Happens When You Miss Them

Most template pages list the $82.50 threshold as a single bullet point. Here is what it actually means in practice, because the operational consequence is what matters.

If a customer who is also GST-registered asks you for a tax invoice on a sale over $82.50, you have 28 calendar days to provide it. Not 28 business days. 28 calendar days. If you miss that window, you have technically breached your obligation under section 29-70 of the A New Tax System (Goods and Services Tax) Act 1999. The customer can report the gap to the ATO, and while enforcement at this level is rare for individual instances, a pattern of missing the deadline becomes part of your compliance record.

The more immediate problem is the buyer's BAS. If the buyer's accountant needs to lodge a Business Activity Statement and the tax invoice has not arrived, the input tax credit cannot be claimed in that period. The buyer either lodges without the credit (losing money) or delays lodgement (risking a late penalty). Either outcome damages the business relationship.

The template solves this by making invoicing fast enough that you send it the day the transaction closes, not when you get around to admin. Enerpize generates the invoice at point of sale, emails it directly to the client, and archives the record so the 28-day window never becomes a question.

How to Express GST on Your Invoice: The Two ATO-Approved Methods

The ATO accepts two formats for displaying GST. Which one you can use depends on the invoice total and whether all items carry the same GST treatment.

Method 1: Line-Item GST Breakdown

Show the GST amount alongside each line item. This is the only acceptable method for invoices totalling $1,000 or more (GST-inclusive), and the only correct approach when your invoice contains a mix of taxable and GST-free items at any price point. Each taxable line shows its GST; each GST-free line shows $0.00 or is labelled “GST-free.”

Method 2: Total-Price-Inclusive Statement

If the invoice total is under $1,000 and every item on it is taxable at the standard 10% rate, you can instead write: "Total price includes GST of [amount]." This method is only valid when the GST is exactly one-eleventh of the total price. If the arithmetic does not produce a clean one-eleventh result, Method 1 is your only option.

A practical example: an invoice for $770 where everything is taxable at 10% can state "Total price includes GST of $70." That is $770 divided by 11, which is exactly $70. If you have one GST-free item in the mix, that calculation no longer applies and you must itemize.

The 1/11th Rounding Rule

When an invoice has multiple taxable line items, rounding can create a one-cent discrepancy between the sum of individual GST amounts and the total GST. The ATO provides two approved approaches: the total invoice rule (calculate GST on the combined pre-tax total, then round once) and the taxable supply rule (round each line's GST individually, then sum them). You and your customer do not need to use the same method. The template handles this automatically so neither party carries a BAS reconciliation error into their quarterly lodgement.

Recipient-Created Tax Invoices (RCTIs): When the Buyer Issues the Invoice

In most transactions, the supplier issues the tax invoice. But Australian tax law provides for a specific exception called a recipient-created tax invoice (RCTI), where the buyer generates the invoice instead of the seller. This arrangement is common in agriculture, mining, construction, and media, and it has strict requirements most template pages never mention.

An RCTI is only valid when both parties are GST-registered at the time the RCTI is issued, both have agreed in writing that the buyer will issue the RCTI and the seller will not issue a standard tax invoice for the same supply, and the ATO's RCTI Determination 2023 covers the type of goods or services involved.

The RCTI must still contain all the fields of a standard tax invoice, plus a statement that it is a recipient-created tax invoice (not a standard tax invoice) and confirmation that GST is payable by the supplier. If you are a supplier operating under an RCTI arrangement, you cannot also issue your own tax invoice for the same transaction. Doing so creates a double-claiming risk for the buyer.

Enerpize supports RCTI-style invoicing for businesses in construction and agricultural supply chains where this arrangement is standard. The buyer-identity and ABN fields, along with the payable-by-supplier notation, are configurable within the invoicing module.

eInvoicing and the Peppol Framework: The ATO Update That Changes the Rules

In August 2025, the ATO updated its guidance on eInvoicing to clarify something that most businesses and their accountants do not yet know: an eInvoice issued under the Australian-New Zealand Peppol specification does not need to include the words "Tax Invoice" to be legally valid.

Australia adopted the Peppol framework as its standard for electronic invoice exchange between business accounting systems. Under the A-NZ Invoice Specification, the structured data fields within the eInvoice satisfy the ATO's "document is intended to be a tax invoice" requirement automatically, even without the traditional heading. This matters for businesses that want to move to fully automated invoice exchange with their clients without reformatting existing document templates.

For businesses not yet using Peppol eInvoicing, the traditional template approach remains valid. A PDF emailed to a client, a printed page posted by mail, or a digital document accessed through an online portal all satisfy the ATO's requirements as long as every mandatory field is present. The format (paper or digital) has never been the issue. The content is.

Enerpize supports eInvoicing exchange and generates invoices that comply with both the traditional tax invoice format and the Peppol structured data requirements, so switching between delivery methods does not require rebuilding your invoice template. For Australian small businesses evaluating a full system rather than a standalone template, see how Enerpize compares as an ERP solution.

The BAS Connection: Why Every Invoice You Issue Feeds Your Quarterly Lodgement

This is the most commercially important reason to use a compliant Australian GST invoice template rather than a generic one.

Every GST amount shown on a tax invoice you issue becomes part of your GST collected figure for the quarter. Every GST amount on a valid tax invoice you receive from a supplier becomes part of your input tax credits for the quarter. The difference between those two numbers is what you pay the ATO (or what the ATO owes you) when you lodge your Business Activity Statement.

If an invoice you issued is missing a required field and your client's accountant flags it as invalid at BAS time, two things happen simultaneously. First, your client cannot claim the input tax credit on that invoice, which means they overpay their BAS by the GST amount. Second, if the invoice was for a large enough amount, they will contact you to reissue a corrected version, which delays their lodgement. If the corrected invoice arrives after the BAS period closes, the credit rolls into the next quarter.

An invalid invoice does not mean the GST disappears. It means the credit is delayed, the relationship is strained, and you have created a compliance record that the ATO can see when it reviews BAS patterns across related businesses.

The template prevents this by making compliance automatic. If the required fields are pre-built and the GST calculation runs on a formula rather than manual arithmetic, the invoice is either correct or it cannot be submitted. There is no middle ground where a mistake slips through.

Generate GST-compliant invoices and track your BAS figures automatically inside Enerpize. Start for free, no credit card required.

GST-Free vs. Input-Taxed vs. Taxable: Getting the Classification Right

One of the most common invoice errors in Australian small business is applying GST to a supply that is legally GST-free, or forgetting to apply it to a taxable one. The three categories have distinct treatment on an invoice.

| Supply Type | GST Rate | Invoice Treatment | Common Examples |

| Taxable supply | 10% | GST shown per line; included in GST collected for BAS. | Software subscriptions, consulting, construction services, electronics, clothing. |

| GST-free supply | 0% | Show $0.00 GST or label 'GST-free'; does not affect GST collected. | Basic food, most medical services, exported goods and services, education courses. |

| Input-taxed supply | 0% | No GST charged; supplier also cannot claim input tax credits on related costs. | Residential rent, financial supplies, precious metals (first supply). |

The distinction between GST-free and input-taxed matters because the tax credit treatment differs. On a GST-free supply, the supplier can still claim input tax credits on their costs. On an input-taxed supply, they cannot. If your business operates across both categories (for example, a property management company charging fees on residential and commercial leases), the invoice template must support per-line GST classification. Enerpize's expense tracking separates GST-claimable and non-claimable costs automatically, so your input tax credit total is never overstated.

Non-Resident Businesses: GST Registration and Invoicing in Australia

Foreign businesses supplying goods or services connected with Australia may be required to register for GST even without an Australian physical presence. The obligation triggers when annual taxable turnover connected with Australia meets or is projected to meet $75,000.

Non-resident businesses have two registration paths. Simplified GST registration allows non-residents to register electronically, report, and pay GST without an ABN. Instead of an ABN, the ATO assigns a 12-digit Australian Reference Number (ARN) that must appear on all tax invoices. The limitation is that simplified registration does not allow input tax credit claims.

Standard GST registration requires an ABN, which non-residents can apply for simultaneously with GST registration. The ABN appears on invoices just as it would for an Australian business. Standard registration allows input tax credit claims on Australian business expenses.

An Australian GST invoice template designed for non-residents needs to accommodate the ARN field rather than the ABN field under simplified registration, and both fields should be clearly labelled so the buyer knows which identifier they are looking at.

How Enerpize Handles Australian GST Invoicing

Filling in a template manually works for the first twenty invoices. It breaks down when you are managing multiple clients across different GST categories, tracking which invoices have been paid, reconciling your GST collected figure against your BAS at quarter end, and trying to give a client a corrected invoice without creating a version control problem.

Enerpize is built for Australian businesses that need the compliance side handled so they can focus on the work.

Automatic GST Calculation and BAS-Ready Records

Every invoice generated in Enerpize applies the correct GST rate per line item based on how the product or service is classified in your catalogue. Taxable supplies carry 10%. GST-free items carry 0%. The system applies the ATO's total invoice rounding rule automatically, so the GST total on the invoice matches what flows into your BAS report to the cent. At quarter end, your GST collected and input tax credit figures are already reconciled inside the system.

ABN Validation and Buyer Identity

Enerpize stores your ABN and validates that it appears on every invoice before the document is issued. For sales over $1,000, the buyer's ABN field is required before the invoice can be finalised. This removes the most common compliance gap in Australian invoicing: an invoice that looks complete but is missing the buyer's identifier for a high-value transaction.

Multi-Currency Invoicing for International Clients

Australian businesses invoicing overseas clients in foreign currencies face a dual obligation: the invoice must show the amount in the foreign currency and the AUD equivalent at the exchange rate on the date of supply, plus a notation of the rate used. Enerpize supports invoicing across 135+ currencies and can display dual-currency amounts on the same invoice, satisfying both the client's payment records and the ATO's forex documentation requirements.

GST-Free Export Invoice Support

When an Australian business exports goods or services, the supply is generally GST-free under Division 38. Enerpize allows you to classify products and services as GST-free exports within the system, so the invoice automatically shows $0.00 GST for those line items while still displaying all the required fields, including your ABN and the tax invoice title, that make the document valid.

Invoice History, Corrections, and BAS Traceability

The ATO requires businesses to retain tax invoice records for five years. When a client asks for a corrected invoice, Enerpize tracks the original and the amendment separately so there is no confusion in your records about which version was used for BAS purposes. The audit trail is built in, not added on. Supplier invoices received through Enerpize's purchase management module are stored against the same five-year record as your issued tax invoices, so your input tax credit trail is complete on both sides.

See how Enerpize manages GST calculations, BAS reconciliation, and invoice records automatically. Start for free, no credit card required.

Key Takeaways

- A valid Australian GST invoice template must include 7 mandatory fields for sales under $1,000 and an 8th (buyer identity or ABN) for sales of $1,000 or more, as set out by the ATO in GSTR 2013/1.

- If a GST-registered customer requests a tax invoice, you have 28 calendar days to provide one for any taxable sale over $82.50. Missing this window creates a compliance breach and blocks the buyer's input tax credit claim.

- GST can be shown per line item or as a total-price-inclusive statement. The second method is only valid when all items are taxable and GST is exactly one-eleventh of the total, and only for invoices under $1,000.

- The ATO updated its eInvoicing rules in August 2025: eInvoices issued under the Peppol A-NZ specification do not require the heading "Tax Invoice" to be legally valid, a change most businesses have not yet absorbed.

- Every tax invoice you issue feeds directly into your quarterly BAS. An invalid invoice delays your client's input tax credit claim, strains the business relationship, and creates a visible gap in your ATO compliance record. Enerpize's accounting software keeps every invoice and its BAS period tagged automatically.

- Non-resident businesses with Australian GST turnover of $75,000 or more must register for GST and issue compliant invoices using either an ABN (standard registration) or an ARN (simplified registration), with the correct identifier displayed on every document.

Get Started with Enerpize

Enerpize generates ATO-compliant Australian GST invoices automatically, calculates the 10% GST rate per line item, validates your ABN on every document, and keeps your BAS figures reconciled across every quarter. More than 40,000 businesses in the Enerpize ecosystem manage their invoicing, accounting, payroll, and inventory in one system. Start for free. No credit card required.

FAQs

What is an Australian GST invoice template?

An Australian GST invoice template is a pre-structured billing document that includes all fields required by the ATO for GST-registered businesses: the title "Tax Invoice," the seller's ABN, a date of issue, a description of the goods or services, the GST amount, and for sales over $1,000, the buyer's identity or ABN. It is the document that allows a GST-registered buyer to claim an input tax credit on their Business Activity Statement.

What is the difference between a tax invoice and a regular invoice in Australia?

A tax invoice must include the title "Tax Invoice," display the seller's ABN, and show the GST amount explicitly. A regular invoice (used by businesses not registered for GST) must not include those words or any GST reference. Issuing a document headed "Tax Invoice" when you are not GST-registered is an offence under Australian tax law. If your annual turnover is under $75,000 and you have not registered, use a standard invoice template and state that no GST has been charged.

Do I need the buyer's ABN on every invoice?

Only for sales of $1,000 or more (GST-inclusive). For sales below that threshold, the buyer's identity is not a mandatory field under ATO rules, though including it is best practice for record-keeping and dispute resolution. If your invoice template consistently includes the buyer's ABN field for all transactions, it satisfies both tiers regardless of the transaction amount.

Can I email a GST invoice as a PDF?

Yes. The ATO has never required paper invoices. A PDF emailed to a client is a valid tax invoice as long as it contains all the required fields. The same applies to invoices delivered via online portal, accounting software, or eInvoicing through the Peppol network. The format of delivery is irrelevant. The content is what determines validity.

What happens if my invoice is missing the ABN?

A tax invoice without the seller's ABN is not a valid tax invoice under ATO rules. The buyer cannot use it to claim an input tax credit. If you discover an invoice was issued without the ABN, issue a replacement immediately with all required fields and notify the buyer so they can substitute it in their records before lodging their BAS.

How long do I need to keep tax invoice records?

The ATO requires businesses to retain tax invoice records for five years from the date of the transaction, regardless of whether the business remains active for that period. This includes both invoices you issued and valid tax invoices you received from suppliers that supported input tax credit claims on your BAS.

Can a non-resident business issue a GST tax invoice without an ABN?

Yes, under simplified GST registration. The ATO assigns a 12-digit Australian Reference Number (ARN) to non-resident businesses that register under the simplified scheme. The ARN must appear on all tax invoices in place of the ABN. Non-residents using standard GST registration obtain an ABN and use it the same way an Australian business would.

What is an input tax credit and how does a tax invoice enable it?

An input tax credit is the mechanism by which a GST-registered business recovers the GST it paid on business purchases. When you receive a valid tax invoice from a supplier, the GST shown on that invoice becomes a credit you can claim against your GST collected figure when you lodge your BAS. Without a valid tax invoice, the ATO will not allow the credit, and you effectively pay GST twice: once to your supplier and once to the ATO.

About the Author

Omar El Bahr is a Senior Digital Growth Specialist at Enerpize, where he leads SEO, content strategy, and organic growth across international markets. He is a Forbes Communications Council contributor and has written for Entrepreneur on business communication and digital strategy.

Disclaimer

The information on this page is provided for general informational purposes only and does not constitute legal, tax, or financial advice. While every effort has been made to ensure accuracy at the time of publication, Australian GST laws and ATO requirements can change. Enerpize does not warrant that this content is complete, current, or applicable to your specific circumstances. Businesses should consult a registered tax agent or accountant before making compliance decisions. For the most current requirements, refer directly to the Australian Taxation Office at ato.gov.au.